IT incident response platform PagerDuty (NYSE:PD) reported results in line with analyst expectations in Q1 FY2024 quarter, with revenue up 20.9% year on year to $103.2 million. However, guidance for the next quarter was less impressive, coming in at $104.5 million at the midpoint, being 3.78% below analyst estimates. PagerDuty made a GAAP loss of $12.8 million, improving on its loss of $32.8 million, in the same quarter last year.

Is now the time to buy PagerDuty? Access our full analysis of the earnings results here, it's free.

PagerDuty (PD) Q1 FY2024 Highlights:

- Revenue: $103.2 million vs analyst estimates of $102.9 million (small beat)

- EPS (non-GAAP): $0.20 vs analyst estimates of $0.09 ($0.11 beat)

- Revenue guidance for Q2 2024 is $104.5 million at the midpoint, below analyst estimates of $108.6 million

- The company dropped revenue guidance for the full year, from $449 million to $427.5 million at the midpoint, a 4.79% decrease

- Free cash flow of $20.8 million, up 33.8% from previous quarter

- Customers: 15,089, down from 15,244 in previous quarter

- Gross Margin (GAAP): 82.6%, up from 81.6% same quarter last year

“PagerDuty demonstrated balanced growth in Q1 with solid revenue growth of 21% and record 16% non-GAAP operating margin—up 1,800 basis points with 20% free cash flow margin,” said Jennifer Tejada, Chairperson and CEO, PagerDuty.

Started by three former Amazon engineers, PagerDuty (NYSE:PD) is a software as a service platform that helps companies respond to IT incidents fast and make sure that any downtime is minimized.

Software is eating the world, increasing organizations’ reliance on digital-only solutions. As more workloads and applications move to the cloud, the reliability of the underlying cloud infrastructure becomes ever more critical, and ever more complex. To solve the challenge, companies and their engineering teams have turned to a range of cloud monitoring tools that provide them with visibility to troubleshoot the issues in real time.

Sales Growth

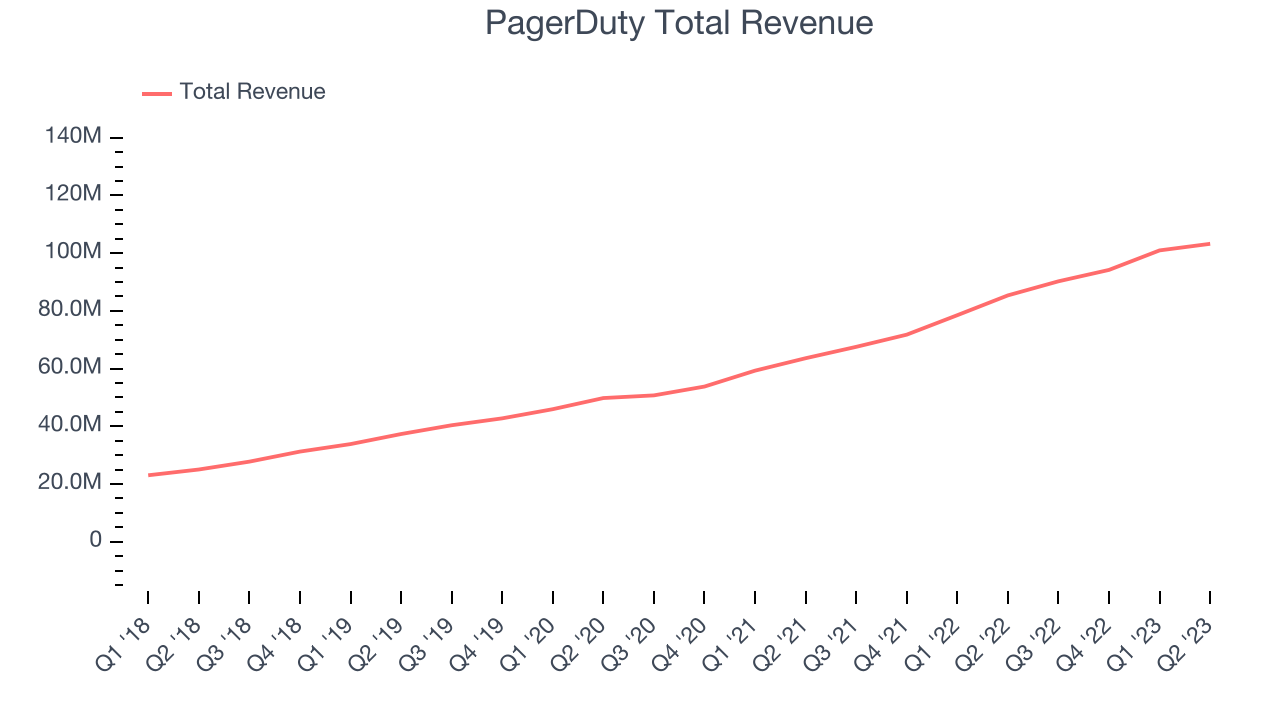

As you can see below, PagerDuty's revenue growth has been very strong over the last two years, growing from quarterly revenue of $63.6 million in Q1 FY2022, to $103.2 million.

This quarter, PagerDuty's quarterly revenue was once again up a very solid 20.9% year on year. But the growth did slow down compared to last quarter, as the revenue increased by just $2.28 million in Q1, compared to $6.76 million in Q4 2023. We'd like to see revenue increase by a greater amount each quarter, but a one-off fluctuation is usually not concerning.

Guidance for the next quarter indicates PagerDuty is expecting revenue to grow 15.8% year on year to $104.5 million, slowing down from the 33.6% year-over-year increase in revenue the company had recorded in the same quarter last year. Ahead of the earnings results the analysts covering the company were estimating sales to grow 21.3% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

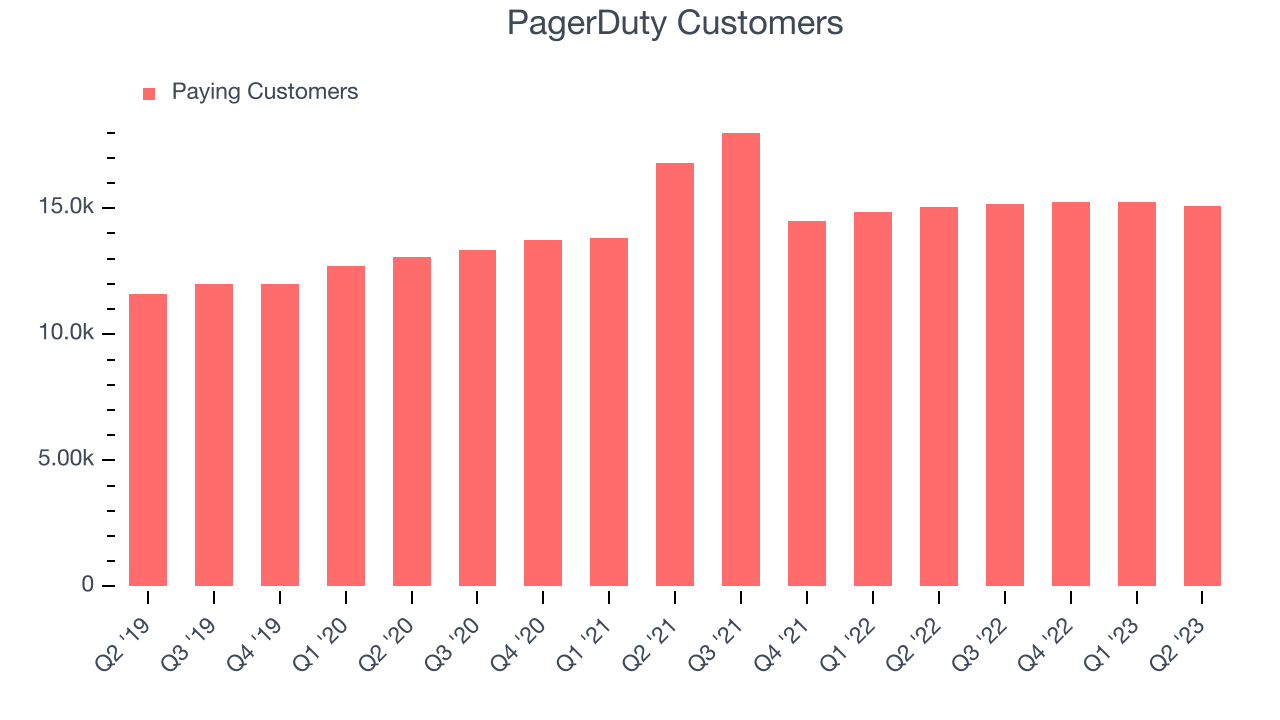

Customer Growth

You can see below that PagerDuty reported 15,089 customers at the end of the quarter, a decrease of 155 on last quarter. That is slower customer growth than what we are used to seeing lately, suggesting that the customer acquisition momentum is slowing down.

Key Takeaways from PagerDuty's Q1 Results

With a market capitalization of $2.51 billion PagerDuty is among smaller companies, but its more than $495.1 million in cash and positive free cash flow over the last twelve months put it in a very strong position to invest in growth.

We struggled to find many strong positives in these results. It was unfortunate to see that PagerDuty's revenue guidance for the full year missed analysts' expectations and the revenue guidance for the next quarter missed analysts' expectations. Overall, it seems to us that this was a complicated quarter for PagerDuty. The company is down 15.3% on the results and currently trades at $23.5 per share.

PagerDuty may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.