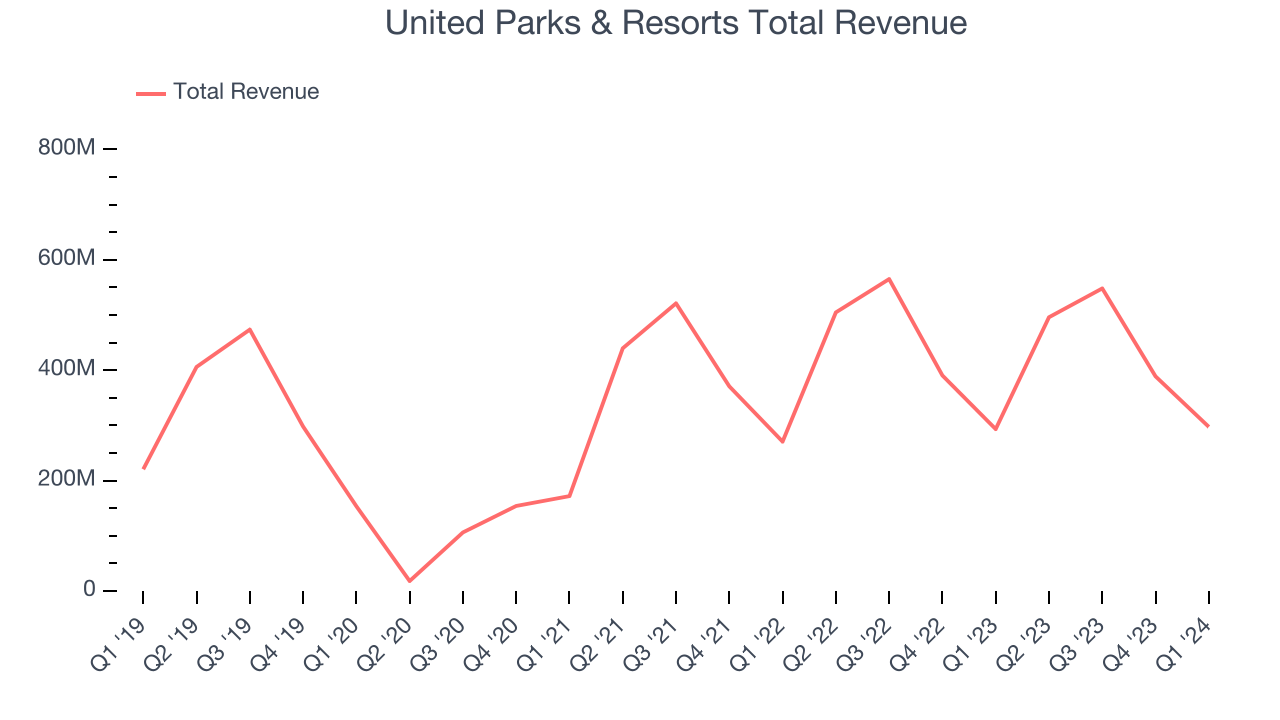

Theme park operator United Parks & Resorts (NYSE:SEAS) beat analysts' expectations in Q1 CY2024, with revenue up 1.4% year on year to $297.4 million. It made a GAAP loss of $0.17 per share, improving from its loss of $0.26 per share in the same quarter last year.

United Parks & Resorts (PRKS) Q1 CY2024 Highlights:

- Revenue: $297.4 million vs analyst estimates of $284.7 million (4.5% beat)

- EPS: -$0.17 vs analyst estimates of -$0.28 (40.1% beat)

- Gross Margin (GAAP): 36.8%, up from 33.2% in the same quarter last year

- Free Cash Flow was -$15.84 million, down from $35.84 million in the previous quarter

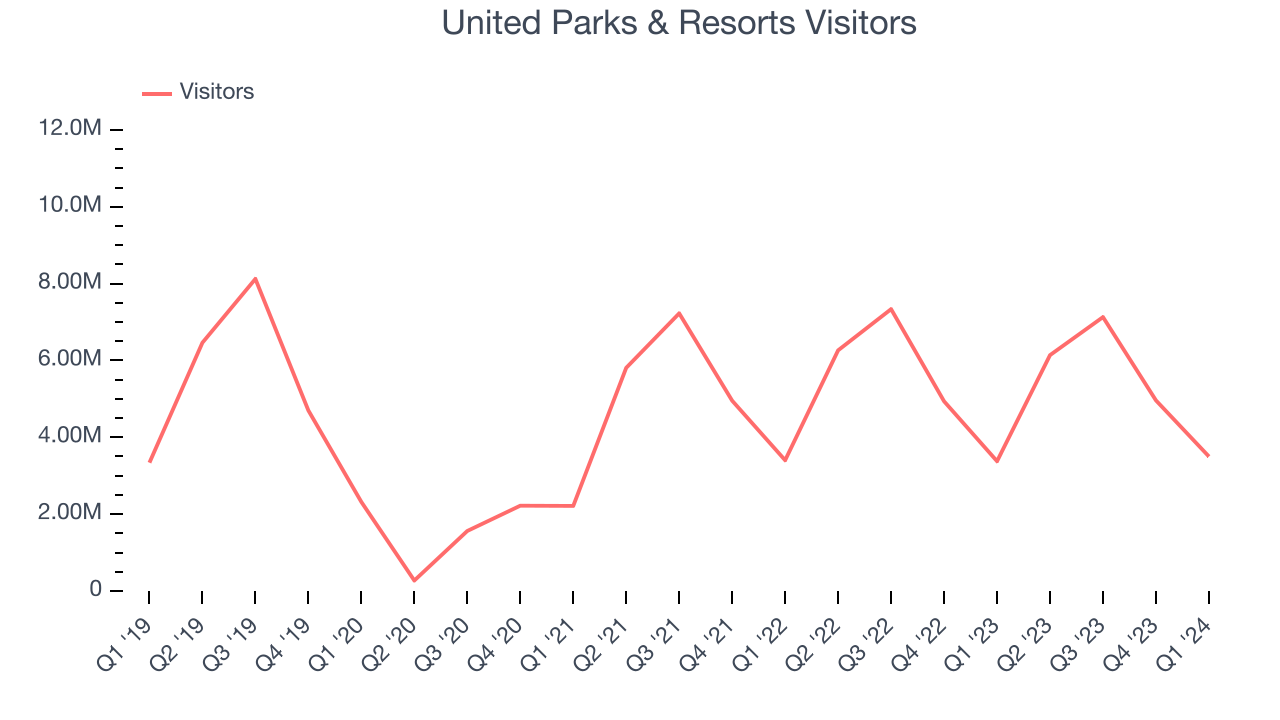

- Visitors: 3.5 million

- Market Capitalization: $3.11 billion

Parent company of SeaWorld and home of the world-famous Shamu, United Parks & Resorts (NYSE:PRKS) is a theme park chain featuring marine life, live entertainment, roller coasters, and waterparks.

The company, originally named SeaWorld, was founded in 1964 by four UCLA graduates whose original idea was to develop an underwater restaurant. It has since rebranded into United Parks & Resorts, evolving into much more, and is known today for its aquatic shows and thrilling rides.

United Parks & Resorts's primary revenue streams are ticket sales, in-park dining, merchandise, and special events. Its parks seek to blend entertainment with marine education, enabling visitors to enjoy performances from marine animals while gaining insights into oceanic conservation.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

Competitors offering amusement park experiences nationally include Six Flags (NYSE:SIX), Cedar Fair (NYSE:FUN), and Walt Disney (NYSE:DIS).Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. United Parks & Resorts's annualized revenue growth rate of 4.7% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. United Parks & Resorts's annualized revenue growth of 3.9% over the last two years aligns with its five-year revenue growth, suggesting the company's demand has been stable.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. United Parks & Resorts's annualized revenue growth of 3.9% over the last two years aligns with its five-year revenue growth, suggesting the company's demand has been stable.

We can better understand the company's revenue dynamics by analyzing its number of visitors, which reached 3.5 million in the latest quarter. Over the last two years, United Parks & Resorts's visitors were flat. Because this number is lower than its revenue growth during the same period, we can see the company's monetization of its consumers has risen.

This quarter, United Parks & Resorts reported reasonable year-on-year revenue growth of 1.4%, and its $297.4 million of revenue topped Wall Street's estimates by 4.5%. Looking ahead, Wall Street expects sales to grow 2.8% over the next 12 months, an acceleration from this quarter.

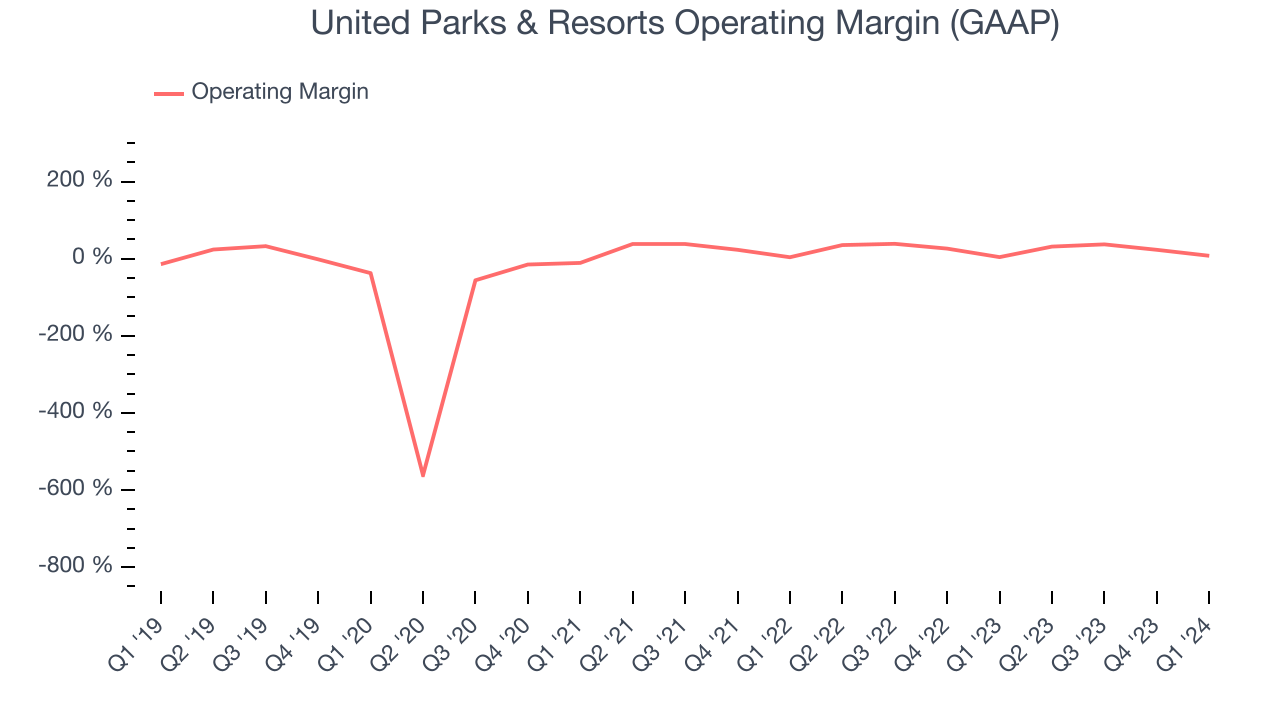

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

United Parks & Resorts has been a well-oiled machine over the last two years. It's demonstrated elite profitability for a consumer discretionary business, boasting an average operating margin of 28.1%.

In Q1, United Parks & Resorts generated an operating profit margin of 7.4%, up 3.4 percentage points year on year.

Over the next 12 months, Wall Street expects United Parks & Resorts to become more profitable. Analysts are expecting the company’s LTM operating margin of 27.2% to rise to 30.2%.EPS

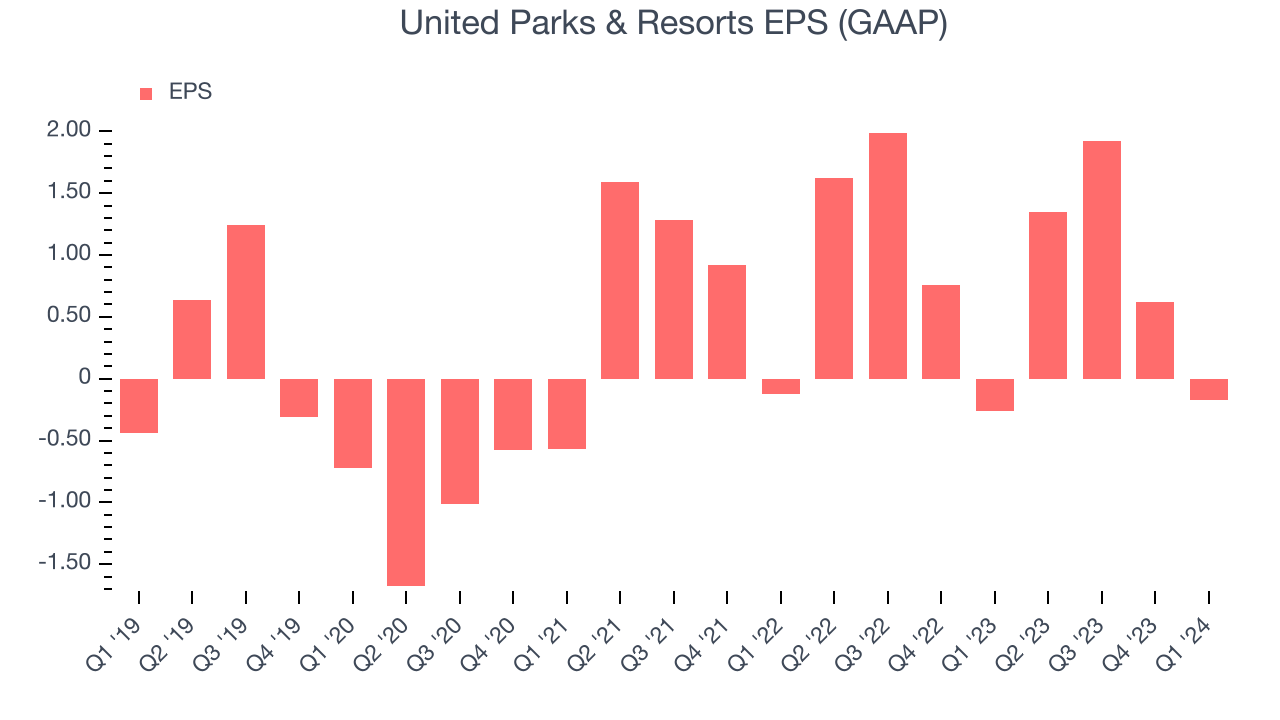

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, United Parks & Resorts's EPS grew 371%, translating into an astounding 36.3% compounded annual growth rate. This performance is materially higher than its 4.7% annualized revenue growth over the same period. Let's dig into why.

United Parks & Resorts's operating margin has expanded 21.6 percentage points over the last five years while its share count has shrunk 23.2%. Improving profitability and share buybacks are positive signs as they juice EPS growth relative to revenue growth.In Q1, United Parks & Resorts reported EPS at negative $0.17, up from negative $0.26 in the same quarter last year. This print beat analysts' estimates by 40.1%. Over the next 12 months, Wall Street expects United Parks & Resorts to grow its earnings. Analysts are projecting its LTM EPS of $3.72 to climb by 19.4% to $4.44.

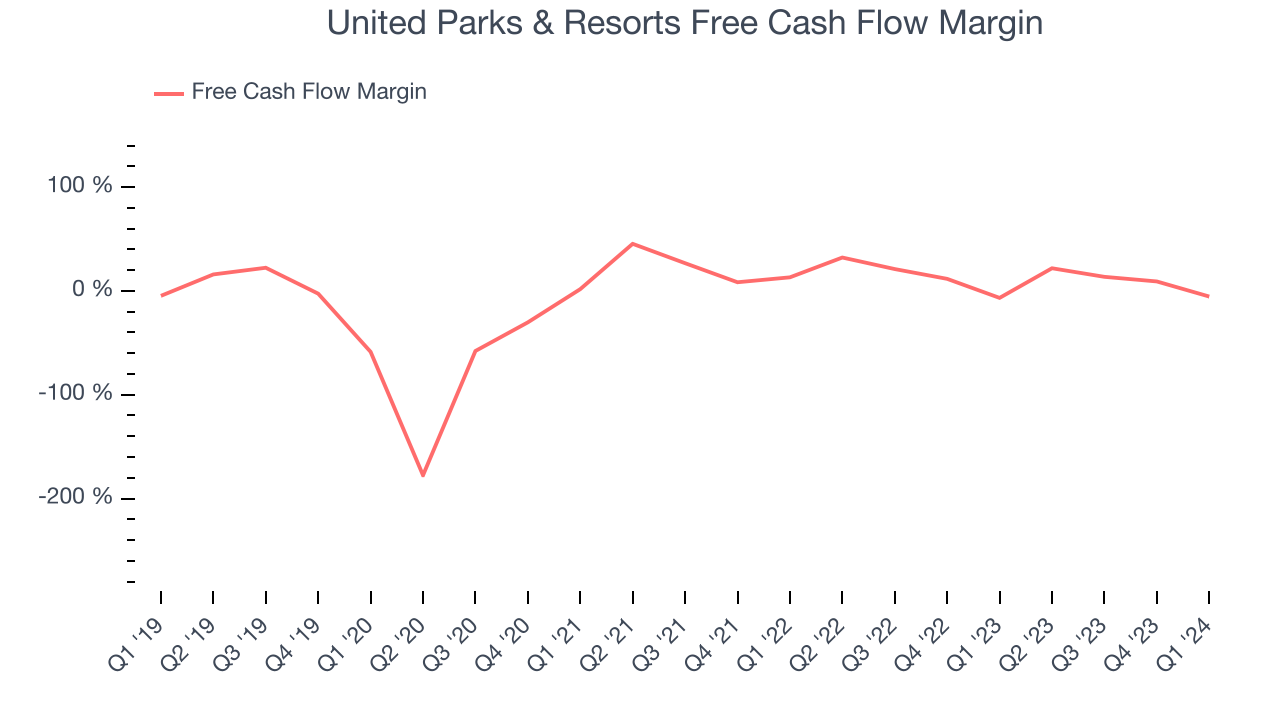

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, United Parks & Resorts has shown solid cash profitability, giving it the flexibility to reinvest or return capital to investors. The company's free cash flow margin has averaged 14.7%, above the broader consumer discretionary sector.

United Parks & Resorts burned through $15.84 million of cash in Q1, equivalent to a negative 5.3% margin, increasing its cash burn by 18.6% year on year.

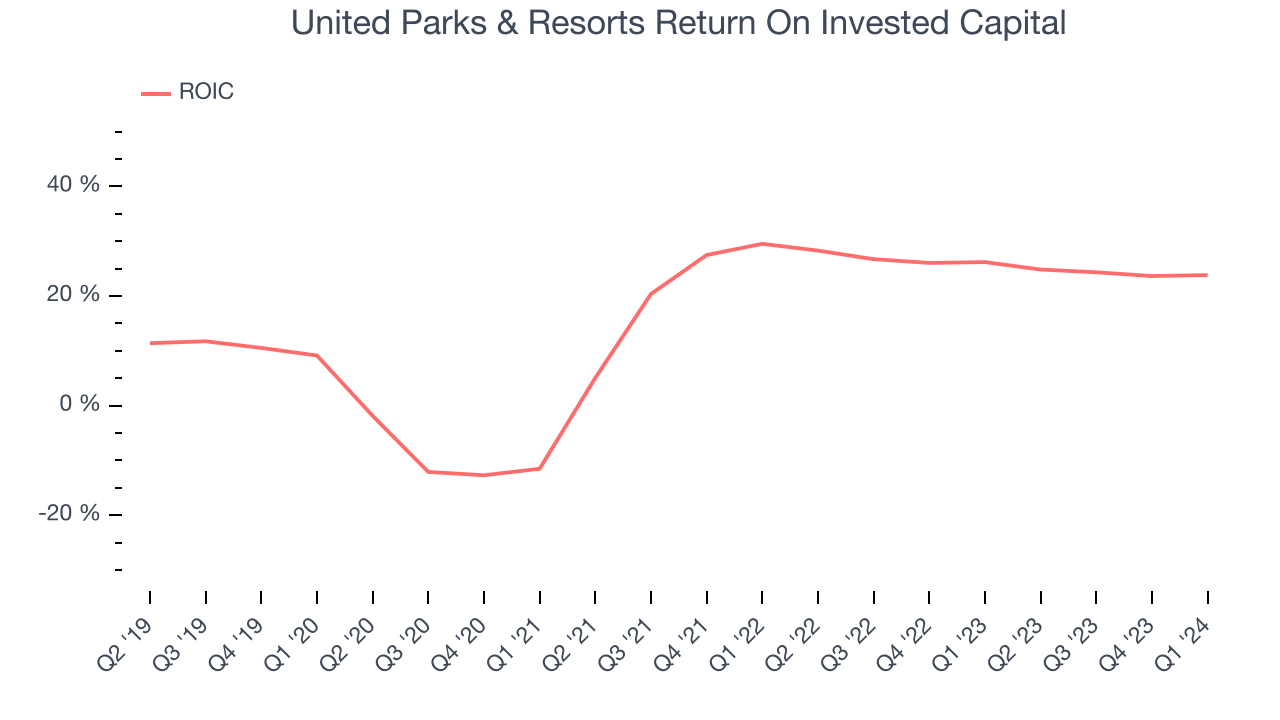

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

United Parks & Resorts's five-year average return on invested capital was 15.4%, slightly better than the broader sector. Just as you’d like your investment dollars to generate returns, United Parks & Resorts's invested capital has produced decent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, United Parks & Resorts's ROIC has significantly increased. This is a good sign, and if the company's returns keep rising, there's a chance it could evolve into an investable business.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

United Parks & Resorts reported $203.7 million of cash and $2.12 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $720.3 million of EBITDA over the last 12 months, we view United Parks & Resorts's 2.7x net-debt-to-EBITDA ratio as safe. We also see its $71.49 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from United Parks & Resorts's Q1 Results

We were impressed by how significantly United Parks & Resorts blew past analysts' EPS estimates this quarter, driven by outperformance in its operating margin. We were also glad its revenue beat as it attracted more visitors than expected. Zooming out, we think this was a great quarter that shareholders will appreciate. The stock is up 3% after reporting and currently trades at $50.6 per share.

Is Now The Time?

United Parks & Resorts may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We have other favorites, but we understand the arguments that United Parks & Resorts isn't a bad business. Although its revenue growth has been uninspiring over the last five years with analysts expecting growth to slow from here, its impressive operating margins show it has a highly efficient business model. Investors should still be cautious, however, as its number of visitors has been disappointing.

United Parks & Resorts's price-to-earnings ratio based on the next 12 months is 10.5x. In the end, beauty is in the eye of the beholder. While United Parks & Resorts wouldn't be our first pick, if you like the business, the shares are trading at a pretty interesting price right now.

Wall Street analysts covering the company had a one-year price target of $64.91 per share right before these results (compared to the current share price of $50.60).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.