Banking software provider Q2 (NYSE:QTWO) beat analysts' expectations in Q1 CY2024, with revenue up 8.2% year on year to $165.5 million. Guidance for next quarter's revenue was also better than expected at $170.5 million at the midpoint, 1.7% above analysts' estimates. It made a GAAP loss of $0.23 per share, down from its loss of $0.01 per share in the same quarter last year.

Q2 Holdings (QTWO) Q1 CY2024 Highlights:

- Revenue: $165.5 million vs analyst estimates of $163.2 million (1.4% beat)

- EPS: -$0.23 vs analyst estimates of -$0.33 (30.3% beat)

- Revenue Guidance for Q2 CY2024 is $170.5 million at the midpoint, above analyst estimates of $167.6 million

- The company slightly raised its revenue and adjusted EBITDA guidance for the full year, both of which are above expectations

- Gross Margin (GAAP): 49.7%, up from 47.9% in the same quarter last year

- Free Cash Flow of $6.02 million, down 79.8% from the previous quarter

- Market Capitalization: $3.09 billion

Founded in 2004 by Hank Seale, Q2 (NYSE:QTWO) offers software-as-a-service that enables small banks to provide online banking and consumer lending services to their clients.

Small, regional and community banks often lack the resources required to manage their own tech infrastructure, making it difficult for them to compete with polished offerings of large national banks. Q2’s cloud-based platform provides them with mobile apps and websites that have the same functionalities big banks offer and allows them to put their own branding on it.

Q2 then handles all the regulatory compliance and security and provides banks with data-based insights on their customers, allowing them to offer more personalized products and better customer service.

Banking Software

Consumers these days are accustomed to frictionless digital experiences from online shopping to ordering food or hailing a cab. Financial services firms are notoriously risk averse in adopting modern software, often lacking the resources or competency to develop the digital solutions in-house. That drives demand for software as a service platforms that allows banks and other finance institutions to offer the digital services without having to run or maintain them.

Q2 and companies like nCino (NASDAQ:NCNO) or Alkami (NASDAQ:ALKT) are offering them a chance to keep up with the bigger players in the market.

Sales Growth

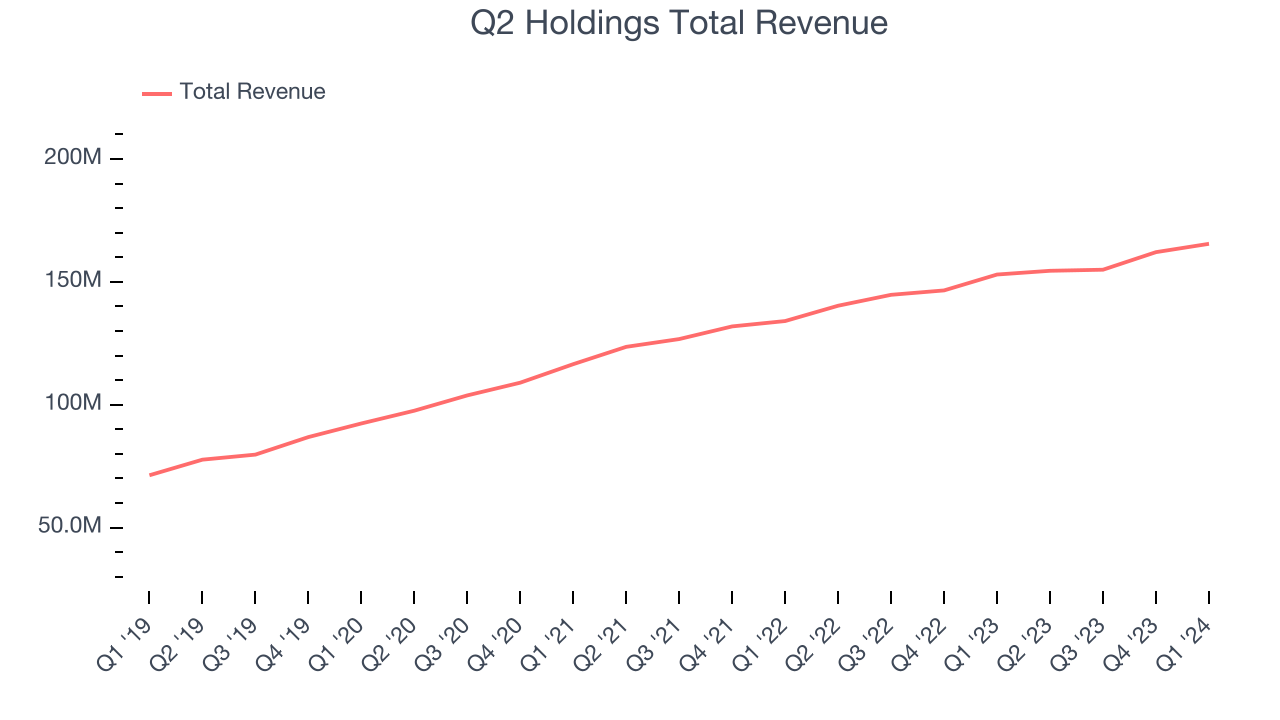

As you can see below, Q2 Holdings's revenue growth has been mediocre over the last three years, growing from $116.5 million in Q1 2021 to $165.5 million this quarter.

Q2 Holdings's quarterly revenue was only up 8.2% year on year, which might disappoint some shareholders. Additionally, its growth did slow down compared to last quarter as the company's revenue increased by just $3.39 million in Q1 compared to $7.15 million in Q4 CY2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Q2 Holdings is expecting revenue to grow 10.3% year on year to $170.5 million, in line with the 10.1% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.9% over the next 12 months before the earnings results announcement.

Profitability

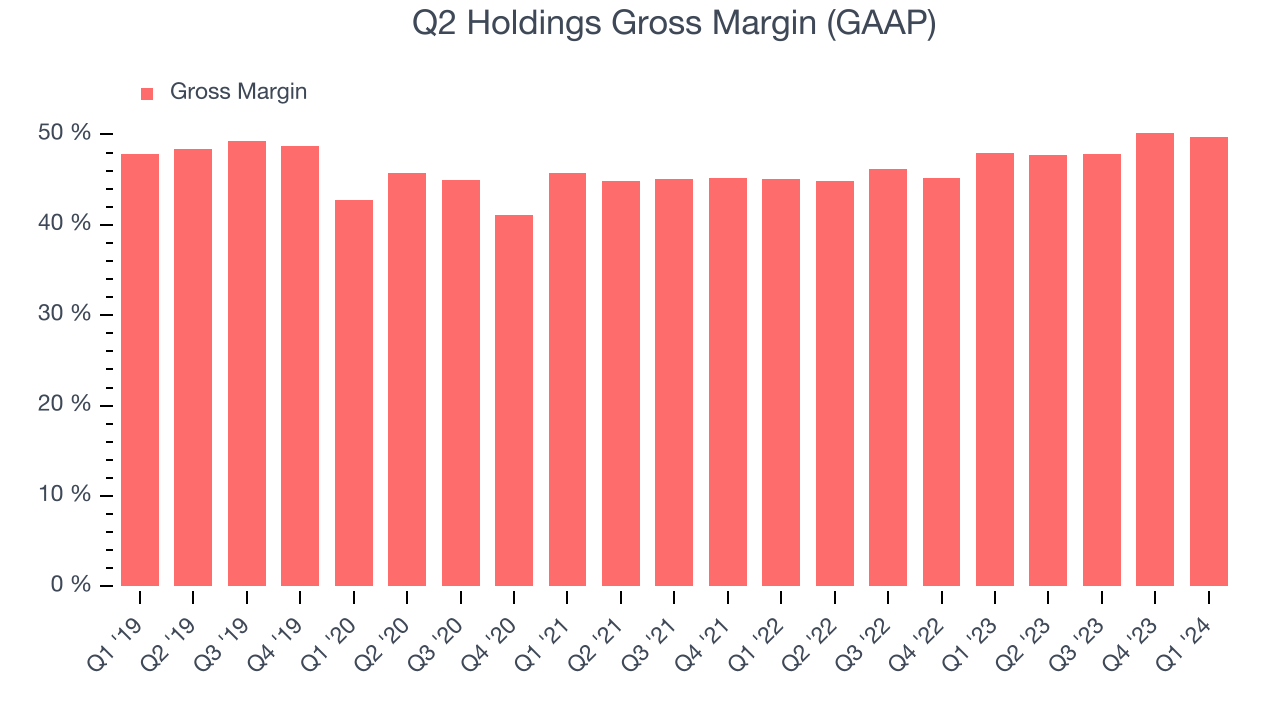

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Q2 Holdings's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 49.7% in Q1.

That means that for every $1 in revenue the company had $0.50 left to spend on developing new products, sales and marketing, and general administrative overhead. Q2 Holdings's gross margin is poor for a SaaS business and it's dropped significantly since the previous quarter. This is probably the exact opposite of what shareholders would like to see.

Cash Is King

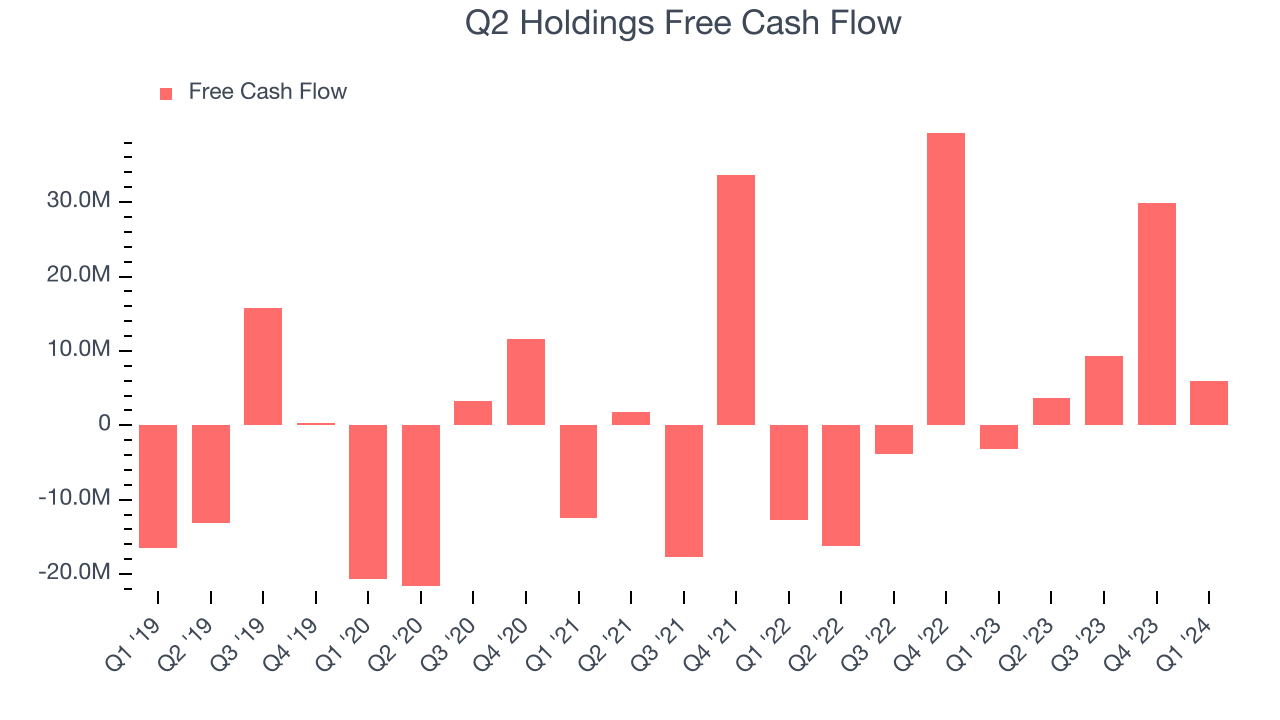

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Q2 Holdings's free cash flow came in at $6.02 million in Q1, turning positive over the last year.

Q2 Holdings has generated $48.86 million in free cash flow over the last 12 months, or 7.7% of revenue. This FCF margin enables it to reinvest in its business without depending on the capital markets.

Key Takeaways from Q2 Holdings's Q1 Results

It was good to see Q2 Holdings's strong revenue guidance for next quarter, which topped analysts' expectations. We were also happy its revenue narrowly outperformed Wall Street's estimates. Lastly, the company raised its full year guidance for revenue and adjusted EBITDA. Zooming out, we think this was a really solid quarter, showing that the company is staying on track. The stock is up 2.4% after reporting and currently trades at $52.99 per share.

Is Now The Time?

When considering an investment in Q2 Holdings, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in case of Q2 Holdings, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last three years, and analysts expect growth to deteriorate from here. And while its customers are increasing their spending quite quickly, suggesting they love the product, unfortunately, its gross margins show its business model is much less lucrative than the best software businesses.

Q2 Holdings's price-to-sales ratio based on the next 12 months is 4.4x, suggesting the market has lower expectations for the business relative to the hottest tech stocks. While there are some things to like about Q2 Holdings and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $54.01 right before these results (compared to the current share price of $52.99).

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.