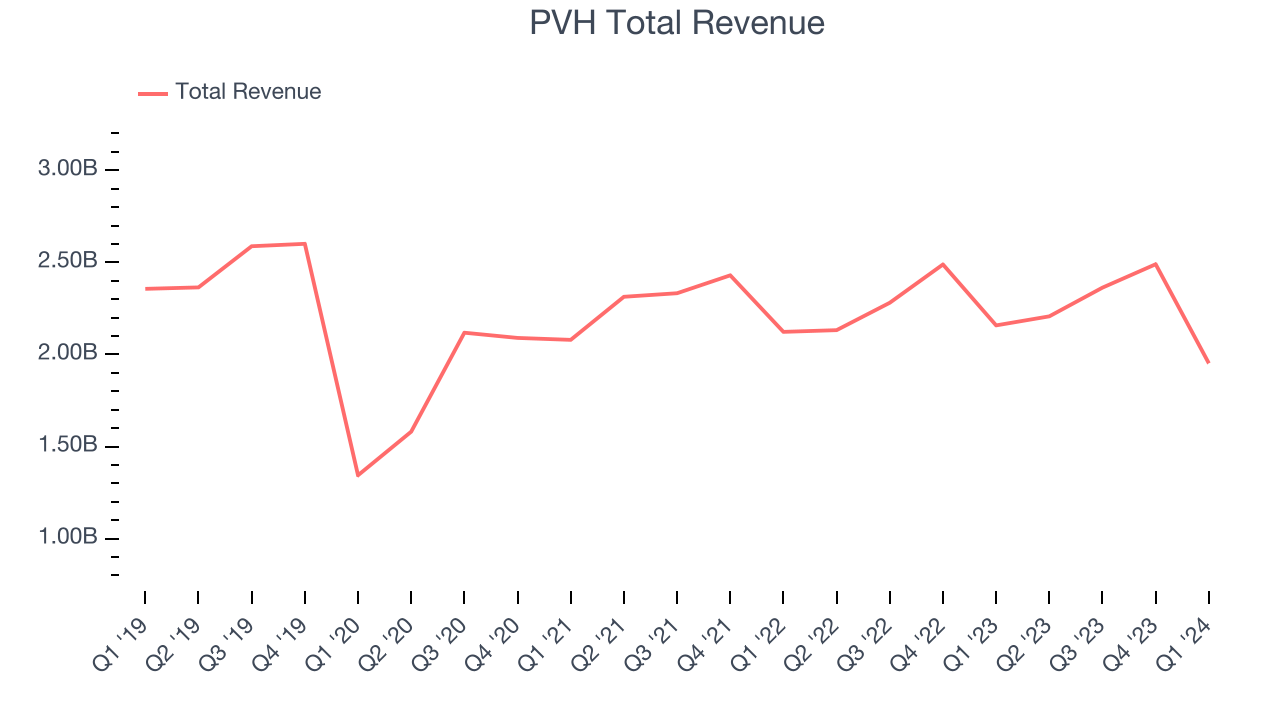

Fashion conglomerate PVH (NYSE:PVH) announced better-than-expected results in Q1 CY2024, with revenue down 9.5% year on year to $1.95 billion. It made a GAAP profit of $2.59 per share, improving from its profit of $2.14 per share in the same quarter last year.

Is now the time to buy PVH? Find out by accessing our full research report, it's free.

PVH (PVH) Q1 CY2024 Highlights:

- Revenue: $1.95 billion vs analyst estimates of $1.94 billion (small beat)

- EPS (non-GAAP): $2.45 vs analyst estimates of $2.19 (12.1% beat)

- Full year EPS (non-GAAP) guidance raised: $11.13 at the midpoint vs. analyst estimates of $11.09 (slight beat)

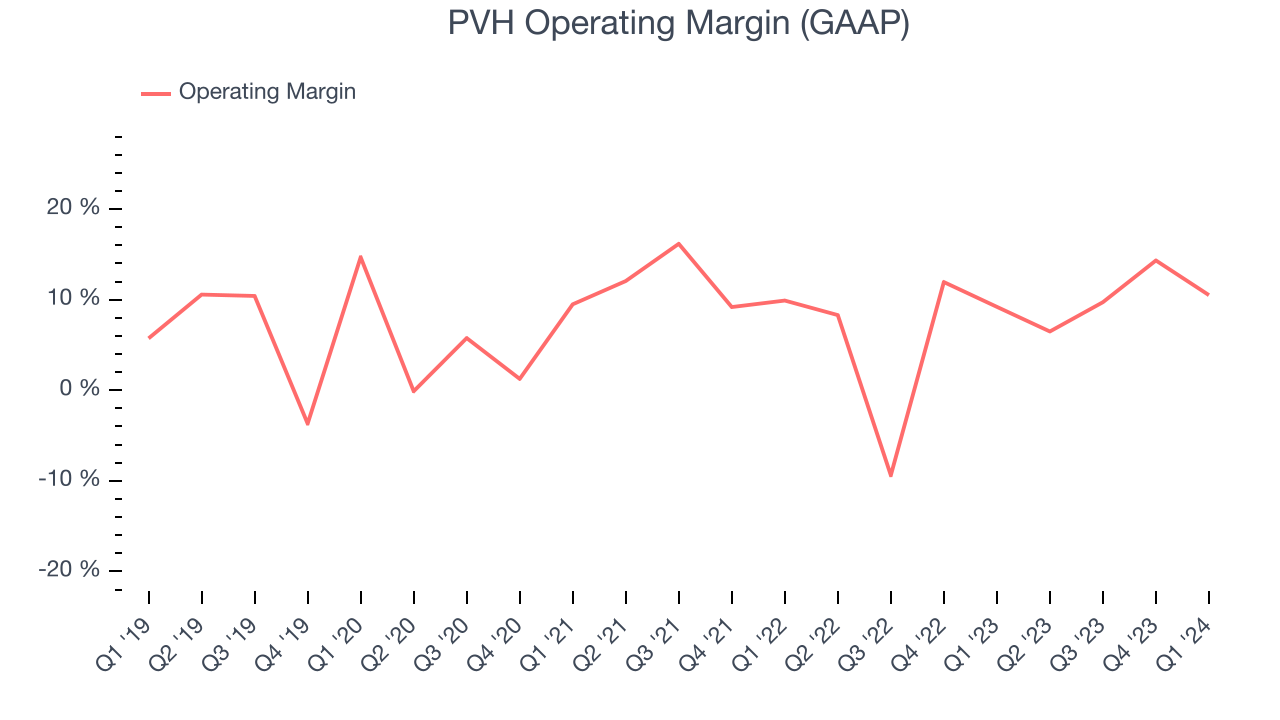

- Gross Margin (GAAP): 61.4%, up from 57.9% in the same quarter last year

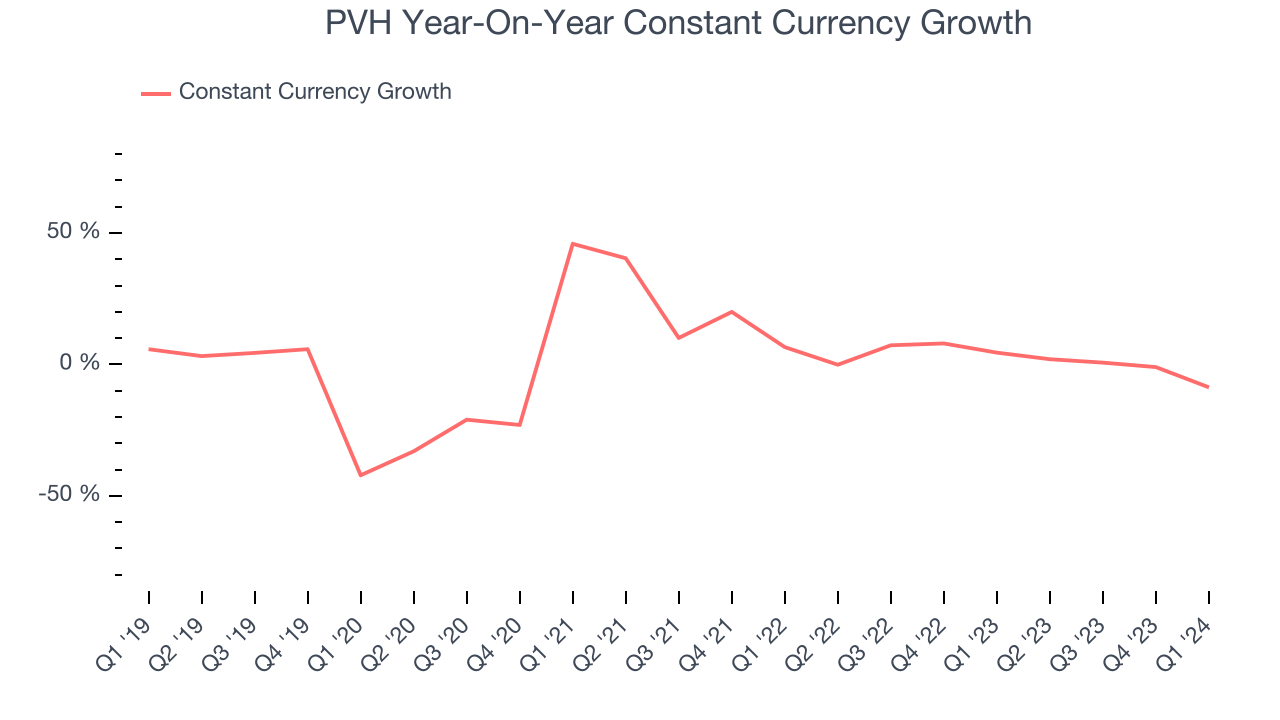

- Constant Currency Revenue fell 8.7% year on year ( compared to 4.5% in the same quarter last year)

- Market Capitalization: $6.93 billion

Stefan Larsson, Chief Executive Officer, commented, “We delivered on our revenue expectations, led by growth in our direct-to-consumer business, and beat our earnings guidance for the first quarter. We further strengthened our brand positioning and pricing power in the marketplace, and as planned we generated growth for Calvin Klein and Tommy Hilfiger combined in both North America and Asia Pacific in constant currency, while successfully driving strategic quality of sales initiatives in Europe.”

Founded in 1881 by a husband and wife duo, PVH (NYSE:PVH) is a global fashion conglomerate with iconic brands like Calvin Klein and Tommy Hilfiger.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. PVH struggled to generate demand over the last five years as its sales dropped by 1.5% annually, setting a rough starting point for our quality assessment.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. PVH's annualized revenue declines of 1% over the last two years align with its five-year trend, suggesting its demand consistently shrunk.

PVH also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 1.6% year-on-year growth. Because this number is better than its revenue growth, we can see that foreign exchange rates have been a headwind for PVH.

This quarter, PVH's revenue fell 9.5% year on year to $1.95 billion but beat Wall Street's estimates by 0.8%. Looking ahead, Wall Street expects revenue to decline 2.7% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

PVH was profitable over the last two years but held back by its large expense base. It demonstrated paltry profitability for a consumer discretionary business, producing an average operating margin of 7.7%.

This quarter, PVH generated an operating profit margin of 10.5%, up 1.3 percentage points year on year. Looking ahead, Wall Street expects PVH to maintain its trailing 12 month operating margin of 10.4% in the coming year.

Key Takeaways from PVH's Q1 Results

It was good to see PVH beat analysts' operating margin expectations this quarter. We were also glad its EPS outperformed Wall Street's estimates. On the other hand, its Calvin Klein revenue unfortunately missed and its earnings guidance for next quarter fell short of Wall Street's estimates. Zooming out, we think this was still a decent, albeit mixed, quarter. The stock is flat after reporting and currently trades at $118.51 per share.

So should you invest in PVH right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.