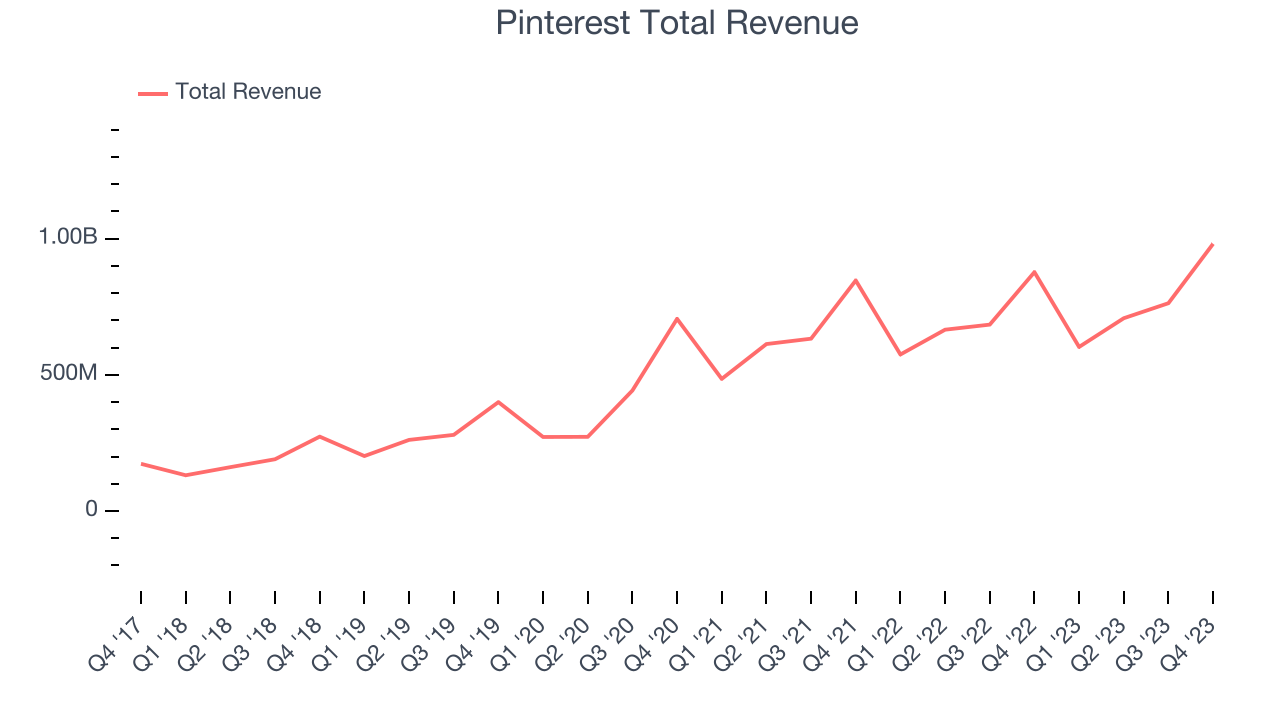

Social commerce platform Pinterest (NYSE: PINS) missed analysts' expectations in Q4 FY2023, with revenue up 11.9% year on year to $981.3 million. It made a non-GAAP profit of $0.53 per share, improving from its profit of $0.29 per share in the same quarter last year.

Is now the time to buy Pinterest? Find out by accessing our full research report, it's free.

Pinterest (PINS) Q4 FY2023 Highlights:

- Revenue: $981.3 million vs analyst estimates of $990.2 million (0.9% miss)

- Revenue guidance for Q1 2024: $698 million vs analyst estimates of $703 million (0.7% miss)

- EPS (non-GAAP): $0.53 vs analyst estimates of $0.51 (3.3% beat)

- Free Cash Flow of $254 million, up 136% from the previous quarter

- Gross Margin (GAAP): 81.9%, up from 79.3% in the same quarter last year

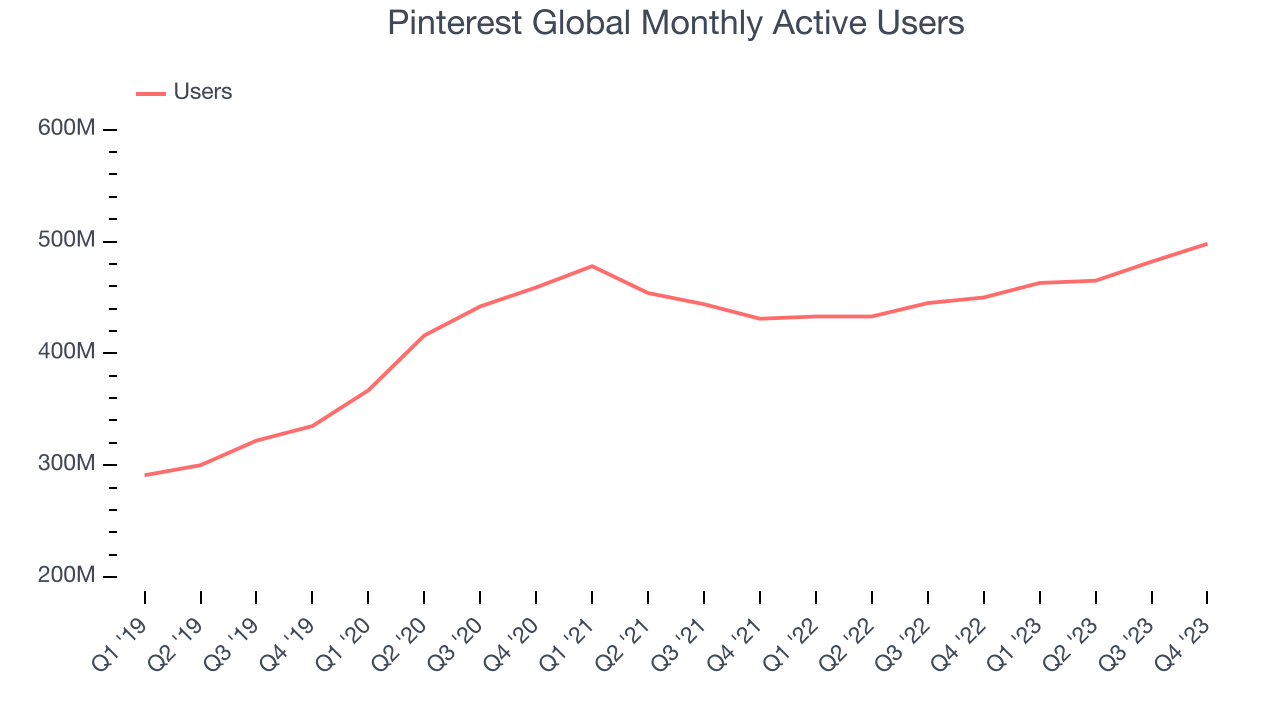

- Global Monthly Active Users: 498 million, up 48 million year on year (beat vs. expectations of 488 million)

- Market Capitalization: $27.53 billion

“We had a strong Q4, bookending a transformative year for Pinterest,” said Bill Ready, CEO of Pinterest.

Created with the idea of virtually replacing paper catalogues, Pinterest (NYSE: PINS) is an online image and social discovery platform.

Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Sales Growth

Pinterest's revenue growth over the last three years has been strong, averaging 28.3% annually. This quarter, Pinterest reported mediocre 11.9% year-on-year revenue growth, missing Wall Street's expectations.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Usage Growth

As a social network, Pinterest generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Pinterest's monthly active users, a key performance metric for the company, grew 3% annually to 498 million. This is one of the lowest rates of growth in the consumer internet sector.

In Q4, Pinterest added 48 million monthly active users, translating into 10.7% year-on-year growth.

Revenue Per User

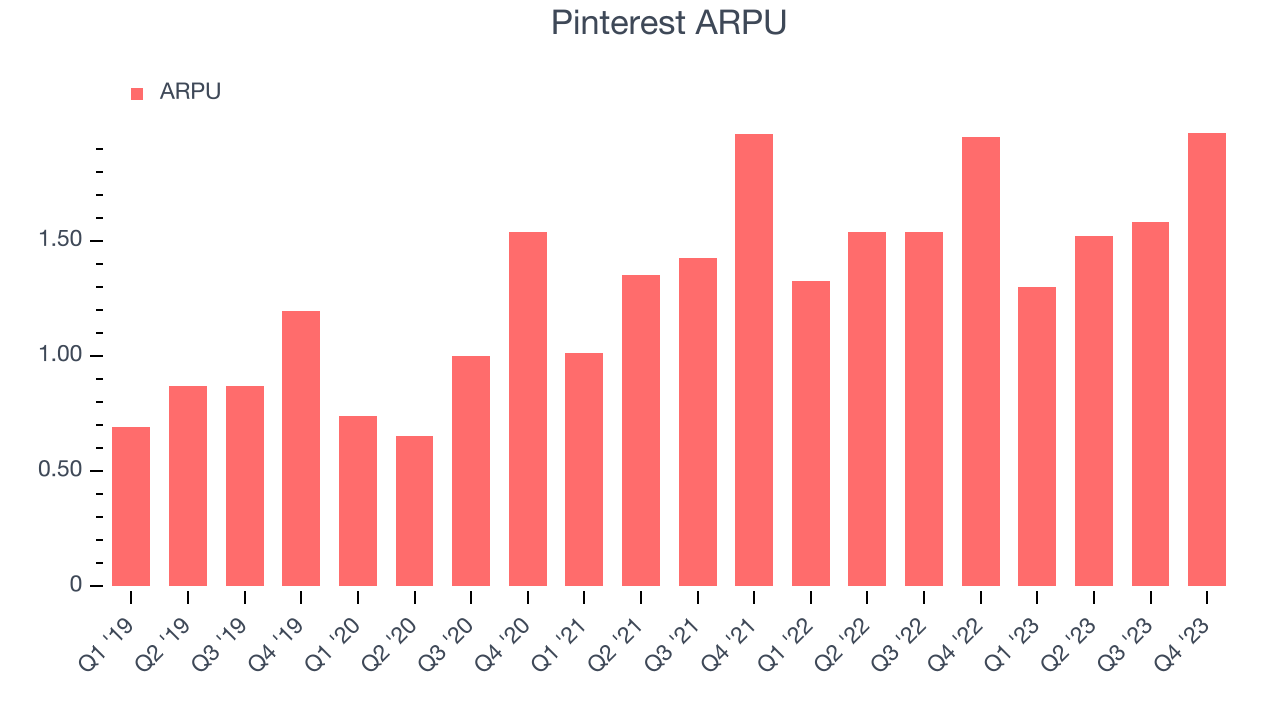

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Pinterest because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Pinterest's audience and its ad-targeting capabilities.

Pinterest's ARPU growth has been decent over the last two years, averaging 6.6%. The company's ability to increase prices while growing its monthly active users demonstrates the value of its platform. This quarter, ARPU grew 1.1% year on year to $1.97 per user.

Key Takeaways from Pinterest's Q4 Results

It was good to see Pinterest add new users this quarter and beat expectations for MAUs (monthly active users). That stood out as a positive in these results. On the other hand, its revenue unfortunately missed analysts' expectations and its revenue growth stalled. Revenue guidance for the next quarter also fell below expectations. Overall, this was a mediocre quarter for Pinterest. The company is down 21.4% on the results and currently trades at $32.02 per share.

Pinterest may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.