Advertising data platform LiveRamp (NYSE:RAMP) reported Q3 FY2022 results beating Wall St's expectations, with revenue up 17.4% year on year to $140.6 million. However the guidance for the next quarter slightly missed expectations, coming in at $139 million, 0.2% below analyst estimates. LiveRamp made a GAAP loss of $15.3 million, down on its loss of $11.7 million, in the same quarter last year.

Is now the time to buy LiveRamp? Access our full analysis of the earnings results here, it's free.

LiveRamp (RAMP) Q3 FY2022 Highlights:

- Revenue: $140.6 million vs analyst estimates of $139 million (1.08% beat)

- EPS (non-GAAP): $0.14 vs analyst estimates of $0.13 (3.78% beat)

- Revenue guidance for Q4 2022 is $139 million at the midpoint, roughly in line with what analysts were expecting (0.2%)

- Free cash flow of $24.1 million, up 140% from previous quarter

- Net Revenue Retention Rate: 109%, in line with previous quarter

- Customers: 890, up from 870 in previous quarter

- Gross Margin (GAAP): 72.5%, up from 69% same quarter last year

“LiveRamp is fast becoming critical data infrastructure for global brands,” said LiveRamp CEO Scott Howe.

Started in 2011 as a spin-out of RapLeaf, LiveRamp (NYSE:RAMP) provides software as a service that helps companies better target their marketing by merging offline and online data about their customers.

The digital advertising market is large, growing and becoming more diverse, both in terms of audiences and media. This as a result drives a growing need for a software that enables advertisers to use data to automate and optimize ad placements.

Sales Growth

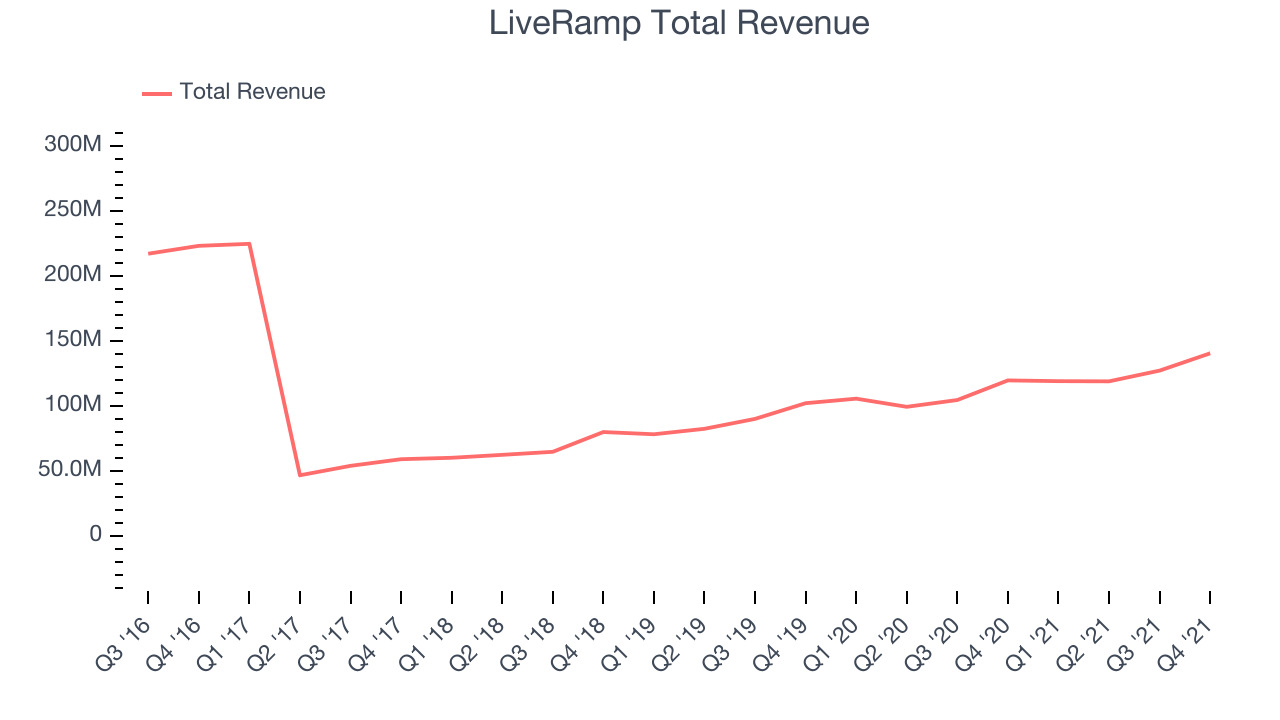

As you can see below, LiveRamp's revenue growth has been moderate over the last year, growing from quarterly revenue of $119.7 million, to $140.6 million.

This quarter, LiveRamp's quarterly revenue was once again up 17.4% year on year. We can see that the company increased revenue by $13.3 million quarter on quarter. That's a solid improvement on the $8.25 million increase in Q2 2022, so shareholders should appreciate the re-acceleration of growth.

Guidance for the next quarter indicates LiveRamp is expecting revenue to grow 16.6% year on year to $139 million, improving on the 12.7% year-over-year increase in revenue the company had recorded in the same quarter last year. Ahead of the earnings results the analysts covering the company were estimating sales to grow 20.1% over the next twelve months.

There are others doing even better than LiveRamp. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 150% since the IPO last December. You can find it on our platform for free.

Product Success

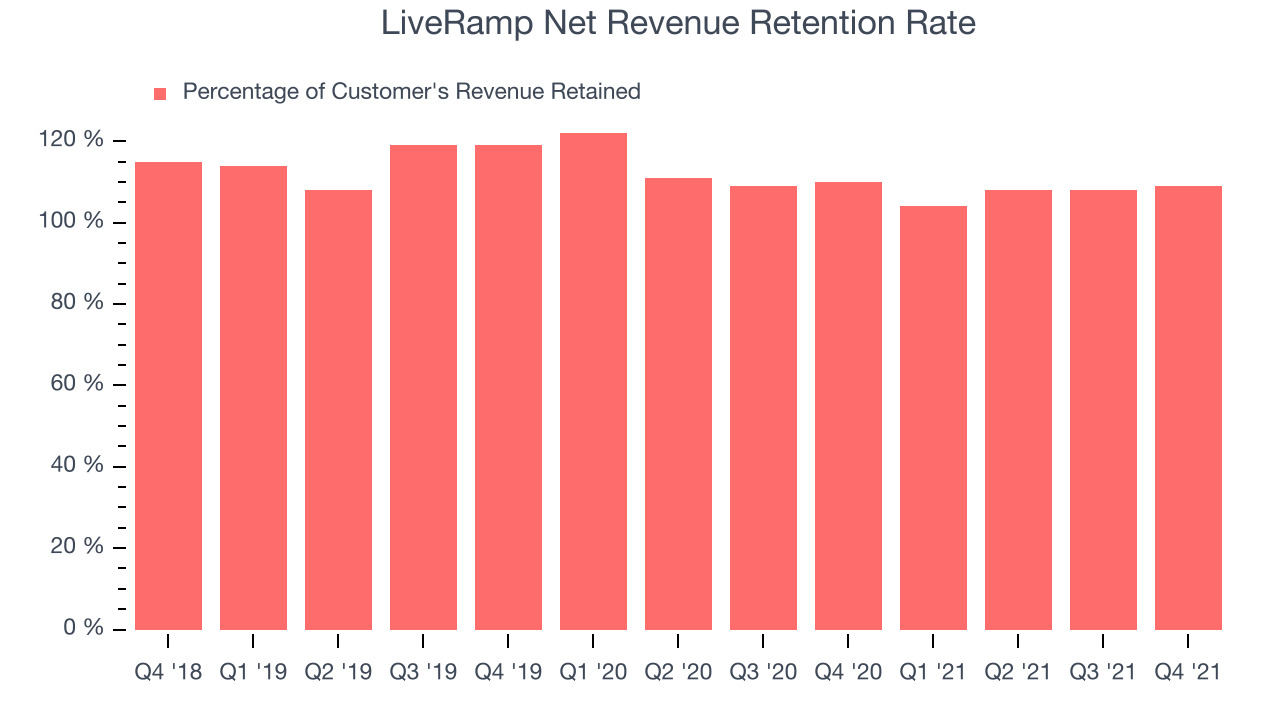

One of the best things about software as a service businesses (and a reason why they trade at such high multiples) is that customers tend to spend more with the company over time.

LiveRamp's net revenue retention rate, an important measure of how much customers from a year ago were spending at the end of the quarter, was at 109% in Q3. That means even if they didn't win any new customers, LiveRamp would have grown its revenue 9% year on year. That is a decent retention rate and it shows us that not only LiveRamp's customers stick around but at least some of them get increasing value from its software over time.

Key Takeaways from LiveRamp's Q3 Results

With a market capitalization of $3.03 billion LiveRamp is among smaller companies, but its more than $552.9 million in cash and the fact it is operating close to free cash flow break-even put it in a robust financial position to invest in growth.

We enjoyed seeing LiveRamp’s strong acceleration in customer growth this quarter. And we were also happy to see it topped analysts’ revenue expectations, even if just narrowly. On the other hand, it was unfortunate to see that the revenue guidance for the next quarter missed analysts' expectations. Zooming out, we think this was still a decent, albeit mixed, quarter, showing the company is staying on target. The company is up 3.01% on the results and currently trades at $45.77 per share.

Should you invest in LiveRamp right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.