MSC Industrial (NYSE:MSM) Beats Q4 Sales Targets

Petr Huřťák /

January 8, 2025

Industrial supplies company MSC Industrial Direct (NYSE:MSM) reported Q4 CY2024 results topping the market’s revenue expectations, but sales fell by 2.7% year on year to $928.5 million. Its non-GAAP profit of $0.86 per share was 18.3% above analysts’ consensus estimates.

Is now the time to buy MSC Industrial? Find out in our full research report.

MSC Industrial (MSM) Q4 CY2024 Highlights:

- Revenue: $928.5 million vs analyst estimates of $904.6 million (2.7% year-on-year decline, 2.6% beat)

- Adjusted EPS: $0.86 vs analyst estimates of $0.73 (18.3% beat)

- Adjusted EBITDA: $97.52 million vs analyst estimates of $86.93 million (10.5% margin, 12.2% beat)

- Operating Margin: 7.8%, down from 10.6% in the same quarter last year

- Free Cash Flow Margin: 8.8%, up from 6.6% in the same quarter last year

- Market Capitalization: $4.46 billion

Erik Gershwind, Chief Executive Officer, said, "Our first quarter results reflect solid performance in a challenging operating environment. During the quarter, we returned to growth in the Public Sector and continued expanding our solutions footprint. While this is an encouraging start to the fiscal year, there is room for improvement, which we are addressing through the three pillars of our Mission Critical strategy."

Company Overview

Founded in NYC’s Little Italy, MSC Industrial Direct (NYSE:MSM) provides industrial supplies and equipment, offering vast and reliable selection for customers such as contractors

Maintenance and Repair Distributors

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Maintenance and repair distributors that boast reliable selection and quickly deliver products to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to serve customers everywhere. Additionally, maintenance and repair distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

Sales Growth

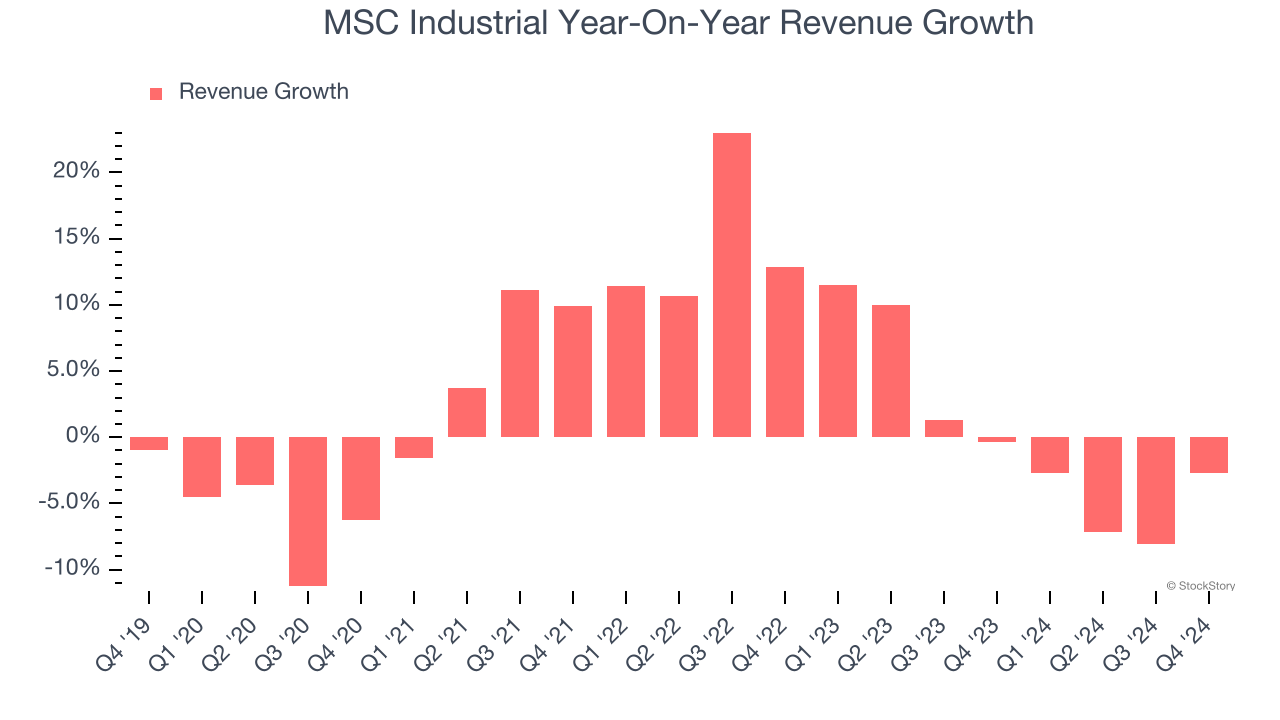

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, MSC Industrial grew its sales at a sluggish 2.5% compounded annual growth rate. This was below our standards and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. MSC Industrial’s recent history shows its demand slowed as its revenue was flat over the last two years. We also note many other Maintenance and Repair Distributors businesses have faced declining sales because of cyclical headwinds. While MSC Industrial’s growth wasn’t the best, it did perform better than its peers.

This quarter, MSC Industrial’s revenue fell by 2.7% year on year to $928.5 million but beat Wall Street’s estimates by 2.6%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and implies its newer products and services will not lead to better top-line performance yet.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

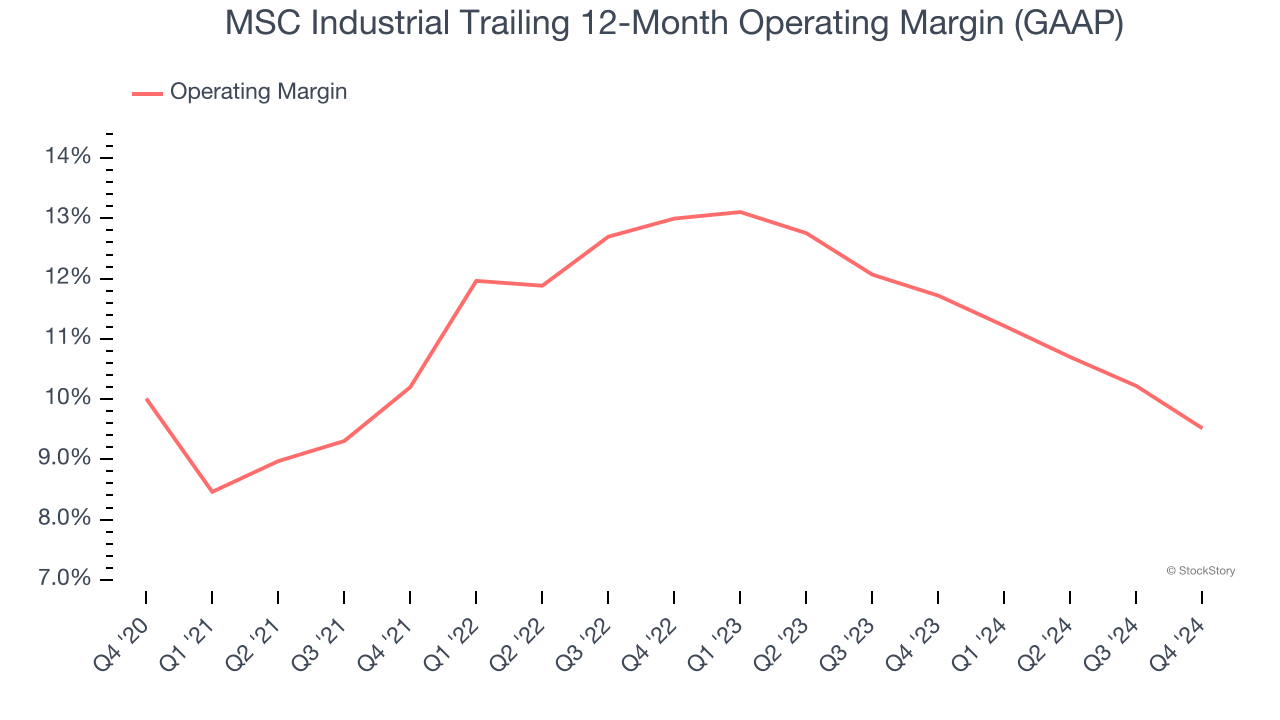

MSC Industrial has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, MSC Industrial’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years, highlighting the long-term consistency of its business.

In Q4, MSC Industrial generated an operating profit margin of 7.8%, down 2.9 percentage points year on year. Since MSC Industrial’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

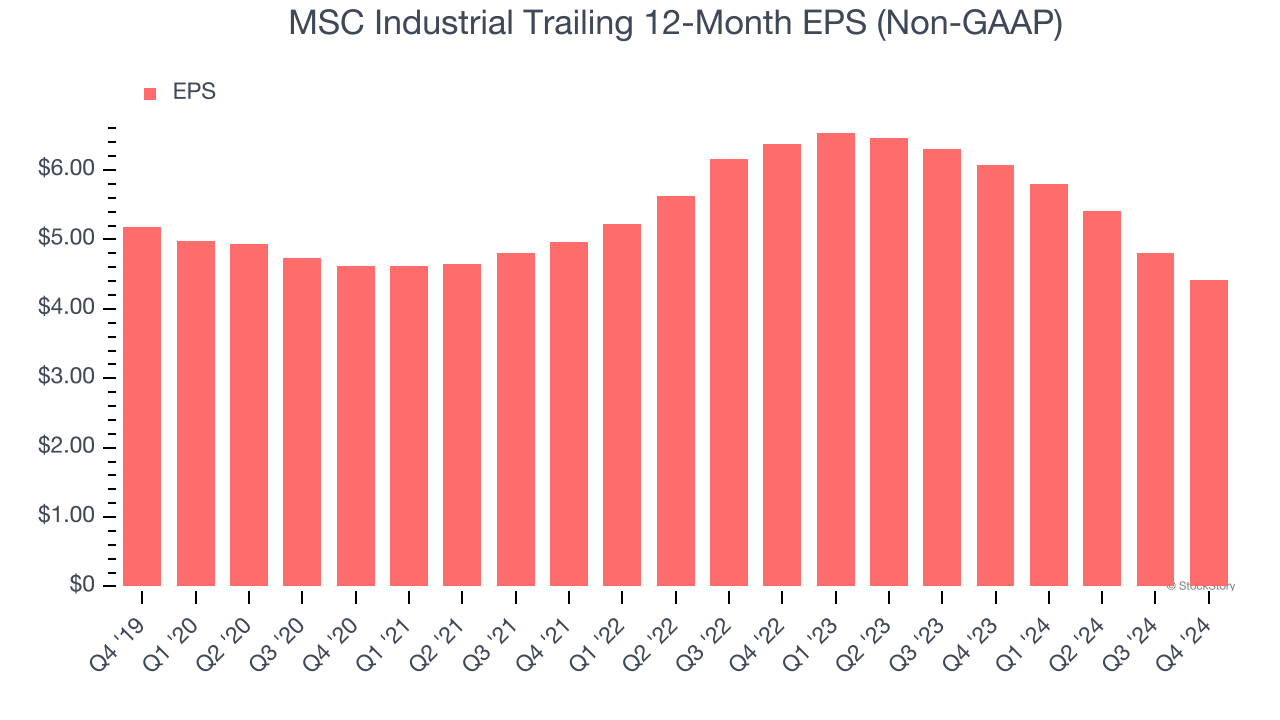

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for MSC Industrial, its EPS declined by 3.2% annually over the last five years while its revenue grew by 2.5%. However, its operating margin didn’t change during this timeframe, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

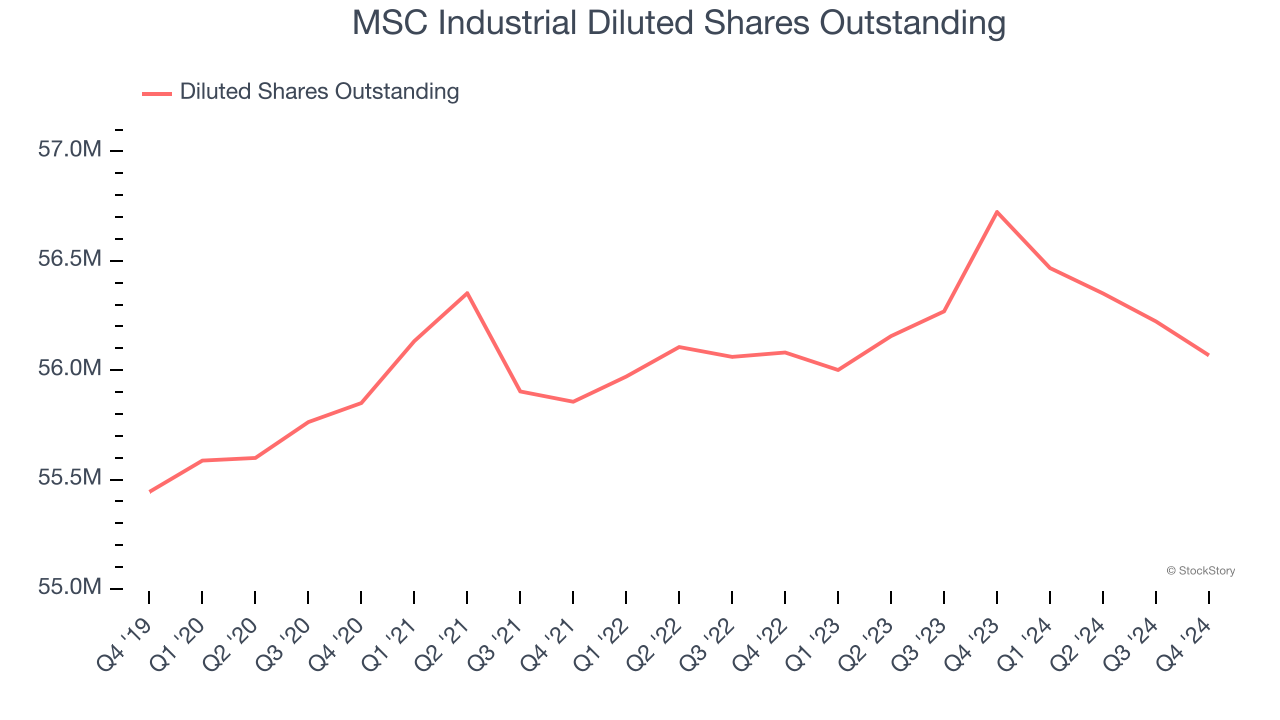

We can take a deeper look into MSC Industrial’s earnings to better understand the drivers of its performance. A five-year view shows MSC Industrial has diluted its shareholders, growing its share count by 1.1%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For MSC Industrial, its two-year annual EPS declines of 16.9% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q4, MSC Industrial reported EPS at $0.86, down from $1.25 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects MSC Industrial’s full-year EPS of $4.41 to shrink by 15.3%.

Key Takeaways from MSC Industrial’s Q4 Results

We were impressed by how significantly MSC Industrial blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 1.4% to $81 immediately after reporting.

Indeed, MSC Industrial had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.