Conveyorized car wash service company Mister Car Wash (NYSE:MCW) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 6.5% year on year to $249.3 million. The company’s outlook for the full year was also close to analysts’ estimates with revenue guided to $991.5 million at the midpoint. Its non-GAAP profit of $0.09 per share was 22.1% above analysts’ consensus estimates.

Is now the time to buy Mister Car Wash? Find out by accessing our full research report, it’s free.

Mister Car Wash (MCW) Q3 CY2024 Highlights:

- Revenue: $249.3 million vs analyst estimates of $249.1 million (in line)

- Adjusted EPS: $0.09 vs analyst estimates of $0.07 (22.1% beat)

- EBITDA: $78.8 million vs analyst estimates of $73.21 million (7.6% beat)

- Management raised its full-year Adjusted EPS guidance to $0.36 at the midpoint, a 10.9% increase

- EBITDA guidance for the full year is $315.5 million at the midpoint, above analyst estimates of $308.6 million

- Gross Margin (GAAP): 29.3%, down from 31.5% in the same quarter last year

- Operating Margin: 19.9%, up from 18.4% in the same quarter last year

- EBITDA Margin: 31.6%, up from 30.6% in the same quarter last year

- Same-Store Sales rose 2.9% year on year (1.7% in the same quarter last year) (beat)

- Market Capitalization: $2.09 billion

“We are pleased with our strong third quarter performance and momentum in the business. Our subscription business remained incredibly resilient, our new premium Titanium offering ramped ahead of expectations, retail sales trends moved in the right direction, and we managed expenses. All of this drove strong sales and profit growth in the third quarter,” commented John Lai, Chairperson and CEO of Mister Car Wash.

Company Overview

Formerly known as Hotshine Holdings, Mister Car Wash (NYSE:MCW) offers car washes across the United States through its conveyorized service.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

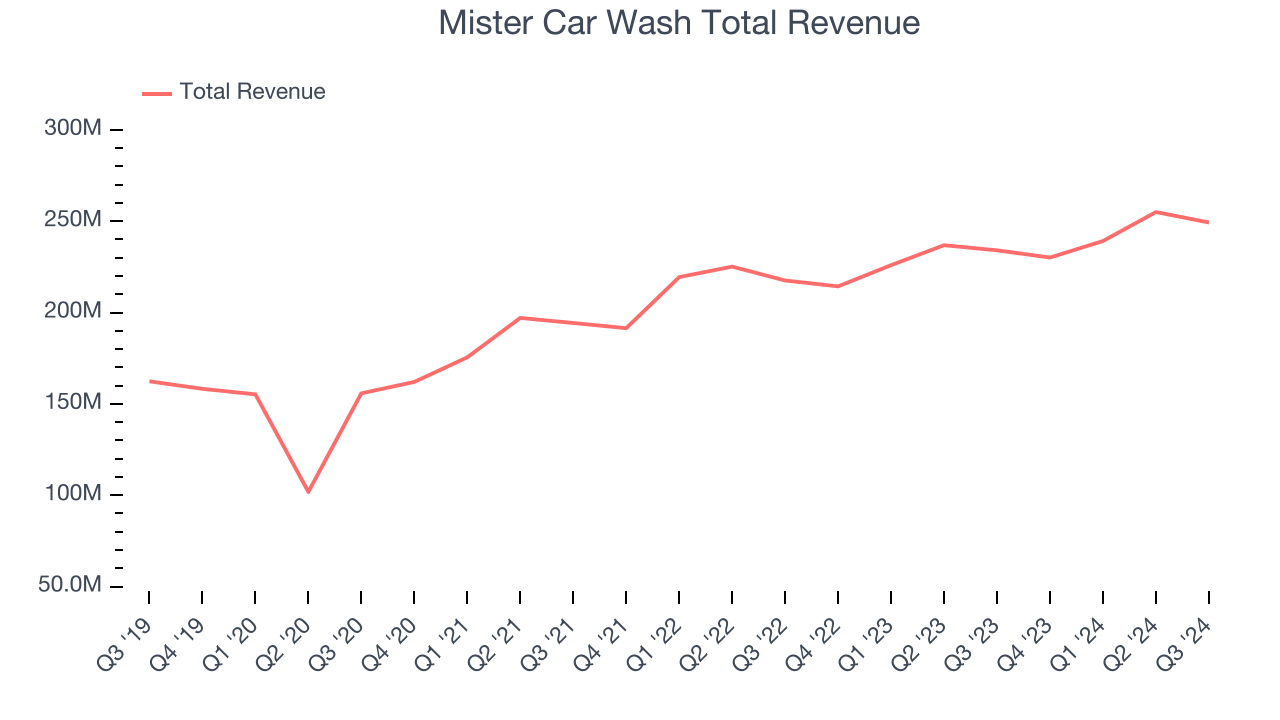

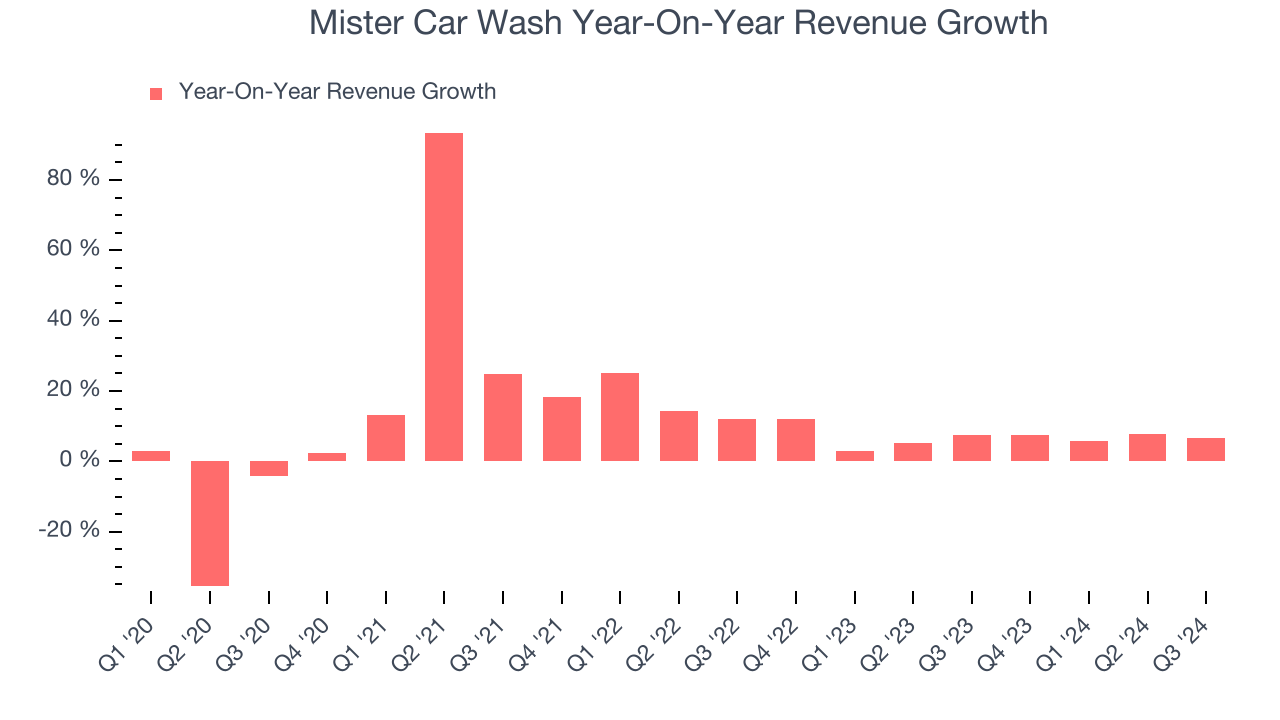

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last five years, Mister Car Wash grew its sales at a tepid 9.5% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or emerging trend. Mister Car Wash’s recent history shows its demand slowed as its annualized revenue growth of 6.8% over the last two years is below its five-year trend.

We can better understand the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Mister Car Wash’s same-store sales averaged 1.4% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Mister Car Wash grew its revenue by 6.5% year on year, and its $249.3 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.8% over the next 12 months, an improvement versus the last two years. Although this projection illustrates the market thinks its newer products and services will catalyze better performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

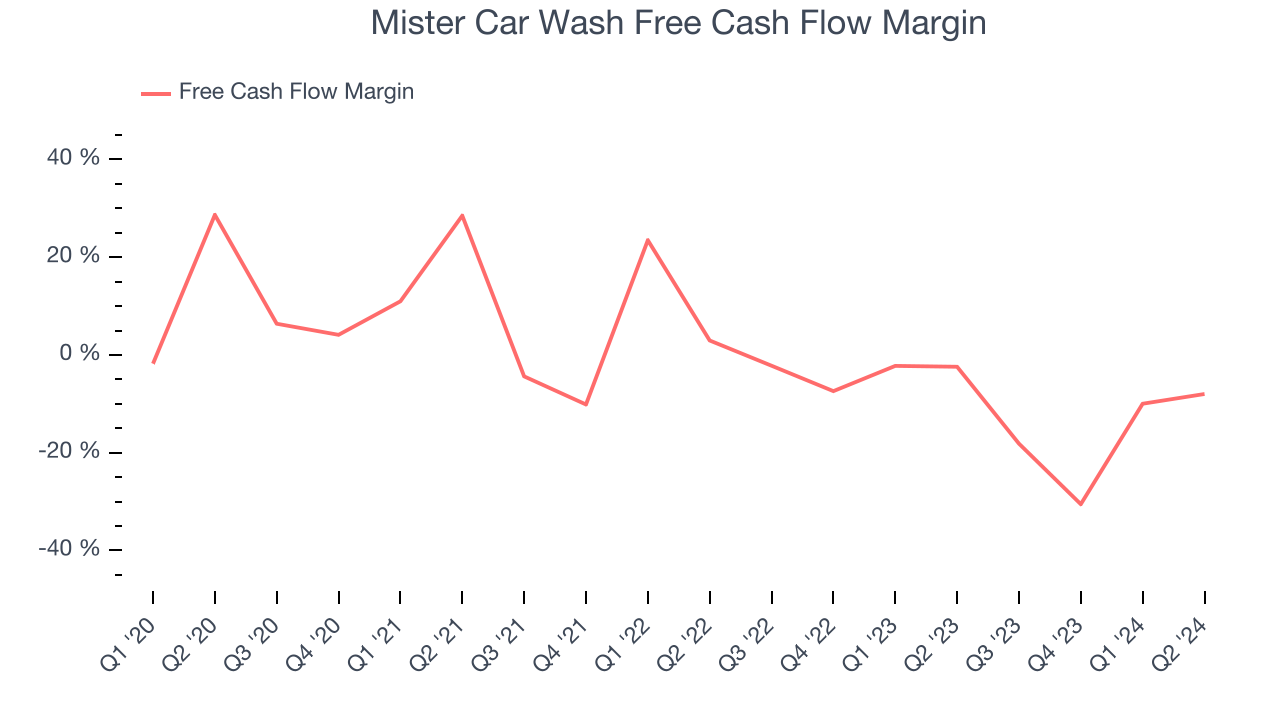

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the last two years, Mister Car Wash’s demanding reinvestments to stay relevant have drained its resources. Its free cash flow margin averaged negative 11.2%, meaning it lit $11.22 of cash on fire for every $100 in revenue. This is a stark contrast from its operating margin, and the investments (working capital, capital expenditures) are the primary culprit.

The company’s cash burn increased from $42.46 million of lost cash in the same quarter last year.

Key Takeaways from Mister Car Wash’s Q3 Results

We liked seeing same-store sales outperform Wall Street’s estimates. EBITDA and EPS also came in ahead of expectations this quarter. Looking ahead, EBITDA guidance came in ahead of expectations as well, and EPS guidance was raised. Overall, this was a very solid quarter. The stock traded up 10.6% to $7.38 immediately following the results.

Indeed, Mister Car Wash had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.