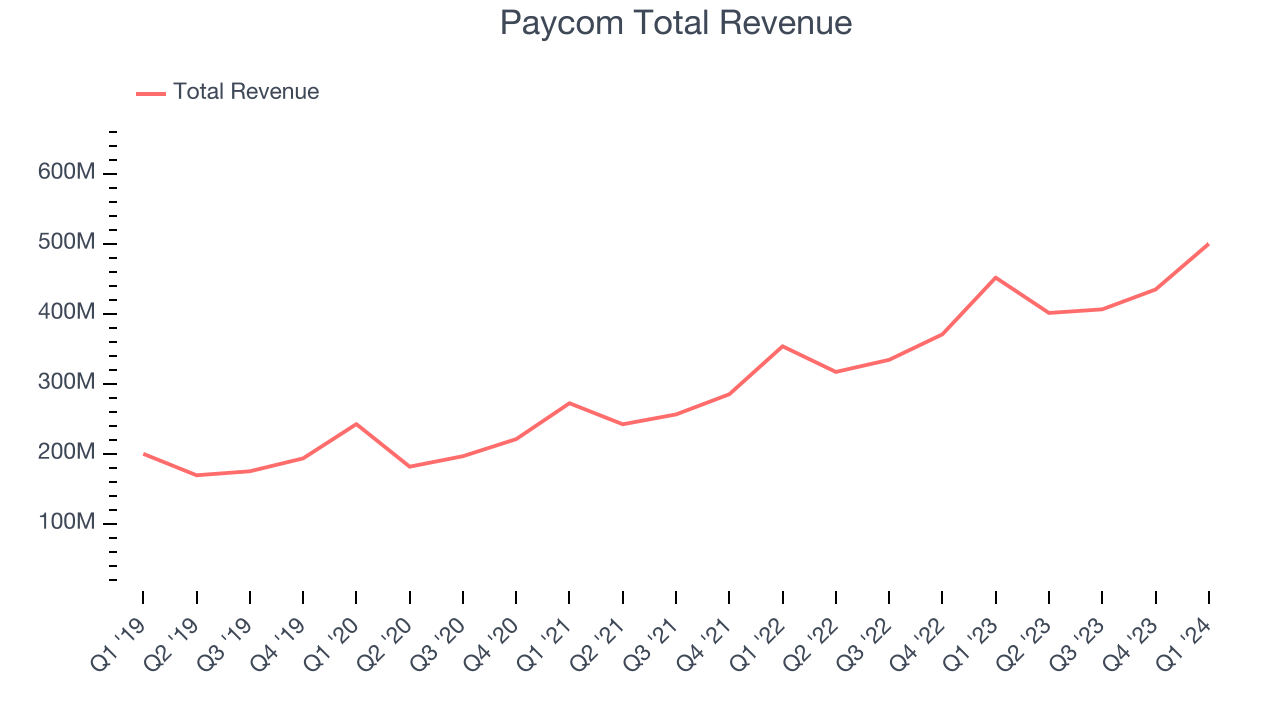

Online payroll and human resource software provider Paycom (NYSE:PAYC) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 10.7% year on year to $499.9 million. On the other hand, next quarter's revenue guidance of $436 million was less impressive, coming in 1.4% below analysts' estimates. It made a non-GAAP profit of $2.59 per share, improving from its profit of $2.46 per share in the same quarter last year.

Is now the time to buy Paycom? Find out by accessing our full research report, it's free.

Paycom (PAYC) Q1 CY2024 Highlights:

- Revenue: $499.9 million vs analyst estimates of $496.2 million (small beat)

- EPS (non-GAAP): $2.59 vs analyst estimates of $2.47 (4.9% beat)

- Revenue Guidance for Q2 CY2024 is $436 million at the midpoint, below analyst estimates of $442.1 million

- The company reconfirmed its revenue guidance for the full year of $1.87 billion at the midpoint

- Gross Margin (GAAP): 84.3%, down from 88.2% in the same quarter last year

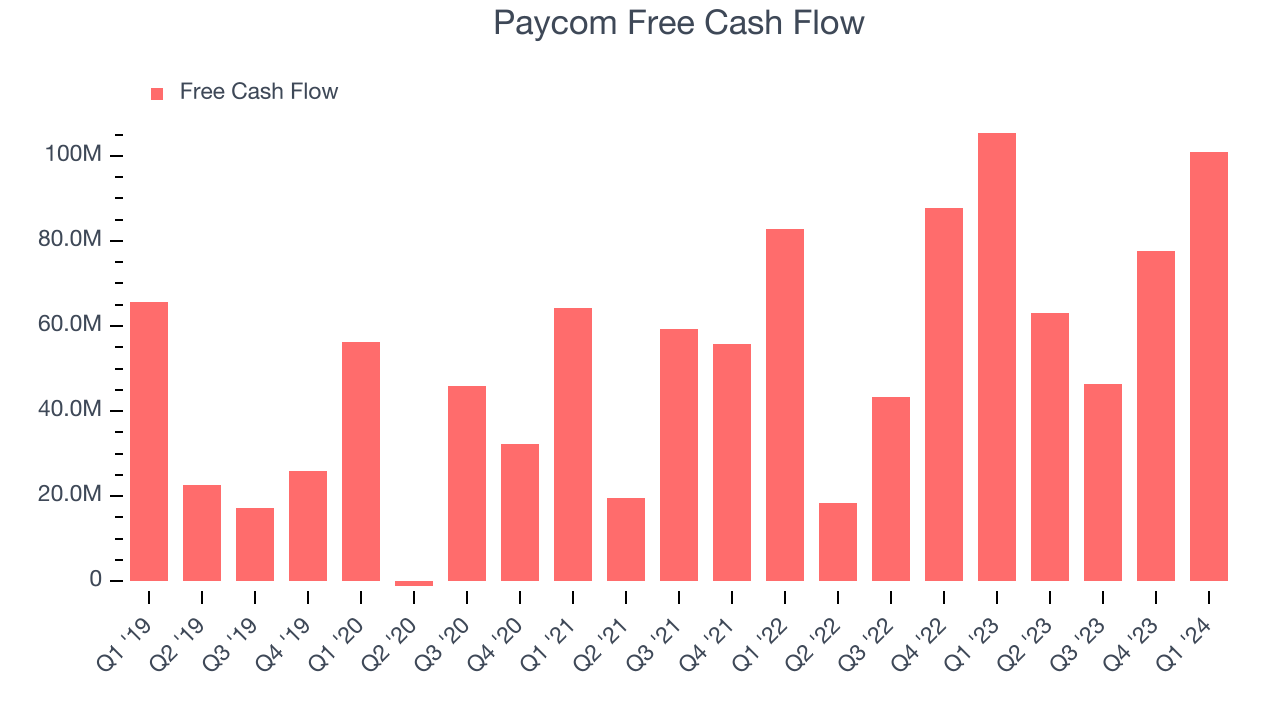

- Free Cash Flow of $100.9 million, up 30.1% from the previous quarter

- Market Capitalization: $10.74 billion

“Led by Beti and our differentiated product strategy, we continue to deliver value to businesses that leverage HCM automation, while simplifying the lives of employees and HR teams across the globe,” said Paycom's founder, Co-CEO, President and Chairman, Chad Richison.

Founded in 1998 as one of the first online payroll companies, Paycom (NYSE:PAYC) provides software for small and medium-sized businesses (SMBs) to manage their payroll and HR needs in one place.

HR Software

Modern HR software has two powerful benefits: cost savings and ease of use. For cost savings, businesses large and small much prefer the flexibility of cloud-based, web-browser-delivered software paid for on a subscription basis rather than the hassle and complexity of purchasing and managing on-premise enterprise software. On the usability side, the consumerization of business software creates seamless experiences whereby multiple standalone processes like payroll processing and compliance are aggregated into a single, easy-to-use platform.

Sales Growth

As you can see below, Paycom's revenue growth has been strong over the last three years, growing from $272.2 million in Q1 2021 to $499.9 million this quarter.

This quarter, Paycom's quarterly revenue was once again up 10.7% year on year. We can see that Paycom's revenue increased by $65.29 million quarter on quarter, which is a solid improvement from the $28.29 million increase in Q4 CY2023. Shareholders should applaud the re-acceleration of growth.

Next quarter's guidance suggests that Paycom is expecting revenue to grow 8.7% year on year to $436 million, slowing down from the 26.6% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.9% over the next 12 months before the earnings results announcement.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Paycom's free cash flow came in at $100.9 million in Q1, roughly the same as last year.

Paycom has generated $287.9 million in free cash flow over the last 12 months, a solid 16.5% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from Paycom's Q1 Results

It was good to see Paycom beat analysts' billings expectations this quarter. On the other hand, its revenue guidance for next quarter missed analysts' expectations and its gross margin decreased. Overall, this was a mediocre quarter for Paycom. The company is down 9.3% on the results and currently trades at $169 per share.

Paycom may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.