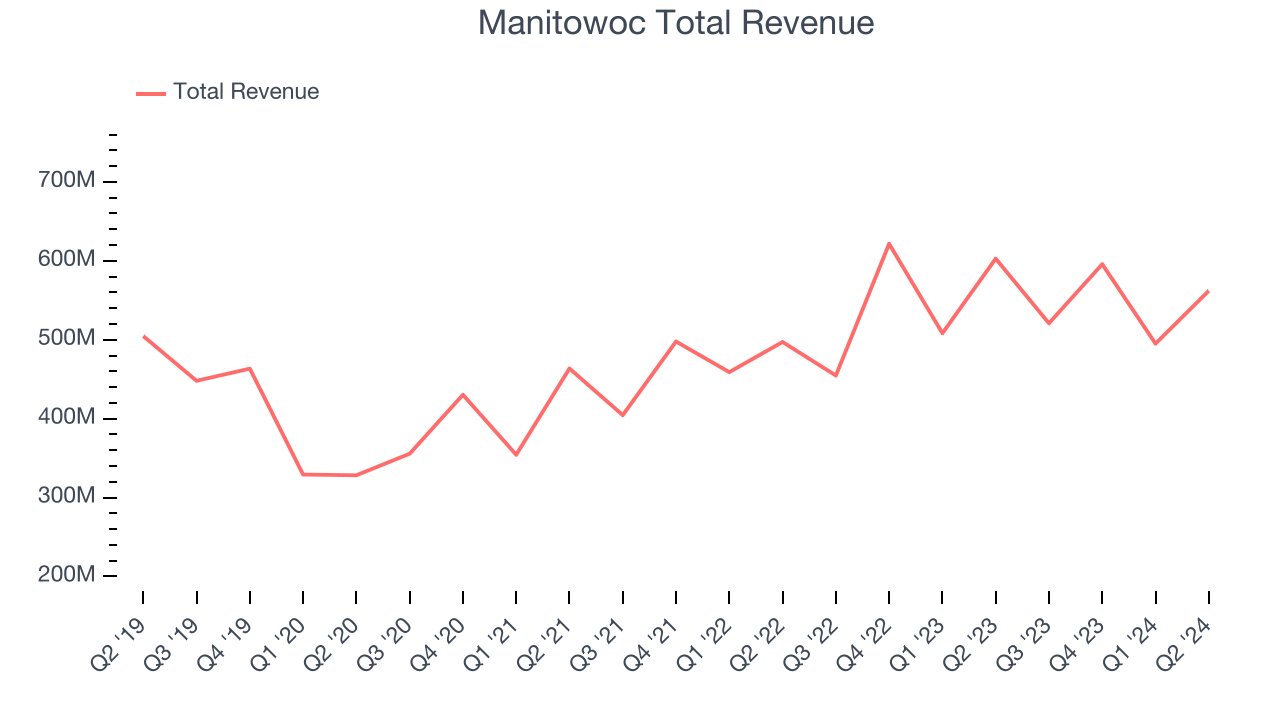

Crane and lifting equipment company Manitowoc (NYSE:MTW) fell short of analysts' expectations in Q2 CY2024, with revenue down 6.8% year on year to $562.1 million. The company's full-year revenue guidance of $2.2 billion at the midpoint also came in 3.5% below analysts' estimates. It made a non-GAAP profit of $0.25 per share, down from its profit of $0.75 per share in the same quarter last year.

Is now the time to buy Manitowoc? Find out by accessing our full research report, it's free.

Manitowoc (MTW) Q2 CY2024 Highlights:

- Revenue: $562.1 million vs analyst estimates of $598.1 million (6% miss)

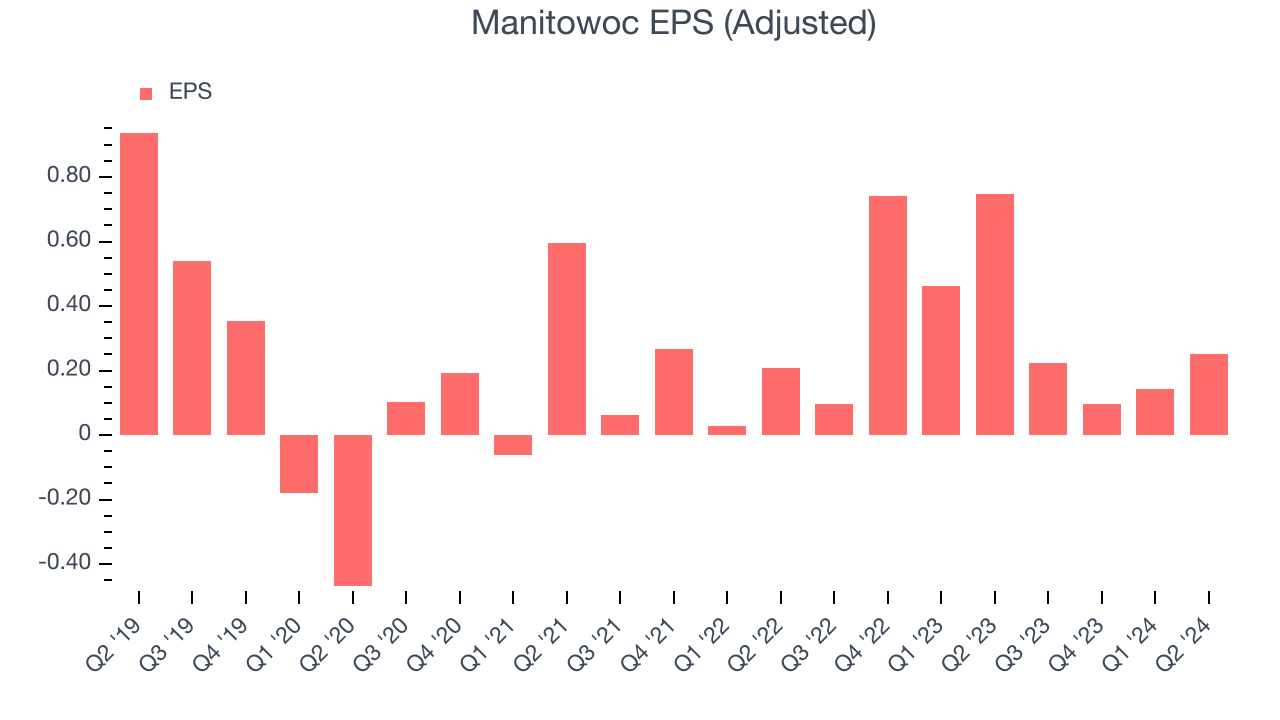

- EPS (non-GAAP): $0.25 vs analyst expectations of $0.49 (48.5% miss)

- EPS (non-GAAP) guidance for the full year is $0.68 at the midpoint, missing analyst estimates by 42.3%

- EBITDA guidance for the full year is $132,500 at the midpoint, below analyst estimates of $159.5 million

- Gross Margin (GAAP): 17.7%, down from 20.4% in the same quarter last year

- EBITDA Margin: 6.4%, down from 10% in the same quarter last year

- Free Cash Flow was -$1.9 million compared to -$42.8 million in the previous quarter

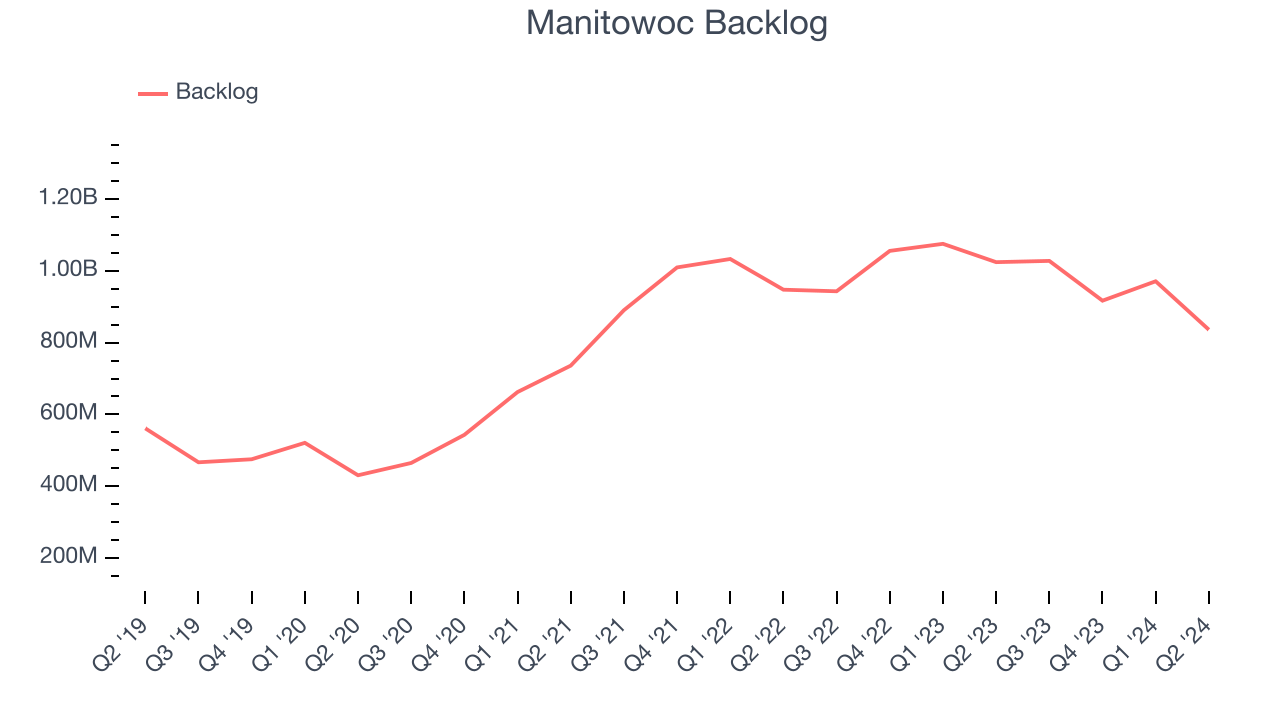

- Backlog: $836.3 million at quarter end, down 18.4% year on year

- Market Capitalization: $383.5 million

“During the second quarter, we faced a variety of operational issues which led to lower-than-anticipated results. In addition, the Tower Crane business in Europe remained a headwind to our results. Order intake was sluggish for mobile cranes in Europe and North America. Mobile customers have been slow to commit to new cranes in the face of the uncertainties associated with the upcoming U.S. election and the continued higher interest rate environment. Looking at the balance of the year, we expect weaker demand to continue. As a result, and with a focus on inventory reductions to generate free cash flow, we took actions to adjust our build schedules in the second half. We have updated our full year guidance accordingly,” commented Aaron H. Ravenscroft, President and Chief Executive Officer of The Manitowoc Company, Inc.

Contracted by the United States Navy during WWII, Manitowoc (NYSE:MTW) provides cranes and lifting equipment.

Construction Machinery

Automation that increases efficiencies and connected equipment that collects analyzable data have been trending, creating new sales opportunities for construction machinery companies. On the other hand, construction machinery companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the commercial and residential construction that drives demand for these companies’ offerings.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. Regrettably, Manitowoc's sales grew at a weak 2.9% compounded annual growth rate over the last five years. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Manitowoc's annualized revenue growth of 8.2% over the last two years is above its five-year trend, suggesting some bright spots.

We can dig further into the company's revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Manitowoc's backlog reached $836.3 million in the latest quarter and averaged 1.2% year-on-year declines over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Manitowoc was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Manitowoc missed Wall Street's estimates and reported a rather uninspiring 6.8% year-on-year revenue decline, generating $562.1 million of revenue. Looking ahead, Wall Street expects sales to grow 5.5% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

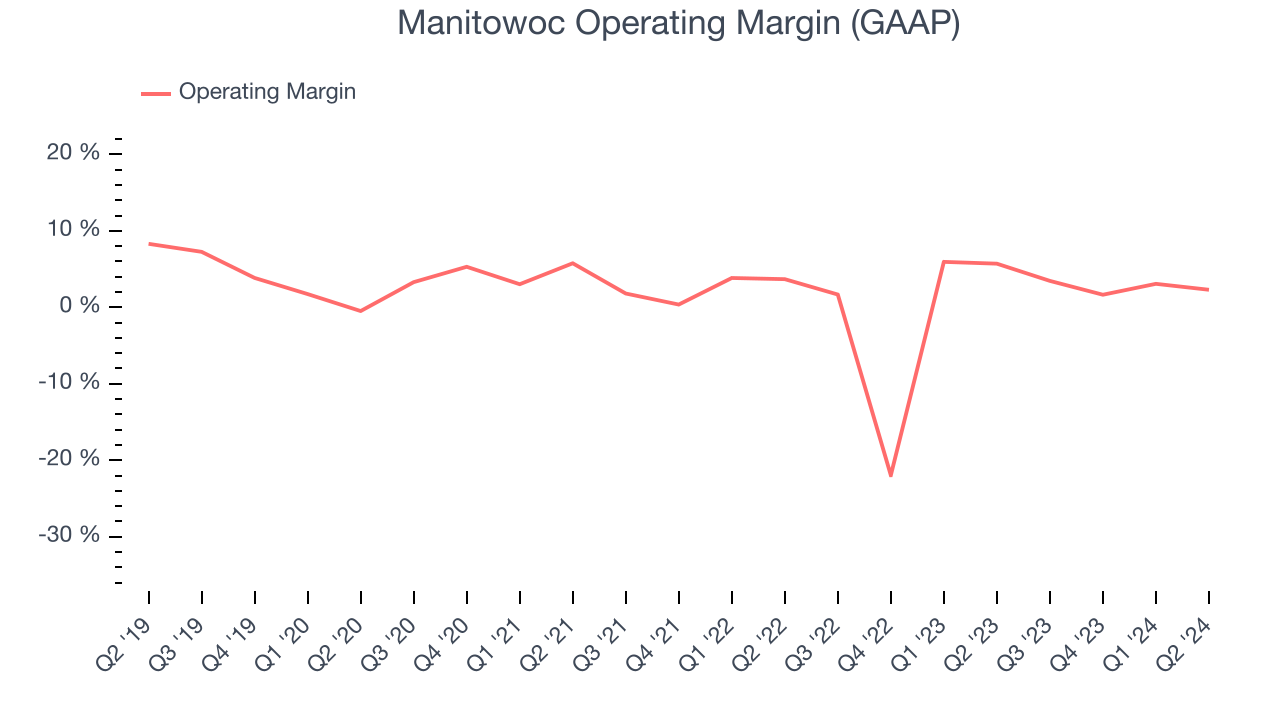

Manitowoc was profitable over the last five years but held back by its large expense base. It demonstrated lousy profitability for an industrials business, producing an average operating margin of 1.7%. This result isn't too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Manitowoc's annual operating margin might have seen some fluctuations but has generally stayed the same over the last five years, which doesn't help its cause.

In Q2, Manitowoc generated an operating profit margin of 2.3%, down 3.4 percentage points year on year. Since Manitowoc's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Sadly for Manitowoc, its EPS declined by 12.4% annually over the last five years while its revenue grew by 2.9%. However, its operating margin didn't change during this timeframe, telling us non-fundamental factors affected its ultimate earnings.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. For Manitowoc, its two-year annual EPS growth of 12% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q2, Manitowoc reported EPS at $0.25, down from $0.75 in the same quarter last year. This print missed analysts' estimates. Over the next 12 months, Wall Street expects Manitowoc to grow its earnings. Analysts are projecting its EPS of $0.71 in the last year to climb by 69.5% to $1.21.

Key Takeaways from Manitowoc's Q2 Results

We struggled to find many strong positives in these results. Its full-year revenue and EBITDA guidance fell short of Wall Street's estimates. The stock traded down 14.9% to $9.17 immediately following the results.

Manitowoc may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.