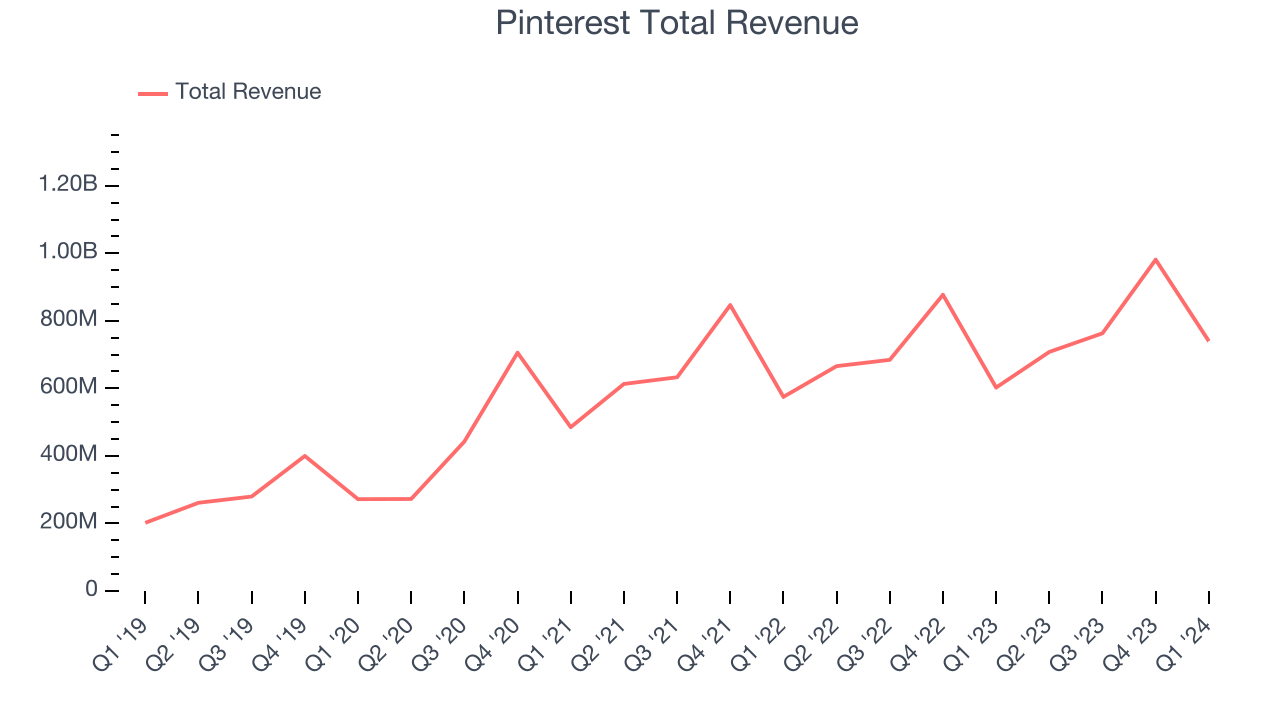

Social commerce platform Pinterest (NYSE: PINS) reported Q1 CY2024 results exceeding Wall Street analysts' expectations, with revenue up 22.8% year on year to $740 million. Guidance for next quarter's revenue was also better than expected at $842.5 million at the midpoint, 1.9% above analysts' estimates. It made a non-GAAP profit of $0.20 per share, improving from its profit of $0.09 per share in the same quarter last year.

Pinterest (PINS) Q1 CY2024 Highlights:

- Revenue: $740 million vs analyst estimates of $700.1 million (5.7% beat)

- EPS (non-GAAP): $0.20 vs analyst estimates of $0.13 (48.8% beat)

- Revenue Guidance for Q2 CY2024 is $842.5 million at the midpoint, above analyst estimates of $827.1 million (implied operating profit also well ahead of expectations)

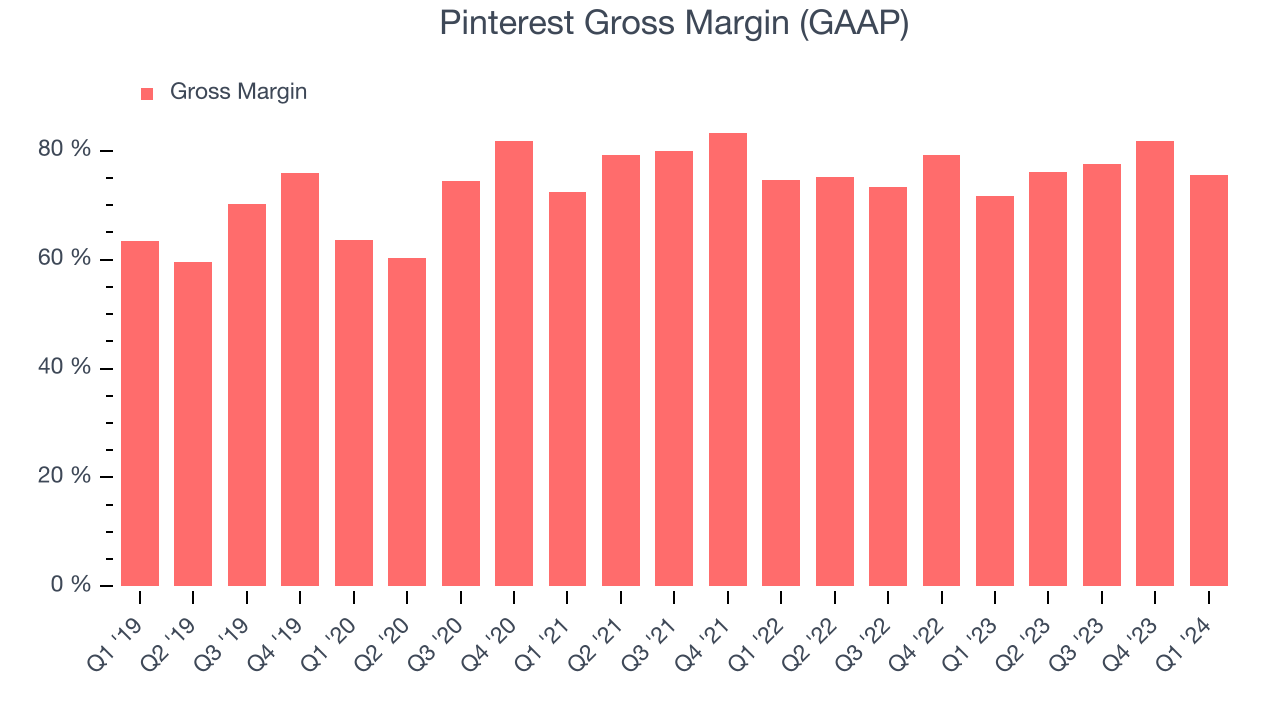

- Gross Margin (GAAP): 75.5%, up from 71.6% in the same quarter last year

- Free Cash Flow of $344 million, up 35.4% from the previous quarter (large beat)

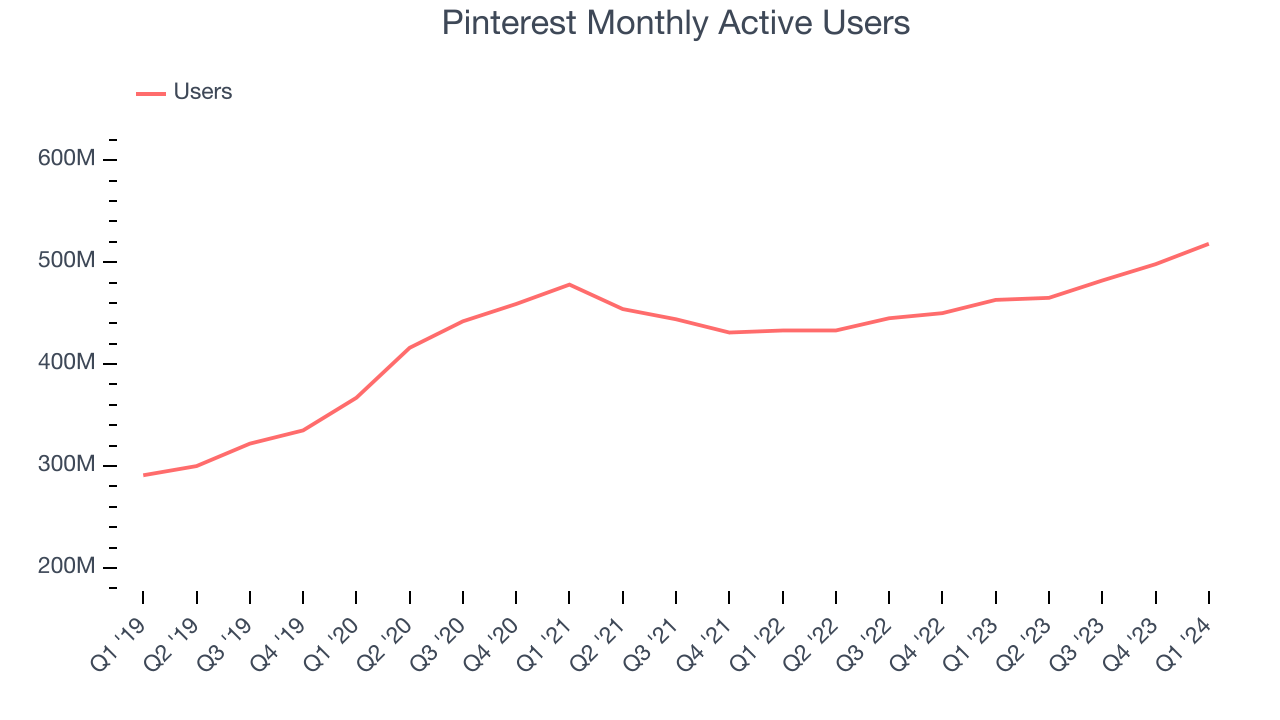

- Monthly Active Users: 518 million, up 55 million year on year (2.6% beat vs. expectations of 505 million)

- Market Capitalization: $23.06 billion

Created with the idea of virtually replacing paper catalogues, Pinterest (NYSE: PINS) is an online image and social discovery platform.

Pinterest is an online content and visual discovery platform that allows its users to create personalized collections of curated design or inspiration ideas while also providing recommendations based on a user’s personal interests. One part search engine and one part media platform, Pinterest is a hybrid of ecommerce and social media platform. For its users, most of which are female, Pinterest is a platform that offers discovery of items such as recipes, fashion, and home goods, and does so in an aspirational social media like use case.

For advertisers, Pinterest’s scale of hundreds of million monthly users is a valuable platform to target advertising where users innately are actively moving from ideation to purchasing, which is exactly where advertisers most like to insert themselves, when a potential customer is showing buying intent. As a bonus, unlike other social media platforms, advertising on Pinterest is content, a unique situation for advertisers.

Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Pinterest (NASDAQ: PINS) competes with fellow social media advertising platforms like Google (NASDAQ: GOOGL), Meta Platforms (NASDAQ:FB), Snapchat (NYSE: SNAP), and Twitter (NYSE: TWTR).

Sales Growth

Pinterest's revenue growth over the last three years has been strong, averaging 23.7% annually. This quarter, Pinterest beat analysts' estimates and reported decent 22.8% year-on-year revenue growth.

Guidance for the next quarter indicates Pinterest is expecting revenue to grow 19% year on year to $842.5 million, improving from the 6.3% year-on-year increase it recorded in the comparable quarter last year. Ahead of the earnings results, analysts were projecting sales to grow 15.7% over the next 12 months.

Usage Growth

As a social network, Pinterest generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Pinterest's monthly active users, a key performance metric for the company, grew 5.6% annually to 518 million. This is average growth for a consumer internet company.

In Q1, Pinterest added 55 million monthly active users, translating into 11.9% year-on-year growth.

Revenue Per User

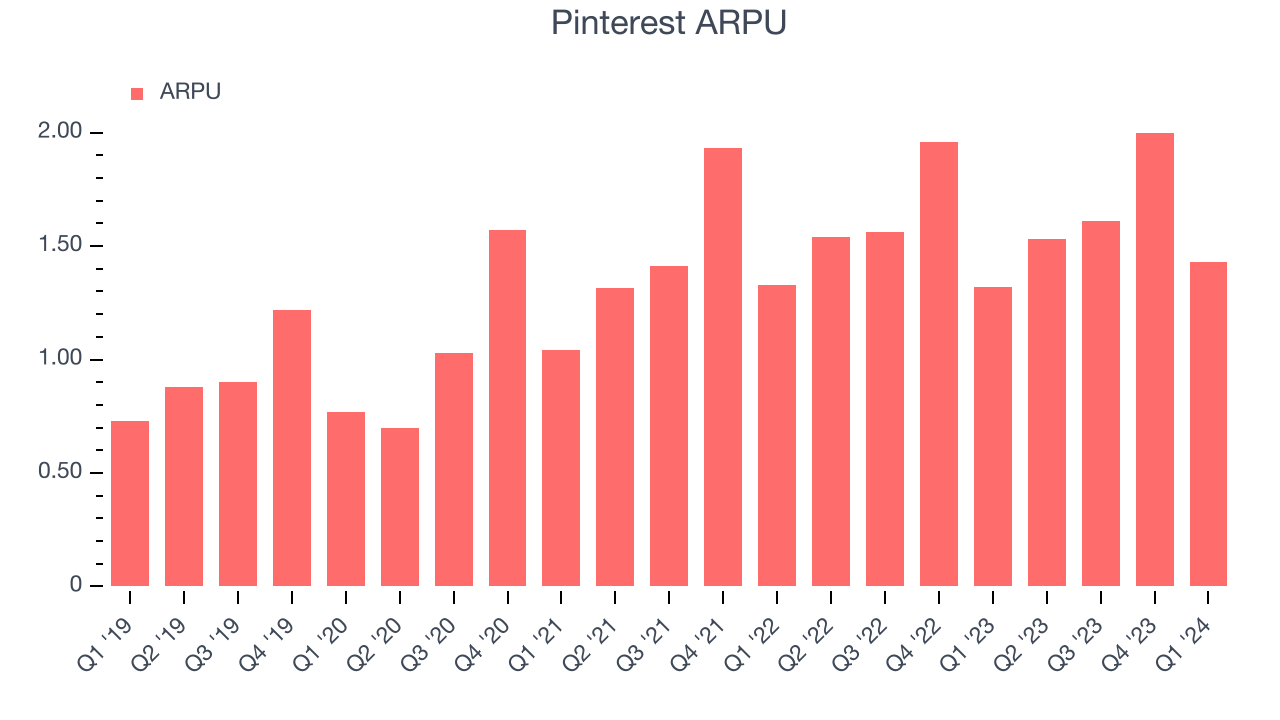

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Pinterest because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Pinterest's audience and its ad-targeting capabilities.

Pinterest's ARPU growth has been decent over the last two years, averaging 5.2%. The company's ability to increase prices while growing its monthly active users demonstrates the value of its platform. This quarter, ARPU grew 8.2% year on year to $1.43 per user.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor.

Pinterest's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 75.5% this quarter, up 3.9 percentage points year on year.

For social network businesses like Pinterest, these aforementioned costs typically include customer service, data center, and other infrastructure expenses. After paying for these expenses, Pinterest had $0.76 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

Pinterest's gross margins have been trending up over the last 12 months, averaging 78.1%. Its margins are some of the highest in the consumer internet sector, enabling it to fund large investments in product and marketing during periods of rapid growth to stay one step ahead of the competition.

User Acquisition Efficiency

Consumer internet businesses like Pinterest grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

Pinterest is efficient at acquiring new users, spending 38.4% of its gross profit on sales and marketing expenses over the last year. This level of efficiency indicates relatively solid competitive positioning, giving Pinterest the freedom to invest its resources into new growth initiatives.

Profitability & Free Cash Flow

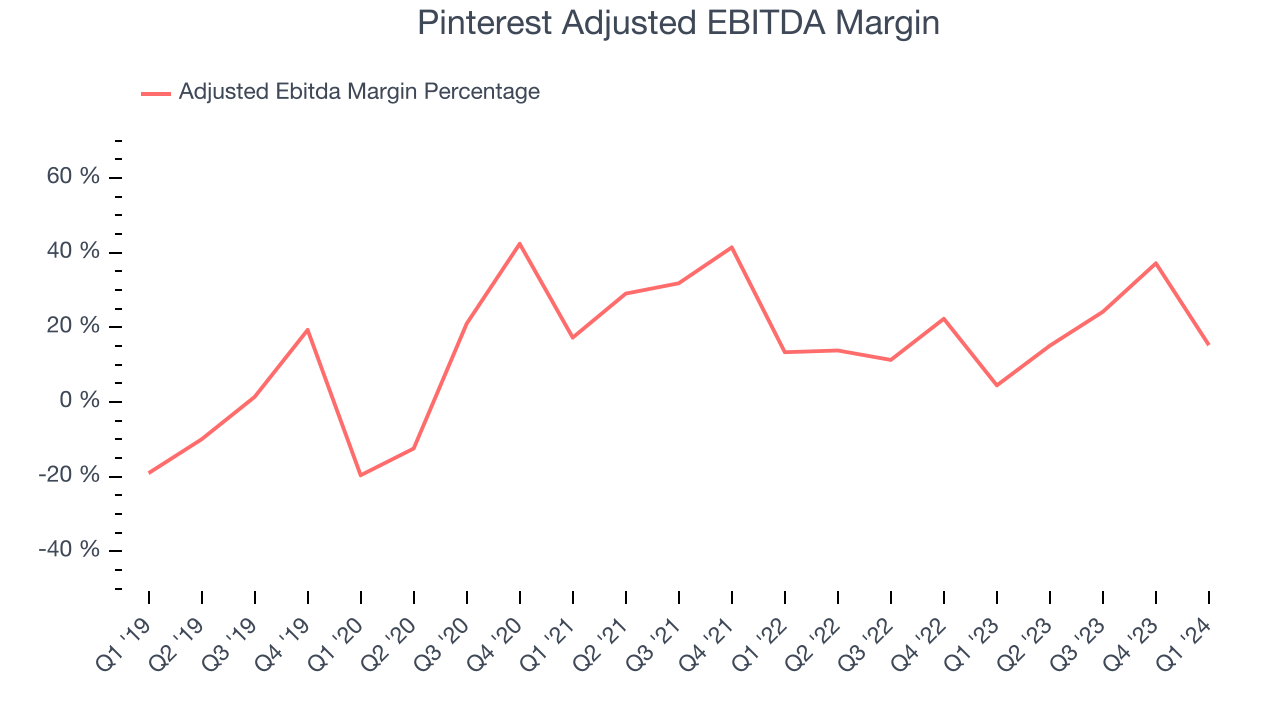

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

Pinterest's EBITDA was $112.9 million this quarter, translating into a 15.3% margin. Furthermore, Pinterest has shown strong profitability over the last four quarters, with average EBITDA margins of 24.1%.

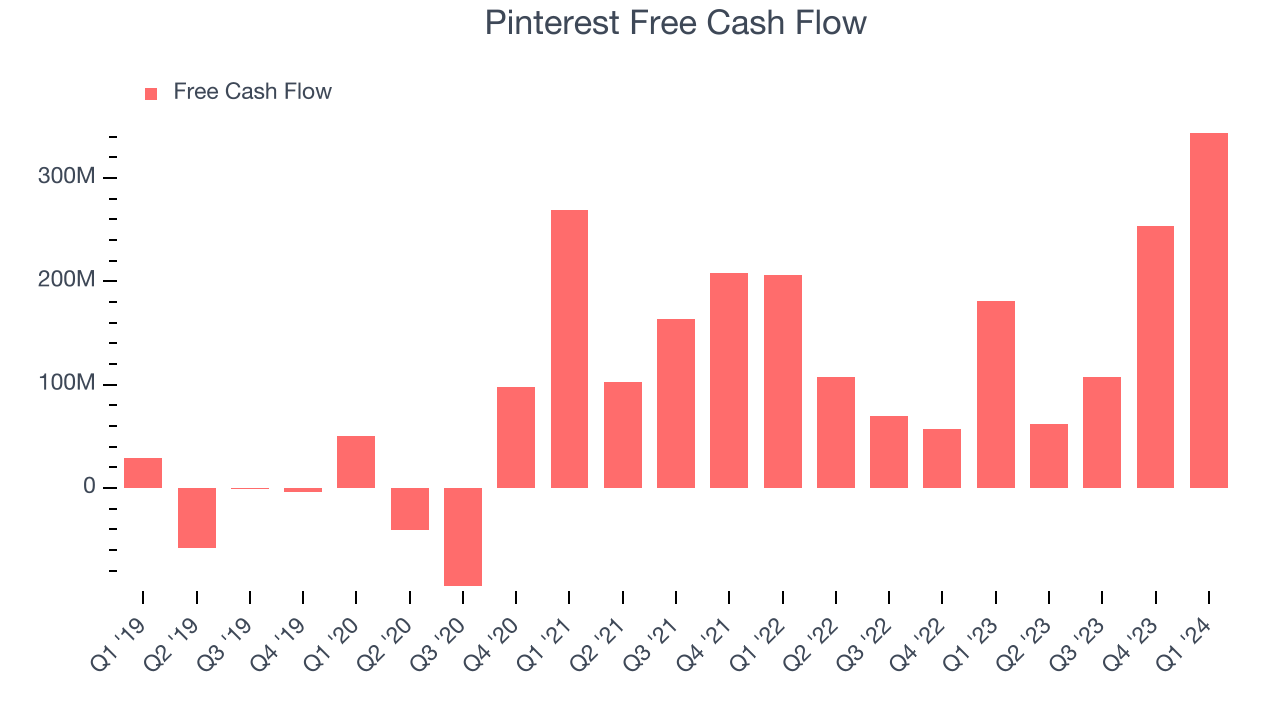

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Pinterest's free cash flow came in at $344 million in Q1, up 89.6% year on year.

Pinterest has generated $767.5 million in free cash flow over the last 12 months, an eye-popping 24% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Pinterest is a well-capitalized company with $2.78 billion of cash and $154.3 million of debt, meaning it could pay back all its debt tomorrow and still have $2.62 billion of cash on its balance sheet. This net cash position gives Pinterest the freedom to raise more debt, return capital to shareholders, or invest in growth initiatives.

Key Takeaways from Pinterest's Q1 Results

We enjoyed seeing Pinterest exceed analysts' revenue expectations this quarter on higher-than-expected MAUs (monthly active users). We were also glad next quarter's revenue guidance came in higher than Wall Street's estimates. The big bright spot was actually next quarter's implied operating profit guidance--while Wall Street was expecting a loss, the company guided to a nice profit instead. Overall, we think this was a really good quarter that should please shareholders. The stock is up 22.5% after reporting and currently trades at $40.99 per share.

Is Now The Time?

When considering an investment in Pinterest, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

There are several reasons why we think Pinterest is a great business. For starters, its revenue growth has been solid over the last three years, and its growth over the next 12 months is expected to exceed that. Additionally, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits and its impressive gross margins are a wonderful starting point for the overall profitability of the business.

At the moment, Pinterest trades at 23.4x next 12 months EV-to-EBITDA. Looking at the consumer internet landscape today, Pinterest's qualities stand out, and we like the stock at this price.

Wall Street analysts covering the company had a one-year price target of $42.94 per share right before these results (compared to the current share price of $40.99), implying they saw upside in buying Pinterest in the short term.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.