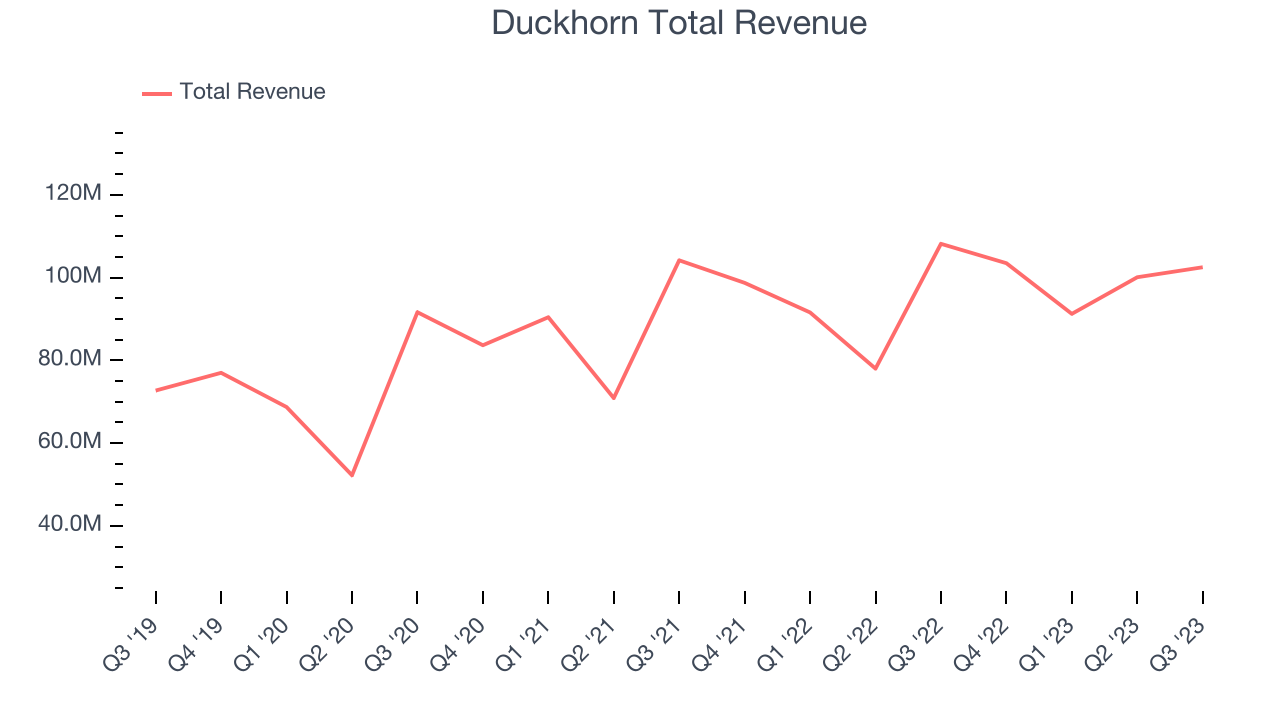

Wine company The Duckhorn Portfolio (NYSE:NAPA) missed analysts' expectations in Q1 FY2024, with revenue down 5.2% year on year to $102.5 million. The company's full-year revenue guidance of $423.5 million at the midpoint also came in 1.4% below analysts' estimates. It made a GAAP profit of $0.13 per share, down from its profit of $0.17 per share in the same quarter last year.

Is now the time to buy Duckhorn? Find out by accessing our full research report, it's free.

Duckhorn (NAPA) Q1 FY2024 Highlights:

- Revenue: $102.5 million vs analyst estimates of $103.6 million (1% miss)

- EPS: $0.13 vs analyst expectations of $0.15 (13.6% miss)

- The company reconfirmed its revenue guidance for the full year of $423.5 million at the midpoint

- Free Cash Flow of $7.67 million is up from -$40.39 million in the previous quarter

- Gross Margin (GAAP): 52.5%, up from 50.6% in the same quarter last year

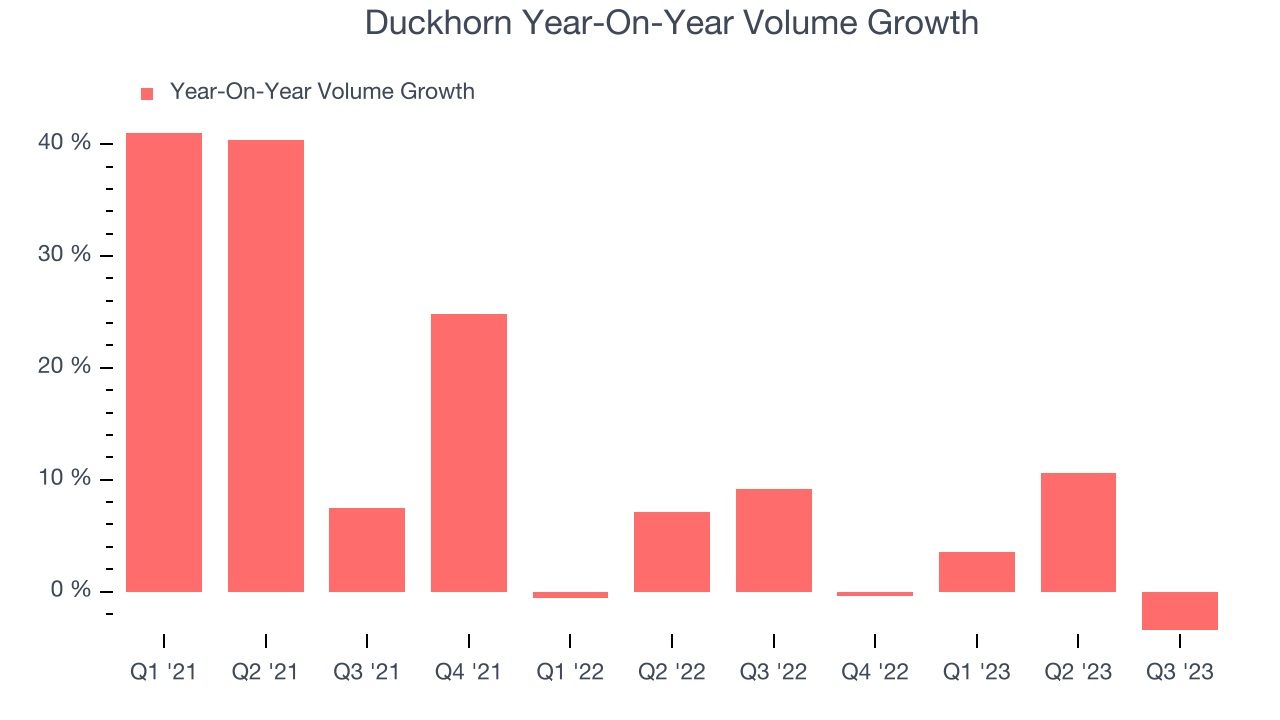

- Sales Volumes were down 3.4% year on year

Deirdre Mahlan, Interim President, Chief Executive Officer and Chairperson, commented, “We delivered a quarter at the high end of our expectations as we lapped an unseasonably strong first quarter in the prior year. In addition, we generated 90 bps of adjusted EBITDA margin expansion on less discounting and a focus on cost management.”

With many of their grapes sourced from the famous Napa Valley region of California, The Duckhorn Portfolio (NYSE:NAPA) is a producer of premium wines and known for its Merlot and other Bordeaux varietals.

Beverages and Alcohol

The beverages and alcohol category encompasses companies engaged in the production, distribution, and sale of refreshments like beer, wine, and spirits, along with soft drinks, juices, and bottled water. These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the explosion of alcoholic craft beer drinks or the steady decline of non-alcoholic sugary sodas. The industry is highly competitive, with a diverse range of products from large multinational corporations, niche brands, and startups vying for market share. It's also subject to varying degrees of government regulation and taxation, especially for alcoholic beverages.

Sales Growth

Duckhorn is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale.

As you can see below, the company's annualized revenue growth rate of 11.1% over the last three years was impressive for a consumer staples business.

This quarter, Duckhorn reported a rather uninspiring 5.2% year-on-year revenue decline, missing Wall Street's estimates. Looking ahead, analysts expect sales to grow 11.1% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Volume Growth

Duckhorn's average quarterly volume growth was a robust 6.4% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Duckhorn's Q1 2024, sales volumes dropped 3.4% year on year. This result was a reversal from the 9.2% year-on-year increase it posted 12 months ago. A one quarter hiccup shouldn't deter you from investing in a business. We'll be monitoring the company to see how things progress.

Key Takeaways from Duckhorn's Q1 Results

With a market capitalization of $1.18 billion, Duckhorn is among smaller companies, but its more than $21.18 million in cash on hand and near break-even free cash flow margins puts it in a stable financial position.

It was good to see Duckhorn beat analysts' gross margin expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue, operating margin, and EPS missed analysts' estimates, driven by worse-than-expected sales volume declines (3.4% decline vs 2.8% projected decline by Wall Street). Overall, this was a mixed quarter for Duckhorn. The company is down 4% on the results and currently trades at $9.8 per share.

Duckhorn may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.