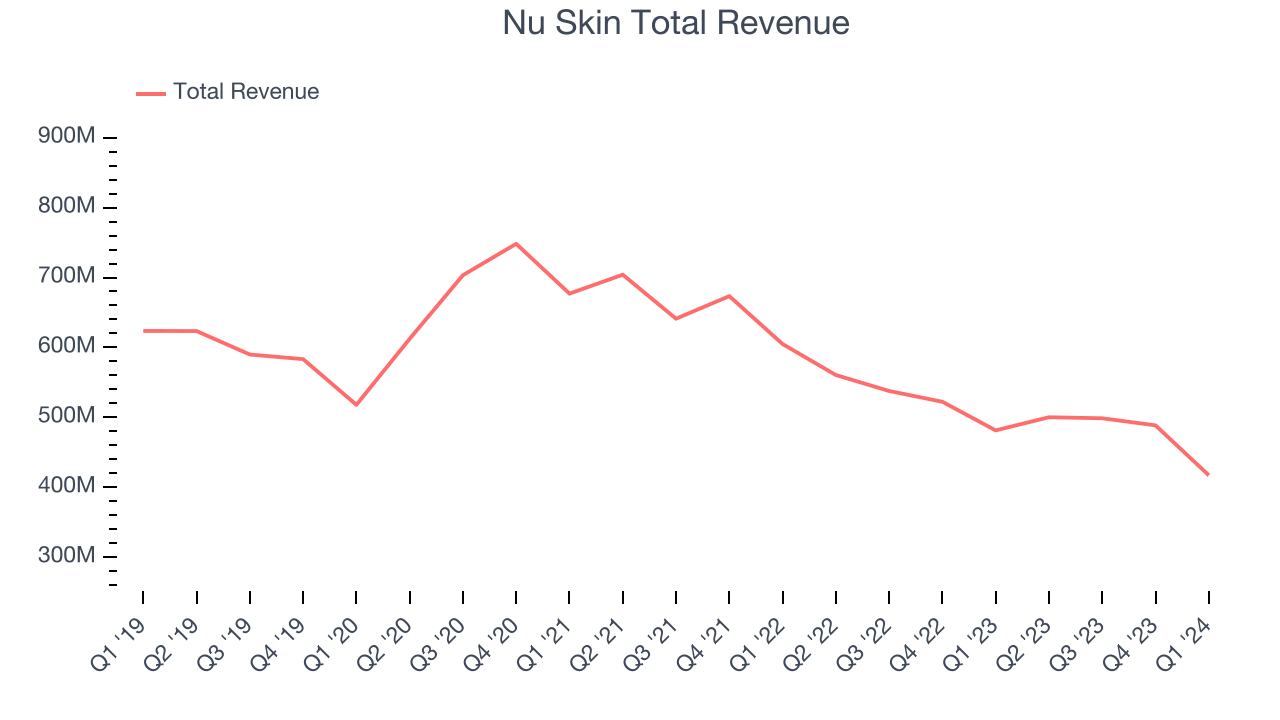

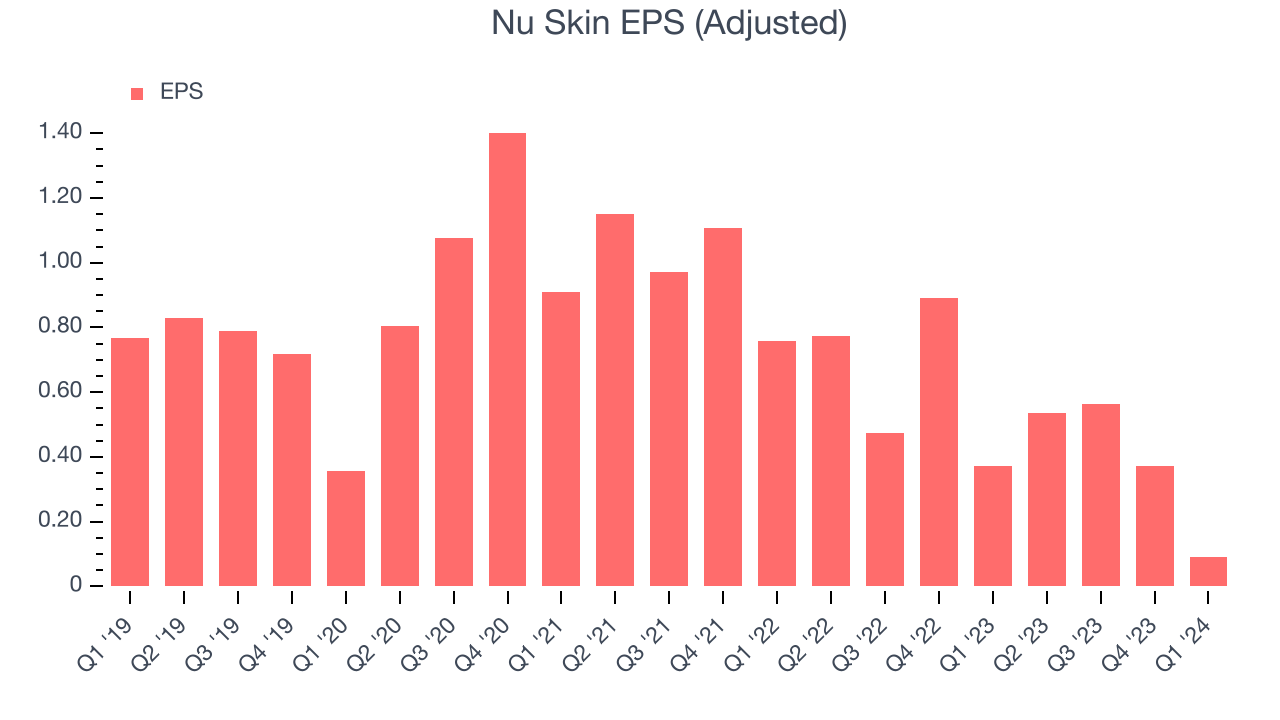

Personal care company Nu Skin (NYSE:NUS) missed analysts' expectations in Q1 CY2024, with revenue down 13.3% year on year to $417.3 million. Next quarter's revenue guidance of $437.5 million also underwhelmed, coming in 3.7% below analysts' estimates. It made a non-GAAP profit of $0.09 per share, down from its profit of $0.37 per share in the same quarter last year.

Nu Skin (NUS) Q1 CY2024 Highlights:

- Revenue: $417.3 million vs analyst estimates of $432.4 million (3.5% miss)

- EPS (non-GAAP): $0.09 vs analyst estimates of $0.05 ($0.04 beat)

- Revenue Guidance for Q2 CY2024 is $437.5 million at the midpoint, below analyst estimates of $454.4 million

- EPS (non-GAAP) Guidance for Q2 CY2024 is $0.15 at the midpoint, below analyst estimates of $0.35

- The company reconfirmed its revenue guidance for the full year of $1.8 billion at the midpoint

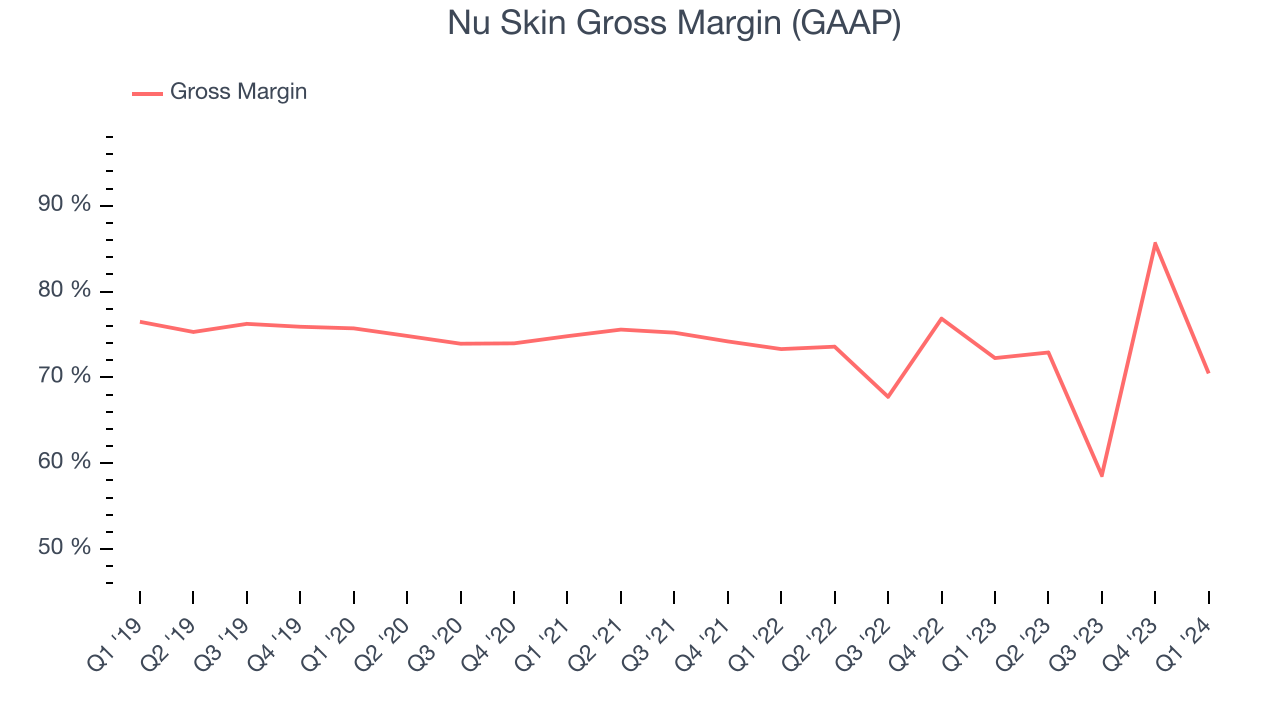

- Gross Margin (GAAP): 70.5%, down from 72.3% in the same quarter last year

- Market Capitalization: $608.4 million

With person-to-person marketing and sales rather than selling through retail stores, Nu Skin (NYSE:NUS) is a personal care and dietary supplements company that engages in direct selling.

The company operates three brands. Nu Skin is the beauty brand, ageLOC is the anti-aging brand, and Pharmanex is the health and wellness brand. The Nu Skin and ageLOC brands primarily sell skin care electronics such as facial massagers and toning devices as well as cosmetics and creams. The Pharmanex brand offers supplements for weight loss, weight management, and skin health as well as vitamins and minerals for general nutrition.

Nu Skin caters to customers who are interested in enhancing their appearance and overall well-being. These customers find value in a one-stop shop–a brand that can provide creams, devices, supplements, and more. The core customer therefore tends to be a lower to middle-income, middle-aged woman.

Nu Skin operates primarily through direct selling rather than distributing through retail stores. The direct selling model means that Nu Skin recruits and trains its own customers, who become representatives of the brand. In turn, these representatives aim to acquire new customers through marketing and sales efforts, which can be powerful because of their personal experience with Nu Skin products. Core customers therefore tend to value community and the chance to earn an extra buck as well.

Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors in the broader personal care industry include Estée Lauder (NYSE:EL), L’Oreal (ENXTPA:OR), and Coty (NYSE:COTY). Companies that operate a direct selling model in the beauty, health, or wellness categories include Herbalife (NYSE:HLF) as well as private companies Avon and Mary Kay.Sales Growth

Nu Skin carries some recognizable brands and products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Nu Skin can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue has declined over the last three years, dropping 11.4% annually. This is among the worst in the consumer staples industry, where demand is typically stable.

This quarter, Nu Skin missed Wall Street's estimates and reported a rather uninspiring 13.3% year-on-year revenue decline, generating $417.3 million in revenue. The company is guiding for a 12.5% year-on-year revenue decline next quarter to $437.5 million, a further deceleration from the 10.8% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects revenue to decline 4.1% over the next 12 months.

Gross Margin & Pricing Power

All else equal, we prefer higher gross margins. They usually indicate that a company sells more differentiated products and commands stronger pricing power.

Nu Skin's gross profit margin came in at 70.5% this quarter, down 1.8 percentage points year on year. That means for every $1 in revenue, only $0.30 went towards paying for raw materials, production of goods, and distribution expenses.

Nu Skin has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to stay one step ahead of the competition. As you can see above, it's averaged an exceptional 72.3% gross margin over the last two years. Its margin, however, has been trending down over the last year, averaging 1.4% year-on-year decreases each quarter. If this trend continues, it could suggest a more competitive environment.

Operating Margin

Operating margin is a key profitability metric for companies because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

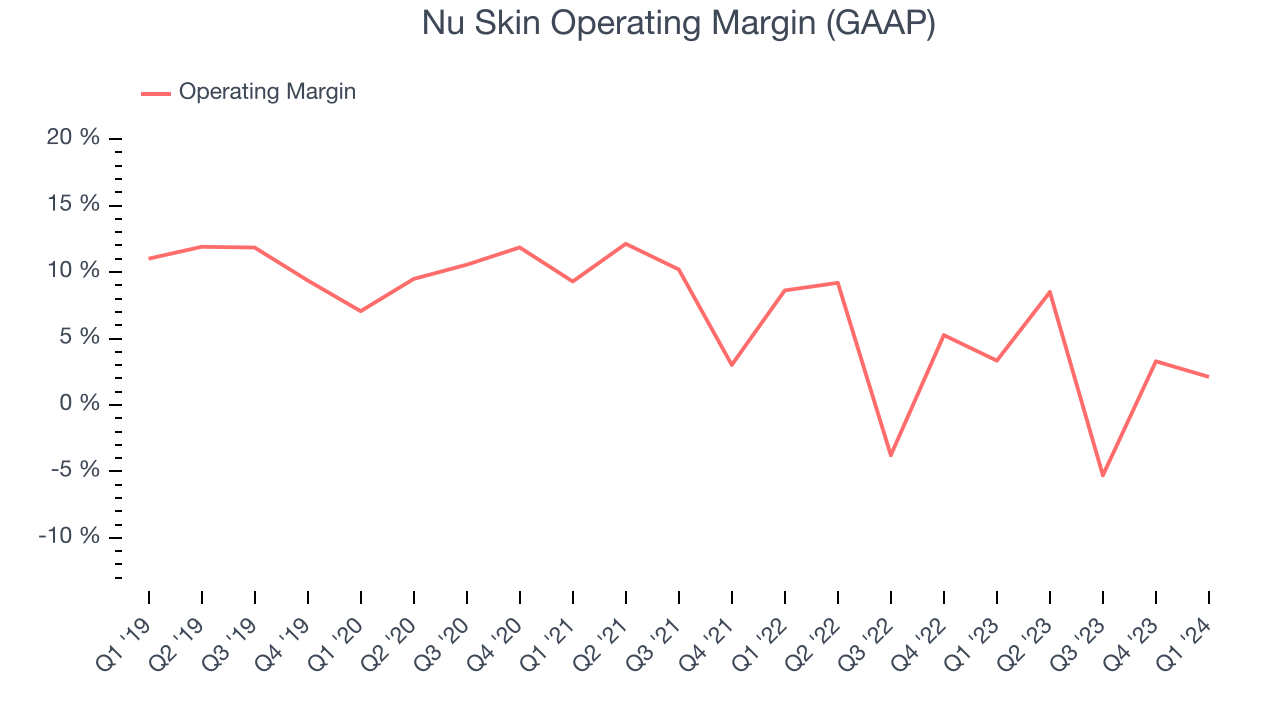

This quarter, Nu Skin generated an operating profit margin of 2.1%, down 1.2 percentage points year on year. Because Nu Skin's gross margin decreased more than its operating margin, we can infer the company had weaker pricing power and higher raw materials/transportation costs.

Zooming out, Nu Skin was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.9%. On top of that, Nu Skin's margin has slightly declined by 1.4 percentage points on average over the last year. This shows Nu Skin has faced some speed bumps along the way.

Zooming out, Nu Skin was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.9%. On top of that, Nu Skin's margin has slightly declined by 1.4 percentage points on average over the last year. This shows Nu Skin has faced some speed bumps along the way.EPS

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q1, Nu Skin reported EPS at $0.09, down from $0.37 in the same quarter a year ago. This print beat Wall Street's estimates by 80%.

Between FY2021 and FY2024, Nu Skin's EPS dropped 62.7%, translating into 28% annualized declines. We tend to steer our readers away from companies with falling EPS, especially in the consumer staples sector, where shrinking earnings could imply changing secular trends or consumer preferences. If there's no earnings growth, it's difficult to build confidence in a business's underlying fundamentals, leaving a low margin of safety around the company's valuation (making the stock susceptible to large downward swings).

Wall Street expects Nu Skin to continue performing poorly over the next 12 months, with analysts projecting an average 24.2% year-on-year decline in EPS.

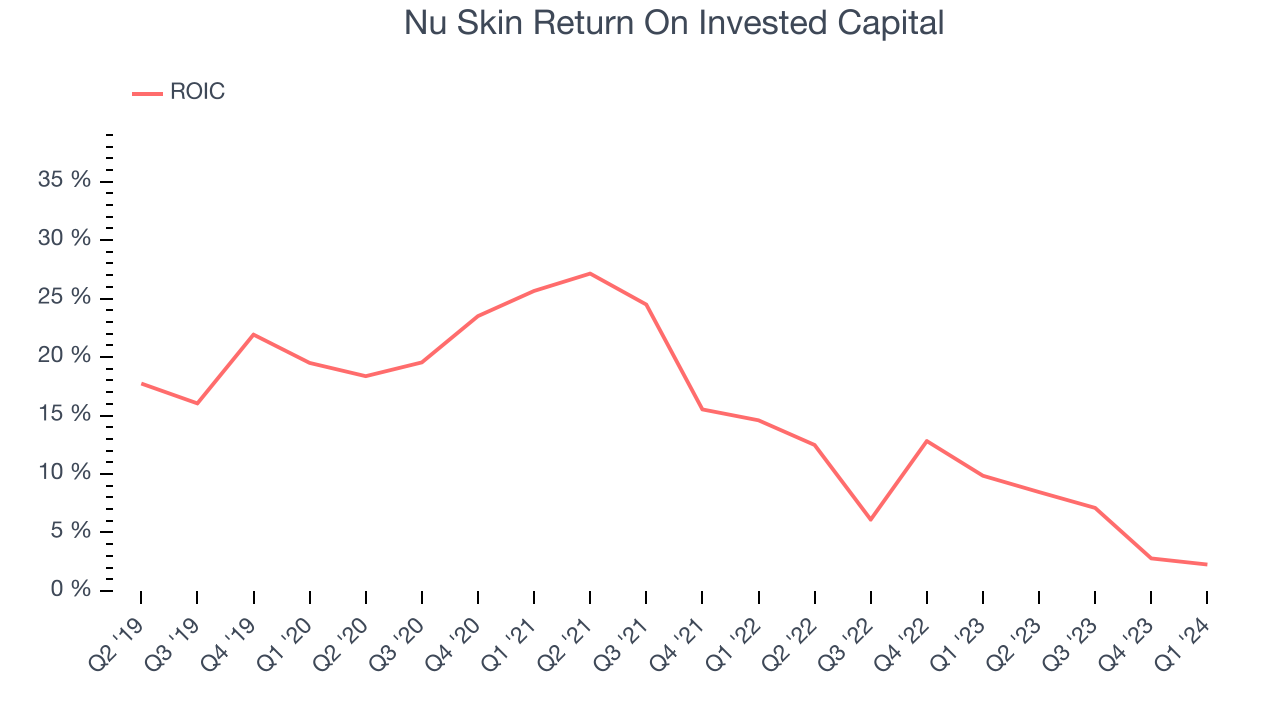

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Although Nu Skin hasn't been the highest-quality company lately because of its poor top-line performance, it historically did a solid job investing in profitable business initiatives. Its five-year average ROIC was 14.4%, higher than most consumer staples companies.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Nu Skin's ROIC significantly decreased over the last few years. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Key Takeaways from Nu Skin's Q1 Results

We were impressed by how significantly Nu Skin blew past analysts' EPS expectations this quarter. We were also excited its operating margin outperformed Wall Street's estimates. On the other hand, its earnings forecast for next quarter missed analysts' expectations. Overall, the results could have been better. The stock is flat after reporting and currently trades at $12.3 per share.

Is Now The Time?

When considering an investment in Nu Skin, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for all companies serving consumers, but in the case of Nu Skin, we'll be cheering from the sidelines. Its revenue has declined over the last three years, but at least growth is expected to increase in the short term. And while its impressive gross margins are a wonderful starting point for the overall profitability of the business, the downside is its declining EPS over the last three years makes it hard to trust. On top of that, its projected EPS for the next year is lacking.

Nu Skin's price-to-earnings ratio based on the next 12 months is 10.5x. While there are some things to like about Nu Skin and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $14.50 per share right before these results (compared to the current share price of $12.30).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.