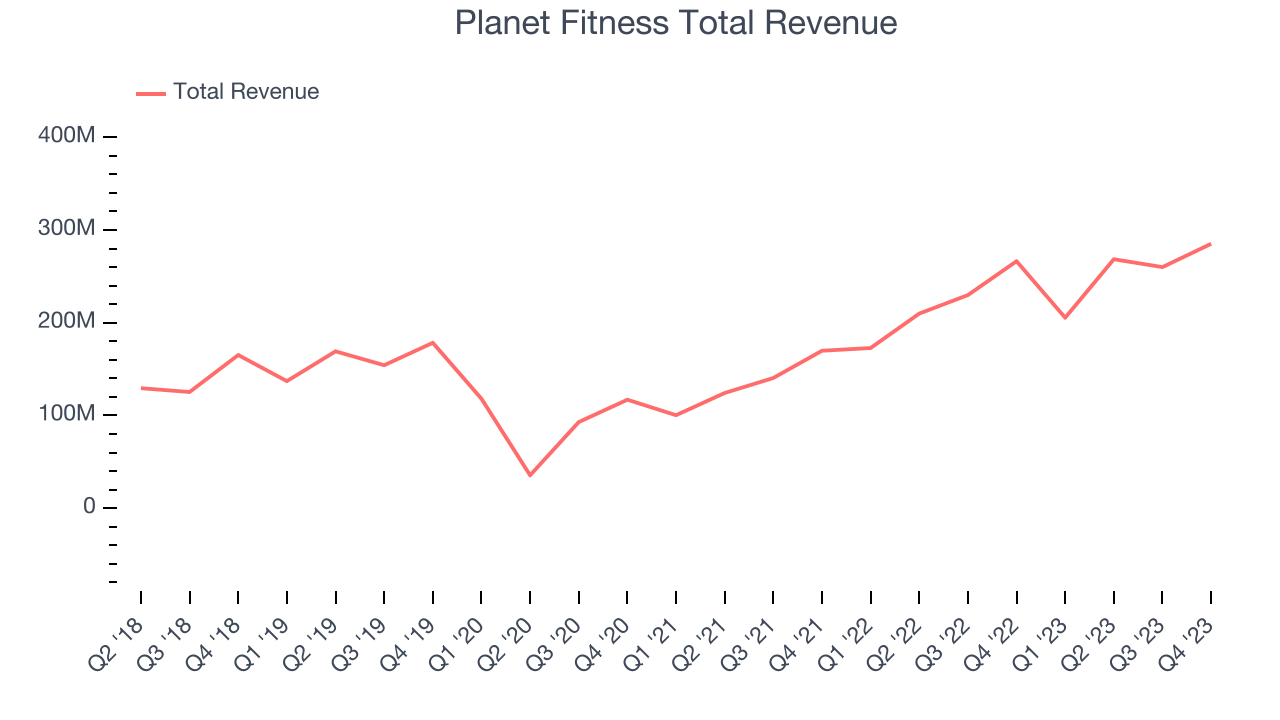

Inclusive gym franchise company (NYSE:PLNT) announced better-than-expected results in Q4 FY2023, with revenue up 1.4% year on year to $285.1 million. It made a non-GAAP profit of $0.60 per share, improving from its profit of $0.53 per share in the same quarter last year.

Is now the time to buy Planet Fitness? Find out by accessing our full research report, it's free.

Planet Fitness (PLNT) Q4 FY2023 Highlights:

- Revenue: $285.1 million vs analyst estimates of $282.2 million (1% beat)

- EPS (non-GAAP): $0.60 vs analyst estimates of $0.58 (3.5% beat)

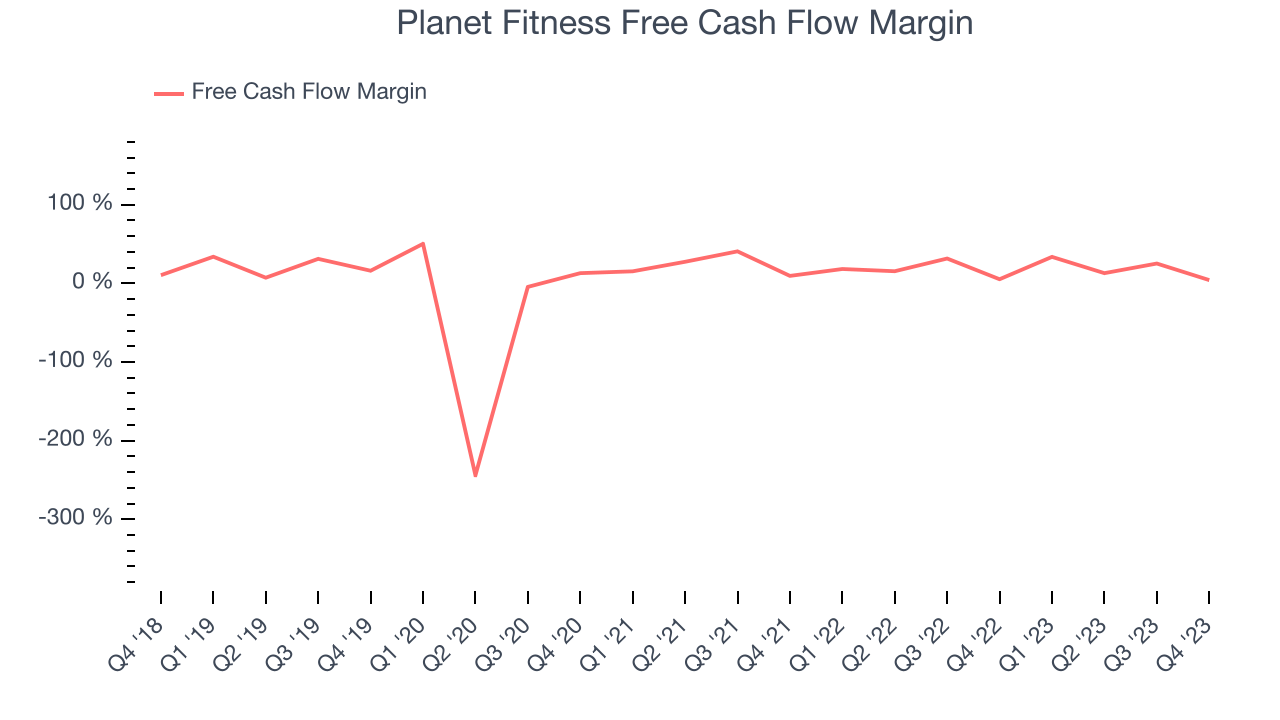

- Free Cash Flow of $11.98 million, down 82.9% from the previous quarter

- Gross Margin (GAAP): 56.8%, up from 53.3% in the same quarter last year

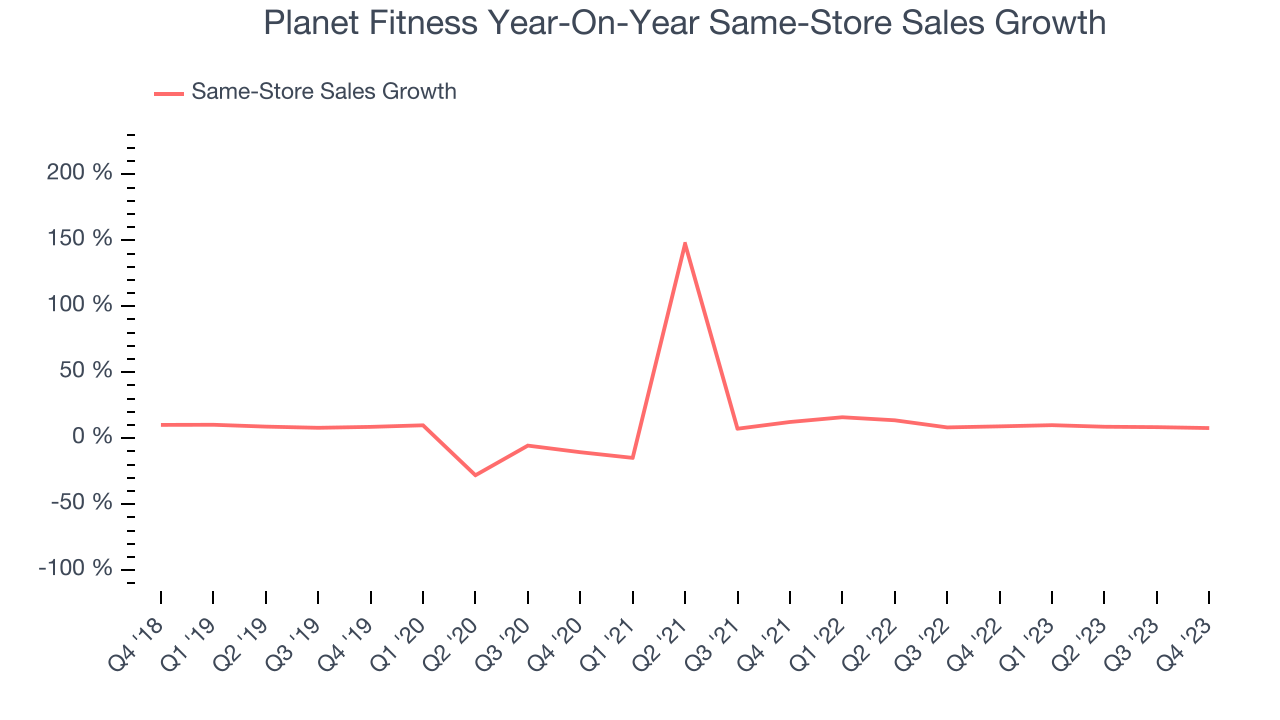

- Same-Store Sales were up 7.7% year on year

- Market Capitalization: $5.63 billion

"In 2023, we proactively developed the New Growth Model to fuel long-term sustainable store growth and in recognition of the macro-economic environmental changes that have taken place since the pandemic. Focused on enhancing returns and reducing the capital requirements for opening and maintaining a Planet Fitness franchise location, the New Growth Model will provide our franchisees with additional flexibility to build their store portfolios for years to come," said Craig Benson, Interim Chief Executive Officer.

Founded by two brothers who purchased a struggling gym, Planet Fitness (NYSE:PLNT) is a gym franchise which caters to casual fitness users by providing a friendly and inclusive atmosphere.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. Planet Fitness's annualized revenue growth rate of 13.3% over the last five years was decent for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Planet Fitness's annualized revenue growth of 35.1% over the last two years is above its five-year trend, suggesting some bright spots.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Planet Fitness's annualized revenue growth of 35.1% over the last two years is above its five-year trend, suggesting some bright spots.

We can dig even further into the company's revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Planet Fitness's same-store sales averaged 10.2% year-on-year growth. Because this number is lower than its revenue growth, we can see the company's sales are benefitting from the opening of new locations.

This quarter, Planet Fitness reported reasonable year-on-year revenue growth of 1.4%, and its $285.1 million of revenue topped Wall Street's estimates by 1%. Looking ahead, Wall Street expects sales to grow 7.4% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Planet Fitness has shown strong cash profitability, giving it an edge over its competitors and the option to reinvest or return capital to investors while keeping cash on hand for emergencies. The company's free cash flow margin has averaged 17.7%, quite impressive for a consumer discretionary business.

Planet Fitness's free cash flow came in at $11.98 million in Q4, equivalent to a 4.2% margin and down 19.4% year on year. Over the next year, analysts predict Planet Fitness's cash profitability will fall. Their consensus estimates imply its LTM free cash flow margin of 18.1% will decrease to 16.9%.

Key Takeaways from Planet Fitness's Q4 Results

It was encouraging to see Planet Fitness narrowly top analysts' revenue expectations this quarter, driven by more new gym openings than expected (77 vs estimates of 69). That boost, however, was offset by underperformance in its same-store sales (7.7% growth vs estimates of 8.3% growth). In terms of profitability, we were glad its adjusted EBITDA and EPS beat Wall Street's forecasts.

Looking ahead, the company's full-year 2024 revenue and EPS guidance fell short as Planet Fitness focuses on rolling out its New Growth Model to franchisees. The company also increased its total store opportunity to 5,000 gyms in the U.S., up from the 4,000 it stated in its 2015 IPO.

Overall, this was a mixed quarter for Planet Fitness. The company is down 2.1% on the results and currently trades at $64.5 per share.

So should you invest in Planet Fitness right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.