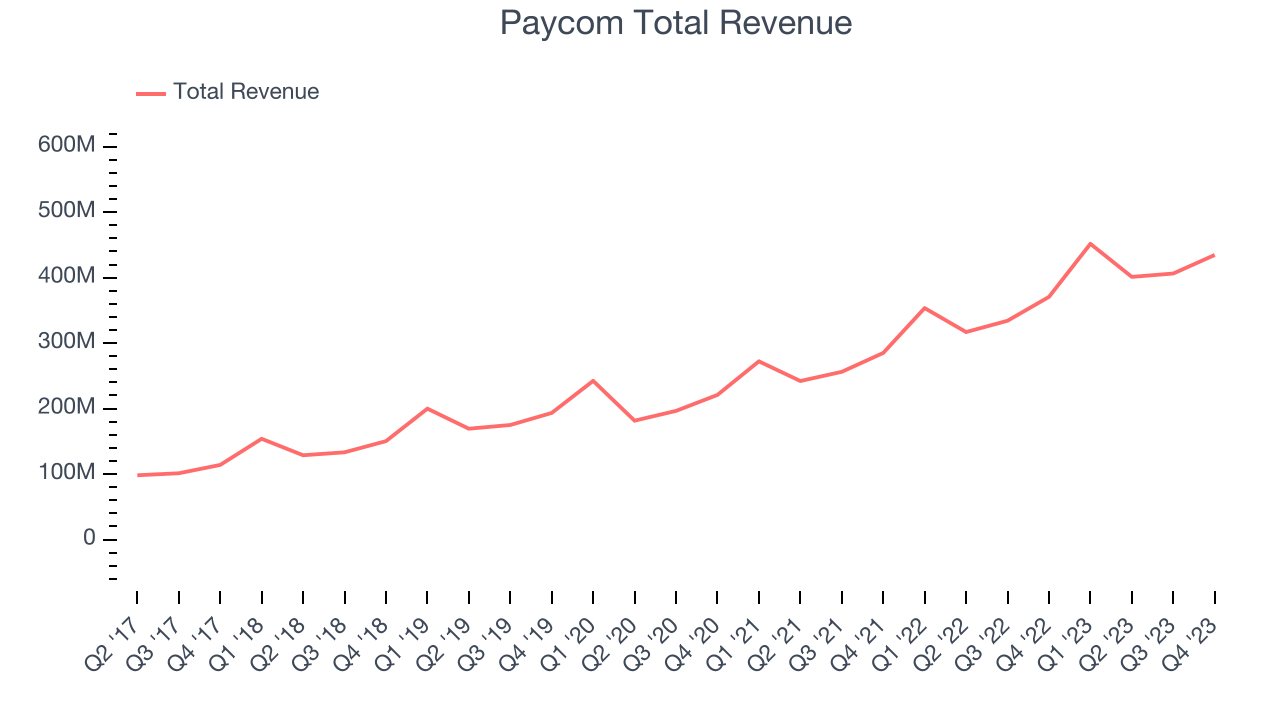

Online payroll and human resource software provider Paycom (NYSE:PAYC) reported Q4 FY2023 results beating Wall Street analysts' expectations, with revenue up 17.3% year on year to $434.6 million. On the other hand, the company expects next quarter's revenue to be around $495.5 million, slightly below analysts' estimates. It made a non-GAAP profit of $1.93 per share, improving from its profit of $1.73 per share in the same quarter last year.

Paycom (PAYC) Q4 FY2023 Highlights:

- Revenue: $434.6 million vs analyst estimates of $422.3 million (2.9% beat)

- EPS (non-GAAP): $1.93 vs analyst estimates of $1.78 (8.5% beat)

- Revenue Guidance for Q1 2024 is $495.5 million at the midpoint, below analyst estimates of $499.6 million

- Management's revenue guidance for the upcoming financial year 2024 is $1.87 billion at the midpoint, in line with analyst expectations and implying 10.6% growth (vs 23.3% in FY2023)

- Free Cash Flow of $77.59 million, up 67.5% from the previous quarter

- Gross Margin (GAAP): 82.8%, down from 87.2% in the same quarter last year

- Market Capitalization: $11.41 billion

Founded in 1998 as one of the first online payroll companies, Paycom (NYSE:PAYC) provides software for small and medium-sized businesses (SMBs) to manage their payroll and HR needs in one place.

Human Capital Management (HCM) software is meant to streamline mundane, but vital, business functions like keeping attendance, running payroll, and keeping compliant with shifting Federal and local government taxes and labor laws. For many small and medium sized businesses, these are often handled by their accountant which is an unnecessarily expensive use of resources, or QuickBooks style spreadsheets which don’t have sufficient functionality.

Using a single database or system of records, Paycom is a cost effective solution that allows SMBs to simplify the management of all their HR operations throughout an employee’s lifecycle, from when they first apply for a job, to onboarding and managing performance reviews, all the way through collecting retirement benefits.

Paycom has useful functionality that differentiates it from rivals, in part because the company regularly iterates its platform based on customer feedback. One example is that HR managers can automatically share open positions to career sites, which funnels qualified applicants back to the company to easily schedule interviews and conduct background checks. Another is the ability for businesses to conduct self evaluations based on analytics that pull together performance reviews and other HR data from across the company.

HR Software

Modern HR software has two powerful benefits: cost savings and ease of use. For cost savings, businesses large and small much prefer the flexibility of cloud-based, web-browser-delivered software paid for on a subscription basis rather than the hassle and complexity of purchasing and managing on-premise enterprise software. On the usability side, the consumerization of business software creates seamless experiences whereby multiple standalone processes like payroll processing and compliance are aggregated into a single, easy-to-use platform.

Other providers of HR solutions for small and medium-sized businesses include Paychex (NASDAQ:PAYX), ADP (NASDAQ:ADP), Asure, (NYSE:ASUR) and Paylocity (NASDAQ:PCTY).

Sales Growth

As you can see below, Paycom's revenue growth has been strong over the last two years, growing from $285 million in Q4 FY2021 to $434.6 million this quarter.

This quarter, Paycom's quarterly revenue was once again up 17.3% year on year. We can see that Paycom's revenue increased by $28.29 million quarter on quarter, which is a solid improvement from the $5.16 million increase in Q3 2023. Shareholders should applaud the re-acceleration of growth.

Next quarter's guidance suggests that Paycom is expecting revenue to grow 9.7% year on year to $495.5 million, slowing down from the 27.8% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $1.87 billion at the midpoint, growing 10.6% year on year compared to the 23.2% increase in FY2023.

Profitability

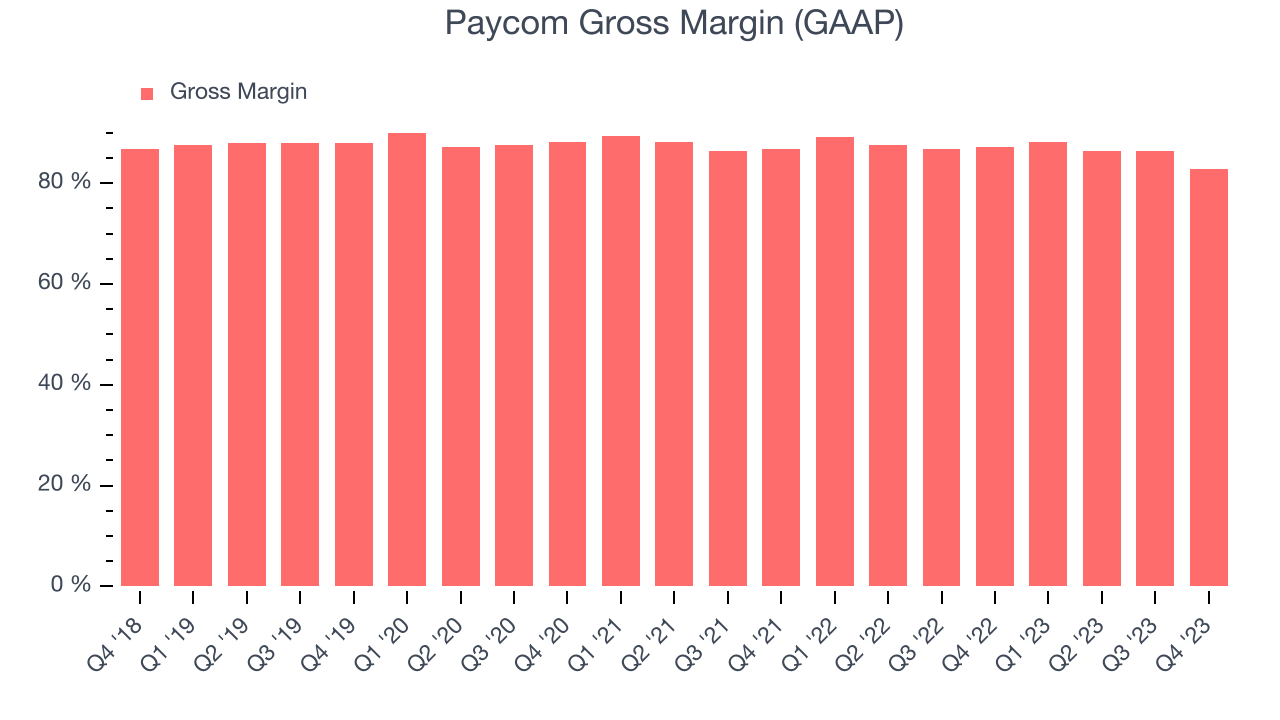

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Paycom's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 82.8% in Q4.

That means that for every $1 in revenue the company had $0.83 left to spend on developing new products, sales and marketing, and general administrative overhead. Despite its decline over the last year, Paycom's excellent gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity.

Cash Is King

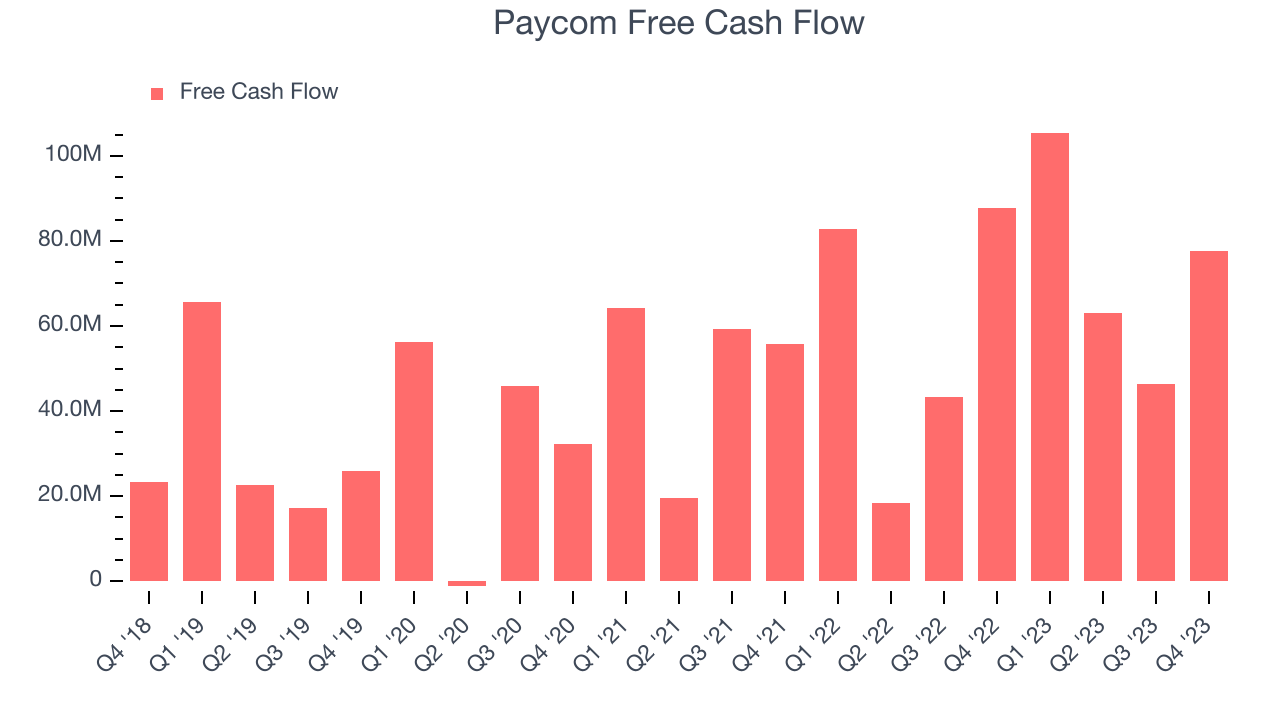

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Paycom's free cash flow came in at $77.59 million in Q4, down 11.6% year on year.

Paycom has generated $292.5 million in free cash flow over the last 12 months, a solid 17.1% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from Paycom's Q4 Results

It was good to see Paycom beat analysts' revenue expectations this quarter. That stood out as a positive in these results. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and its revenue guidance for next quarter missed Wall Street's estimates. Overall, the results could have been better. The company is down 4.5% on the results and currently trades at $190 per share.

Is Now The Time?

When considering an investment in Paycom, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although we have other favorites, we understand the arguments that Paycom isn't a bad business. We'd expect growth rates to moderate from here, but its revenue growth has been solid over the last two years. On top of that, its impressive gross margins indicate excellent business economics.

The market is certainly expecting long-term growth from Paycom given its price-to-sales ratio based on the next 12 months is 6.1x. There are things to like about Paycom and there's no doubt it's a bit of a market darling, at least for some. But we are wondering whether there might be better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $204.22 per share right before these results (compared to the current share price of $190).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.