Virtual events software company (NYSE:ONTF) reported Q4 FY2023 results beating Wall Street analysts' expectations, with revenue down 15.5% year on year to $39.34 million. The company also expects next quarter's revenue to be around $37 million, coming in 2.3% above analysts' estimates. It made a non-GAAP profit of $0.06 per share, improving from its loss of $0.04 per share in the same quarter last year.

ON24 (ONTF) Q4 FY2023 Highlights:

- Revenue: $39.34 million vs analyst estimates of $37.26 million (5.6% beat)

- EPS (non-GAAP): $0.06 vs analyst estimates of $0.02 ($0.05 beat)

- Revenue Guidance for Q1 2024 is $37 million at the midpoint, above analyst estimates of $36.18 million

- Management's revenue guidance for the upcoming financial year 2024 is $145 million at the midpoint, missing analyst estimates by 1.6% and implying 11.4% decline (vs -14.3% in FY2023)

- Free Cash Flow was -$1.97 million compared to -$3.20 million in the previous quarter

- Gross Margin (GAAP): 74.6%, up from 71.6% in the same quarter last year

- Market Capitalization: $323.7 million

Started in 1998 as a platform to broadcast press conferences, ON24’s (NYSE:ONTF) software helps organizations organize online webinars and other virtual events and convert prospects into customers.

The Covid-19 pandemic has accelerated the shift to a digital-first world. Given the growing difficulty of organizing physical meetings, more companies are adopting digital channels to engage with customers and are realizing it is harder than just video streaming a presentation. One directional online webinars are missing the interactivity of real world conferences and potential customers either give up during the stream or leave without being able to engage anybody from the company to ask questions.

ON24’s software as a service helps companies organize interactive online events like webinars or conferences and create a library of engaging pre-recorded content. The software provides users with tools that handle everything from registrations, streaming the video itself, to analytics on how customers reacted during the talk. Most importantly it allows companies to enhance their webinars with interactive features that allow the viewers to ask questions, immediately start a free trial of the product or request a meeting with the company’s representative. ON24 also connects with marketing and sales automation data to provide better insights to sales teams, making it easier to convert prospects into paying users.

Virtual Events Software

Online marketing and sales are expanding at a rapid pace. Compared to the offline advertising market, which has been affected by the Covid pandemic and is challenging to measure and improve, more organizations are expected to adopt data-driven digital engagement platforms to better engage their customers online.

ON24 faces competition from marketing and web engagement tools provided by companies including Zoom (NASDAQ:ZM), LogMeIn (NASDAQ:LOGM), Intrado, Cisco (NASDAQ:CSCO), and Cvent.

Sales Growth

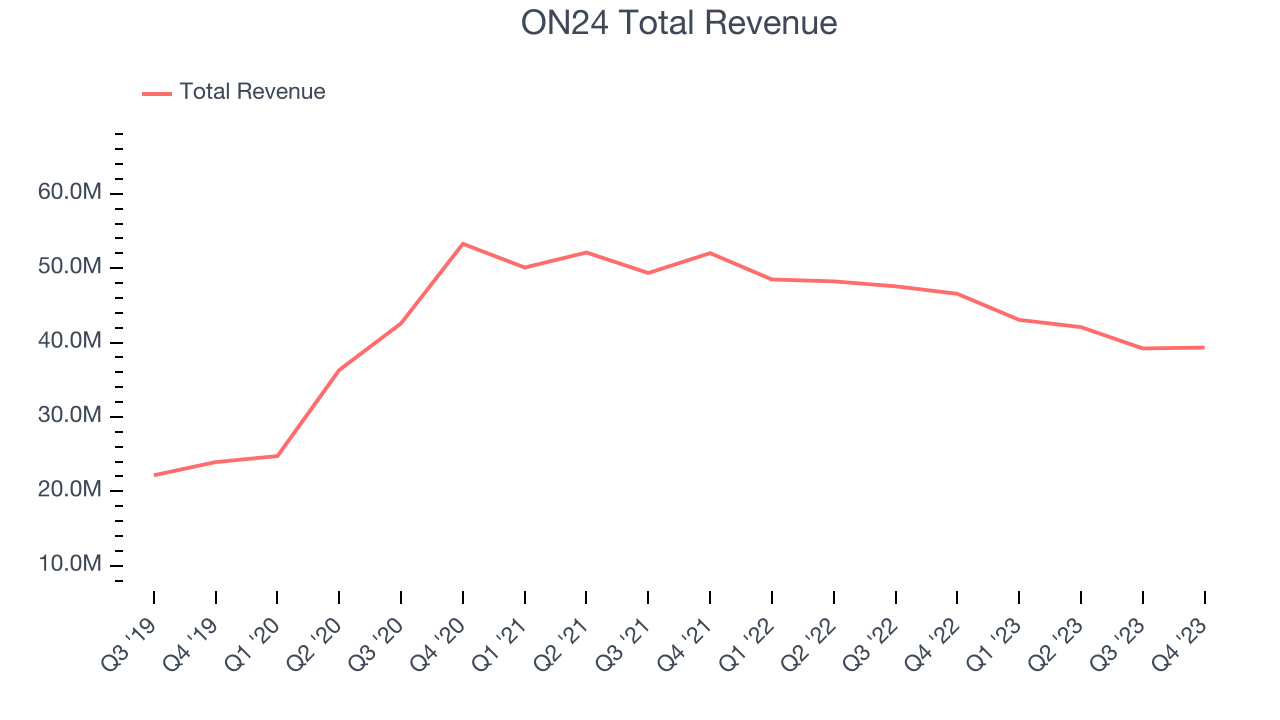

As you can see below, ON24's revenue has been declining over the last two years, shrinking from $52.03 million in Q4 FY2021 to $39.34 million this quarter.

ON24's revenue was down again this quarter, falling 15.5% year on year.

Next quarter, ON24 is guiding for a 14.1% year-on-year revenue decline to $37 million, a further deceleration from the 11.2% year-on-year decrease it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $145 million at the midpoint, declining 11.4% year on year compared to 14.2% drop in FY2023.

Profitability

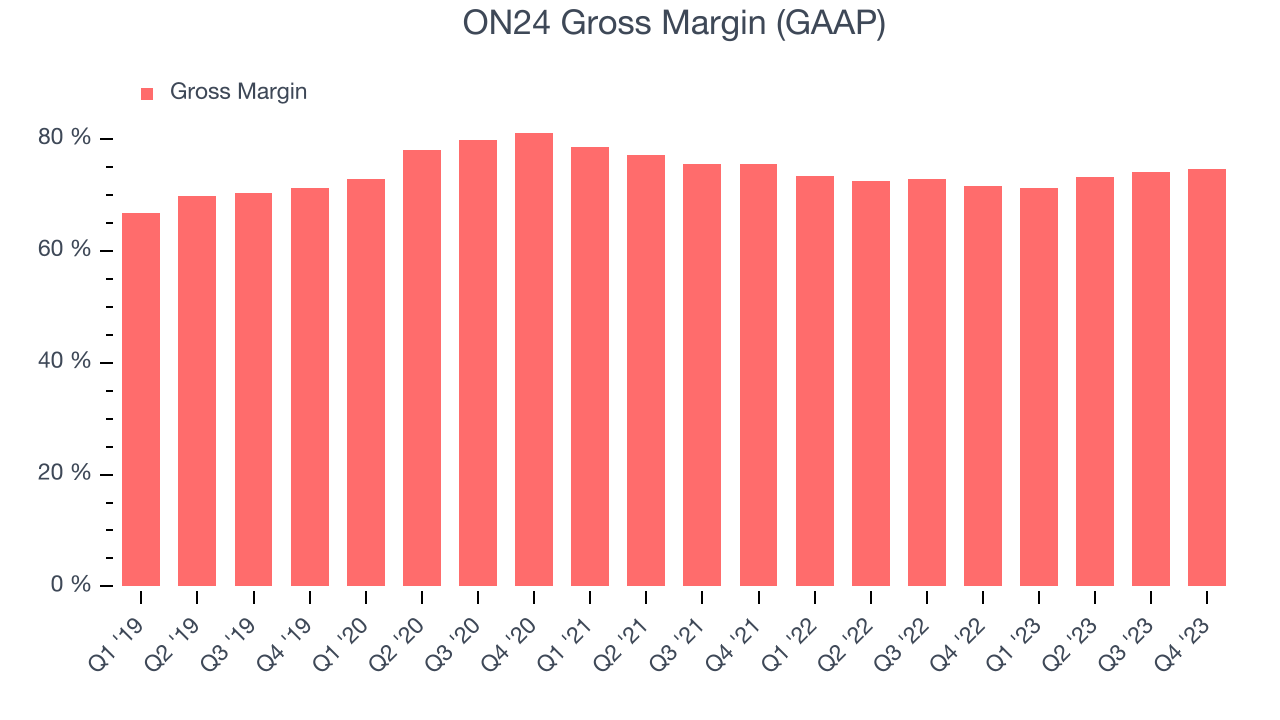

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. ON24's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 74.6% in Q4.

That means that for every $1 in revenue the company had $0.75 left to spend on developing new products, sales and marketing, and general administrative overhead. Trending up over the last year, ON24's gross margin is around the average of a typical SaaS businesses. Gross margin has a major impact on a company’s ability to develop new products and invest in marketing, which may ultimately determine the winner in a competitive market. This makes it a critical metric to track for the long-term investor.

Cash Is King

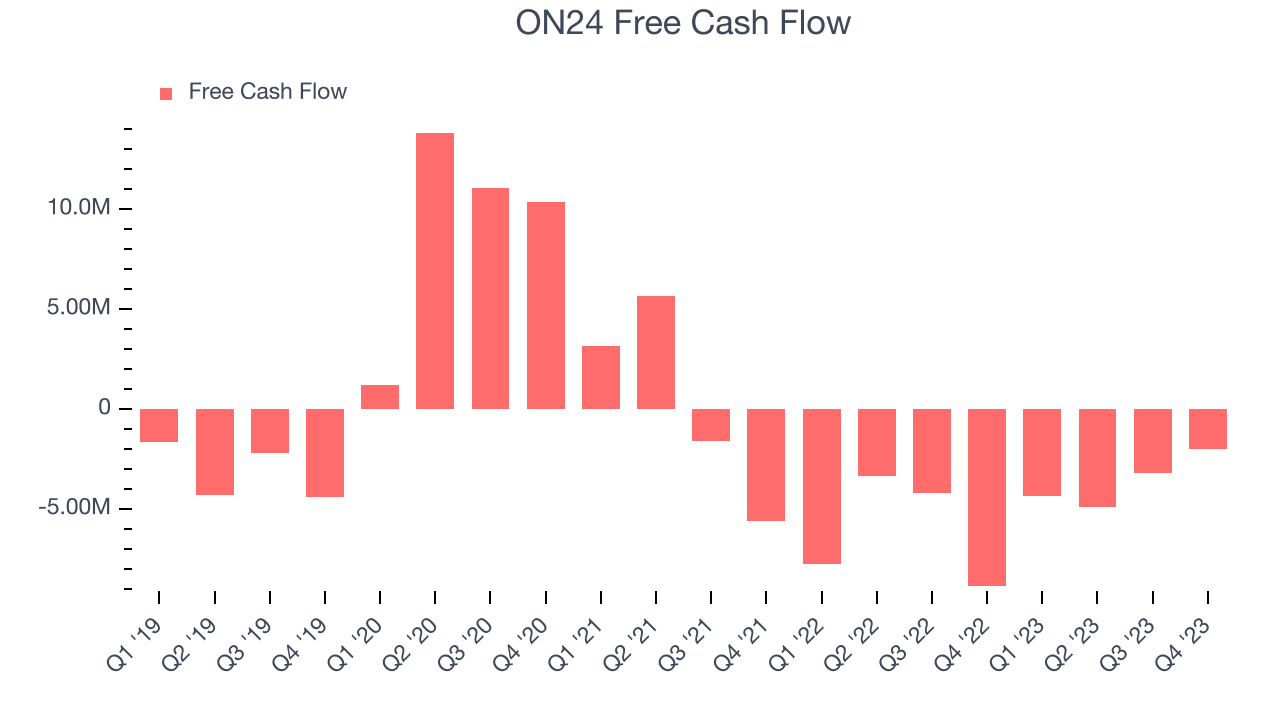

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. ON24 burned through $1.97 million of cash in Q4, decreasing its cash burn by 77.8% year on year.

ON24 has burned through $14.39 million of cash over the last 12 months, resulting in a negative 8.8% free cash flow margin. This low FCF margin stems from ON24's constant need to reinvest in its business to stay competitive.

Key Takeaways from ON24's Q4 Results

ON24's revenue continues to shrink, while the company keeps burning cash. But it was good to see that the cash burn is slowing down, on the other hand, its full-year revenue guidance was below expectations. Zooming out, we think this was still mixed quarter. The stock is flat after reporting and currently trades at $7.7 per share.

Is Now The Time?

When considering an investment in ON24, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in case of ON24, we'll be cheering from the sidelines. Its revenue has has been declining, and analysts expect growth to deteriorate from here. And while its strong gross margins suggest it can operate profitably and sustainably, the downside is its customer acquisition is less efficient than many comparable companies. On top of that, its operations are coming at a cost of significant cash burn.

ON24's price-to-sales ratio based on the next 12 months is 2.2x, suggesting that the market does have lower expectations of the business, relative to the high growth tech stocks. While we have no doubt one can find things to like about the company, and the price is not completely unreasonable, we think that at the moment there might be better opportunities in the market.

Wall Street analysts covering the company had a one-year price target of $9 per share right before these results (compared to the current share price of $7.70).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.