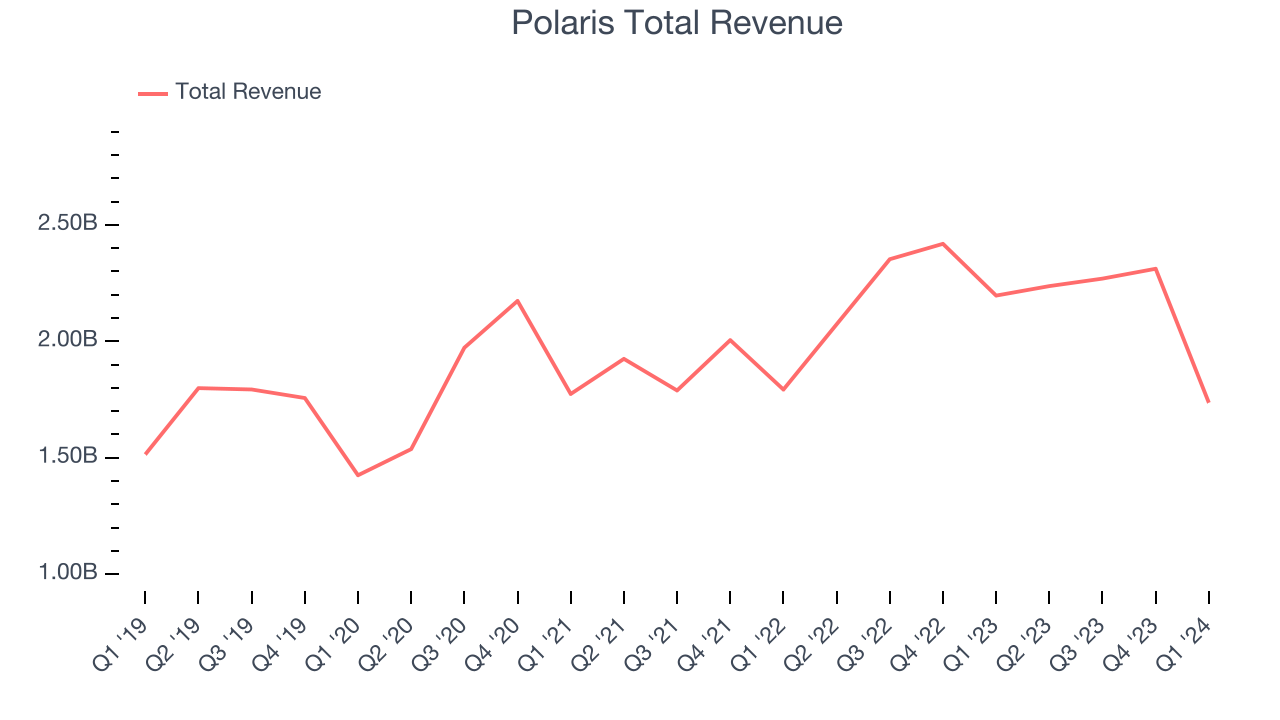

Off-Road and powersports vehicle corporation Polaris (NYSE:PII) missed analysts' expectations in Q1 CY2024, with revenue down 20.9% year on year to $1.74 billion. It made a GAAP profit of $0.07 per share, down from its profit of $1.95 per share in the same quarter last year.

Is now the time to buy Polaris? Find out by accessing our full research report, it's free.

Polaris (PII) Q1 CY2024 Highlights:

- Revenue: $1.74 billion vs analyst estimates of $1.75 billion (0.6% miss)

- EPS: $0.07 vs analyst expectations of $0.10 (29.5% miss)

- Full year guidance reiterated from previous

- Gross Margin (GAAP): 19%, down from 22.1% in the same quarter last year

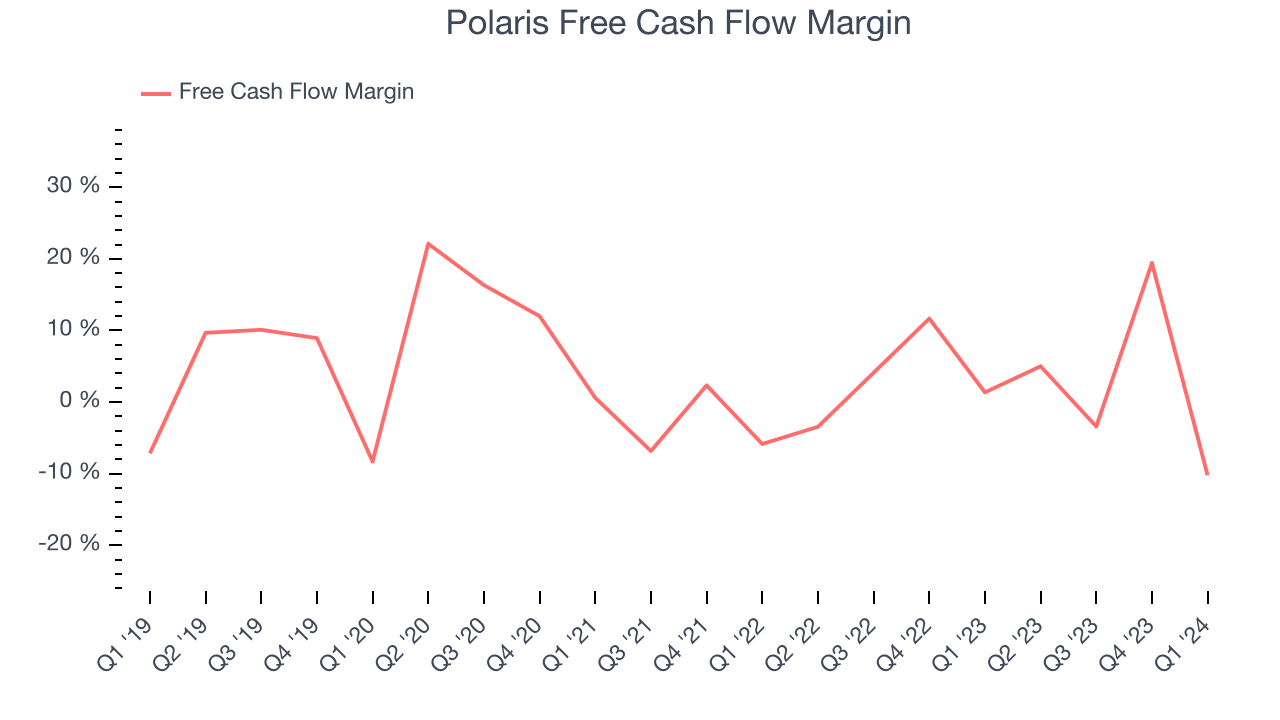

- Free Cash Flow was -$177.5 million, down from $448.9 million in the previous quarter

- Market Capitalization: $4.98 billion

Founded in 1954, Polaris (NYSE:PII) designs and manufactures high-performance off-road vehicles, snowmobiles, and motorcycles.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Polaris's annualized revenue growth rate of 5.5% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Polaris's annualized revenue growth of 6.7% over the last two years is above its five-year trend, suggesting some bright spots.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Polaris's annualized revenue growth of 6.7% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Polaris missed Wall Street's estimates and reported a rather uninspiring 20.9% year-on-year revenue decline, generating $1.74 billion of revenue. Looking ahead, Wall Street expects revenue to decline 1% over the next 12 months.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Polaris has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 3.7%, subpar for a consumer discretionary business.

Polaris burned through $177.5 million of cash in Q1, equivalent to a negative 10.2% margin. This caught our eye as the company shifted from cash flow positive in the same quarter last year to cash flow negative this quarter.

Key Takeaways from Polaris's Q1 Results

Revenue and EPS missed this quarter. On a brighter note, the company reiterated its previous full year guidance. Management stated that the company "gained share in ORV, motorcycles and Marine, and the recent launches in our best-selling full-size RANGER and Indian Scout lineups reflect our strategic focus on Rider-Driven Innovation". Overall, the results could have been better. The company is down 2.3% on the results and currently trades at $86.21 per share.

So should you invest in Polaris right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.