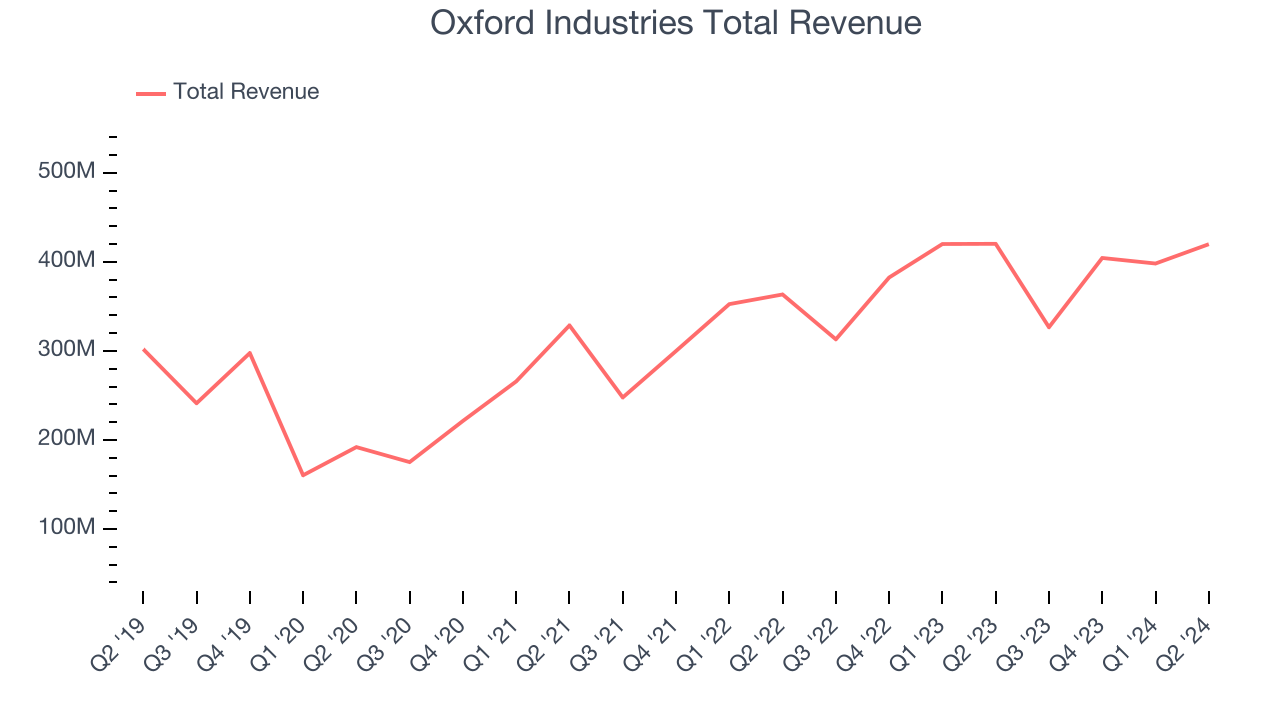

Fashion conglomerate Oxford Industries (NYSE:OXM) missed analysts’ expectations in Q2 CY2024, with revenue flat year on year at $419.9 million. Next quarter’s revenue guidance of $317.5 million also underwhelmed, coming in 9.9% below analysts’ estimates. It made a non-GAAP profit of $2.77 per share, down from its profit of $3.45 per share in the same quarter last year.

Is now the time to buy Oxford Industries? Find out by accessing our full research report, it’s free.

Oxford Industries (OXM) Q2 CY2024 Highlights:

- Revenue: $419.9 million vs analyst estimates of $438.2 million (4.2% miss)

- EPS (non-GAAP): $2.77 vs analyst expectations of $3.00 (7.8% miss)

- The company dropped its revenue guidance for the full year to $1.53 billion at the midpoint from $1.61 billion, a 5.3% decrease

- EPS (non-GAAP) guidance for the full year is $7.15 at the midpoint, missing analyst estimates by 17.4%

- Gross Margin (GAAP): 63.1%, in line with the same quarter last year

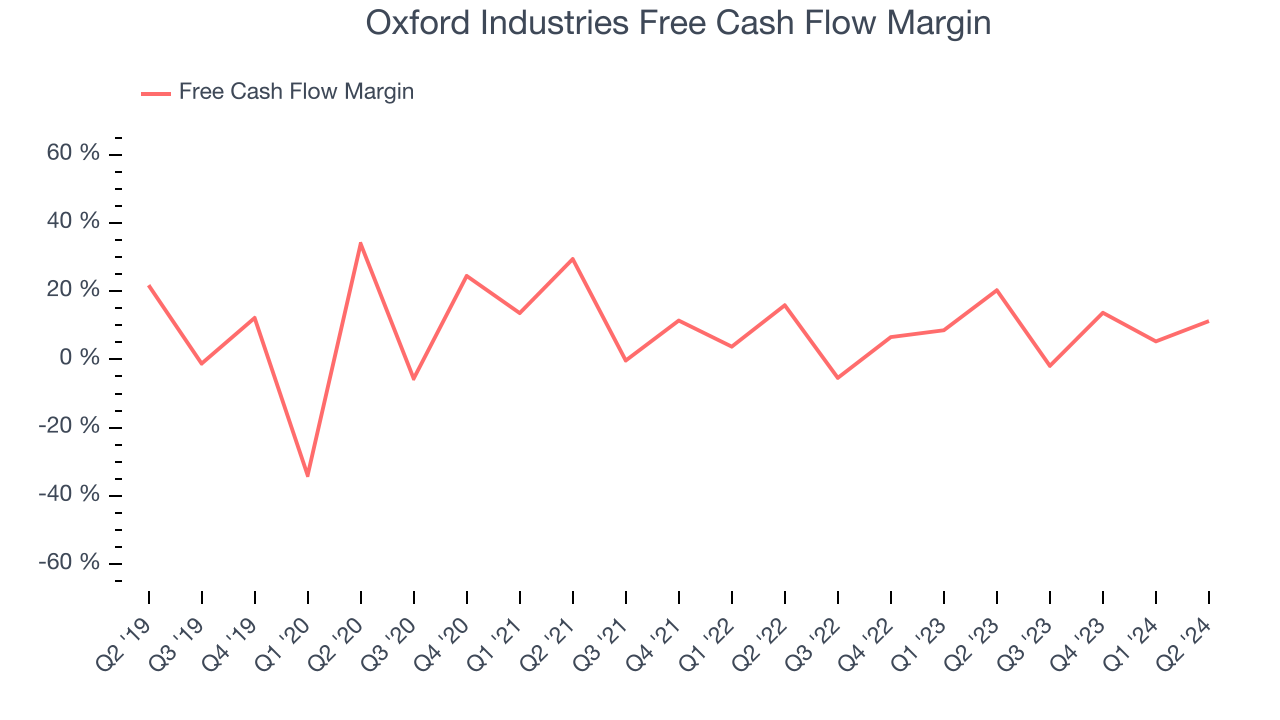

- Free Cash Flow Margin: 11.2%, down from 20.3% in the same quarter last year

- Market Capitalization: $1.31 billion

Tom Chubb, Chairman and CEO, commented, “Consumer sentiment in the second quarter continued to decline from levels earlier in the year reaching an eight month low in July. The decline led to market conditions that were weaker than expected with more consumers looking for deals and promotions as evidenced by increased sales in our outlet locations and during promotional events. Despite the challenging consumer environment, our teams continue to focus on our strategy of delivering new and compelling products and experiences for our customers. The current macroeconomic environment does not diminish our enthusiasm or commitment to our strategy to drive long-term shareholder value.

The parent company of Tommy Bahama, Oxford Industries (NYSE:OXM) is a lifestyle fashion conglomerate with brands that embody outdoor happiness.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Oxford Industries grew its sales at a weak 6.8% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Oxford Industries’s annualized revenue growth of 10.7% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Oxford Industries missed Wall Street’s estimates and reported a rather uninspiring 0.1% year-on-year revenue decline, generating $419.9 million of revenue. The company is guiding for a 2.8% year-on-year revenue decline next quarter to $317.5 million, a reversal from the 4.3% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 6.1% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Oxford Industries has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8%, subpar for a consumer discretionary business.

Oxford Industries’s free cash flow clocked in at $47.18 million in Q2, equivalent to a 11.2% margin. The company’s cash profitability regressed as it was 9 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends trump temporary fluctuations.

Key Takeaways from Oxford Industries’s Q2 Results

We struggled to find many strong positives in these results. Its full-year revenue guidance missed and its full-year earnings guidance fell short of Wall Street’s estimates. Overall, this was a mediocre quarter. The stock traded down 7.1% to $77.65 immediately after reporting.

Oxford Industries may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.