Enterprise workflow software maker ServiceNow (NYSE:NOW) reported results in line with analyst expectations in Q1 FY2023 quarter, with revenue up 21.7% year on year to $2.1 billion. However and more positively, the important cRPO (current remaining performance obligations) beat by 2%. ServiceNow made a GAAP profit of $150 million, improving on its profit of $75 million, in the same quarter last year.

Is now the time to buy ServiceNow? Access our full analysis of the earnings results here, it's free.

ServiceNow (NOW) Q1 FY2023 Highlights:

- Revenue: $2.1 billion vs analyst estimates of $2.09 billion (small beat)

- EPS (non-GAAP): $2.37 vs analyst estimates of $2.04 (16.5% beat)

- Subscription revenue guidance for Q2 2023 is $2.04 billion at the midpoint, below analyst estimates of $2.13 billion

- The company provided subscription revenue guidance for the full year of $8.5 billion at the midpoint

- Free cash flow of $737 million, down 27.6% from previous quarter

- Customers: 1,682 customers paying more than $1m annually

- Gross Margin (GAAP): 79.1%, in line with same quarter last year

“Once again, ServiceNow delivered a powerful combination of growth and profitability,” said ServiceNow Chairman and CEO Bill McDermott.

Founded by Fred Luddy who wrote the code for the initial prototype on a single flight from San Francisco to London, ServiceNow (NYSE:NOW) offers software as a service platform that helps companies become more efficient by allowing them to automate workflows across IT, HR and Customer Service.

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

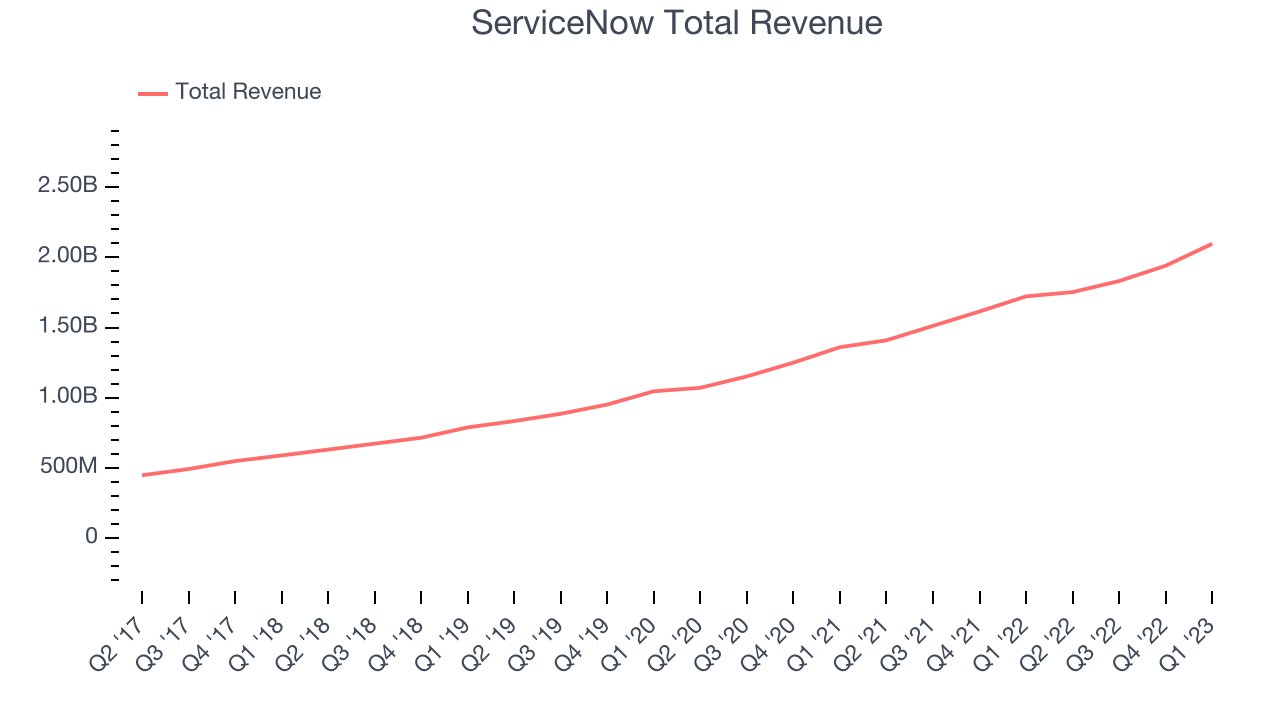

Sales Growth

As you can see below, ServiceNow's revenue growth has been strong over the last two years, growing from quarterly revenue of $1.36 billion in Q1 FY2021, to $2.1 billion.

This quarter, ServiceNow's quarterly revenue was once again up a very solid 21.7% year on year. On top of that, revenue increased $156 million quarter on quarter, a very strong improvement on the $109 million increase in Q4 2022, which shows re-acceleration of growth, and is great to see.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 22.2% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

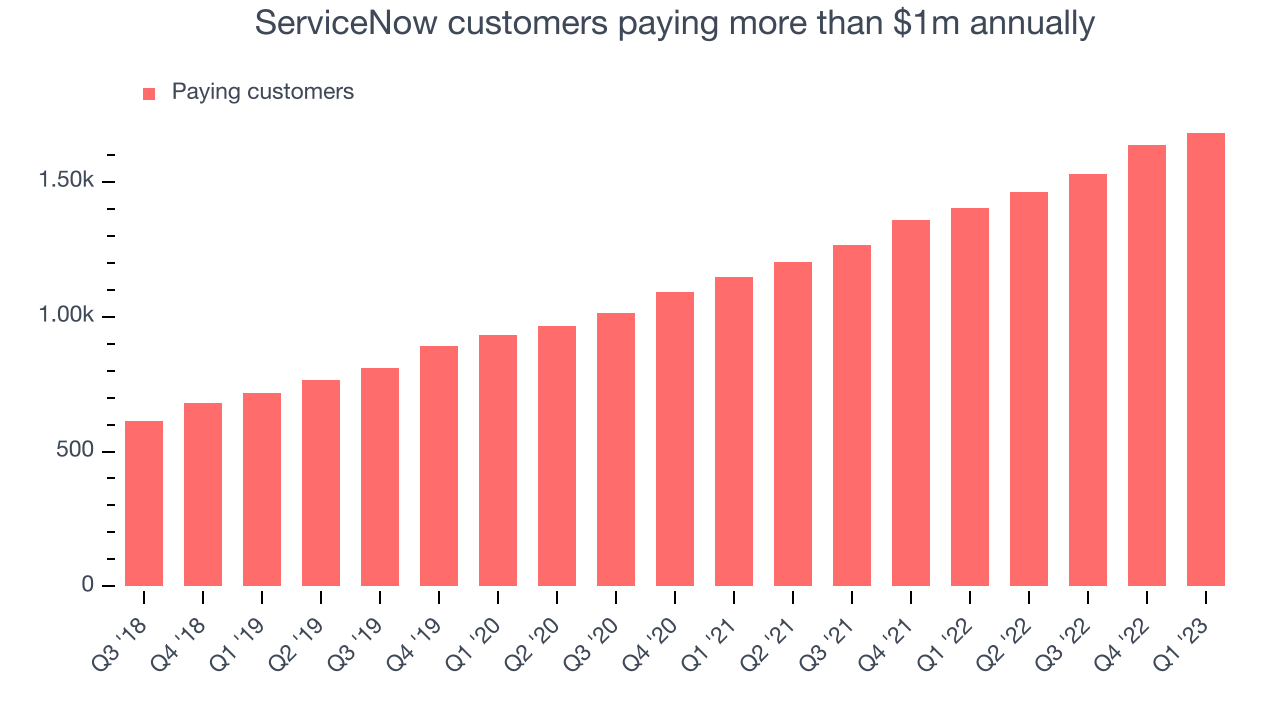

Large Customers Growth

You can see below that at the end of the quarter ServiceNow reported 1,682 enterprise customers paying more than $1m annually, an increase of 45 on last quarter. That is a bit less contract wins than last quarter and also quite a bit below what we have typically seen over the past couple of quarters, suggesting that the sales momentum with large customers is slowing down.

Key Takeaways from ServiceNow's Q1 Results

With a market capitalization of $90.1 billion, more than $4.91 billion in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

While total revenue was roughly in line, subscription revenue and cRPO beat. cRPO growth guidance for next quarter was also slightly ahead. Adjusted operating profit also beat by 9% in the quarter. On the other hand, it was unfortunate to see the slowdown in new contract wins. Overall, this quarter's results were mixed but overall fine. The company is up 2.01% on the results and currently trades at $463.25 per share.

ServiceNow may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.