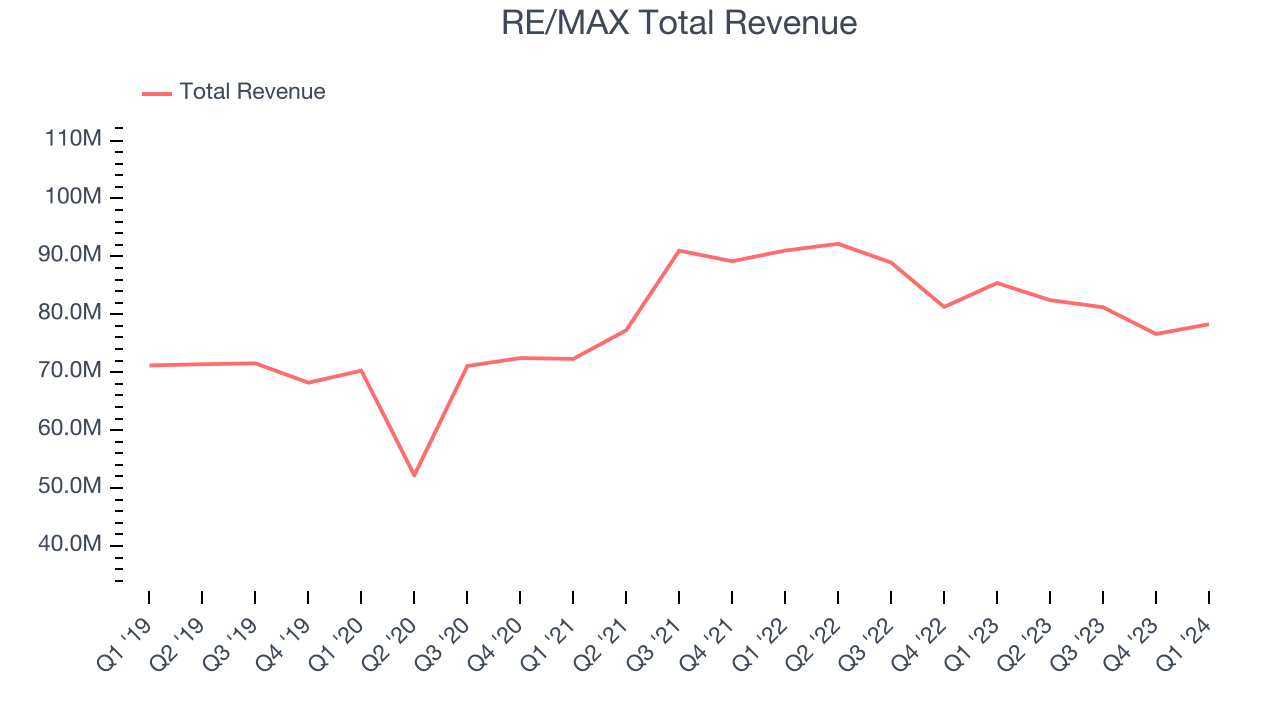

Real estate franchise company RE/MAX (NYSE:RMAX) announced better-than-expected results in Q1 CY2024, with revenue down 8.3% year on year to $78.29 million. On the other hand, next quarter's revenue guidance of $77.5 million was less impressive, coming in 1.6% below analysts' estimates. It made a non-GAAP profit of $0.20 per share, down from its profit of $0.26 per share in the same quarter last year.

Is now the time to buy RE/MAX? Find out by accessing our full research report, it's free.

RE/MAX (RMAX) Q1 CY2024 Highlights:

- Revenue: $78.29 million vs analyst estimates of $77.26 million (1.3% beat)

- EPS (non-GAAP): $0.20 vs analyst expectations of $0.19 (in line)

- Revenue Guidance for Q2 CY2024 is $77.5 million at the midpoint, below analyst estimates of $78.76 million

- The company reconfirmed its revenue guidance for the full year of $310 million at the midpoint (also reconfirmed adjusted EBITDA guidance)

- Gross Margin (GAAP): 74.2%, down from 75% in the same quarter last year

- Free Cash Flow of $6.76 million, similar to the previous quarter

- Agents: 143,287

- Market Capitalization: $135.7 million

"Effective cost management led to solid first-quarter margin performance, as we continue to operate our business as efficiently as possible amidst an environment of uncertainty," said Erik Carlson, RE/MAX Holdings Chief Executive Officer.

Short for Real Estate Maximums, RE/MAX (NYSE:RMAX) operates a real estate franchise network spanning over 100 countries and territories.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. RE/MAX's annualized revenue growth rate of 6.6% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. RE/MAX's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 4.4% over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. RE/MAX's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 4.4% over the last two years.

We can better understand the company's revenue dynamics by analyzing its number of agents, which reached 143,287 in the latest quarter. Over the last two years, RE/MAX's agents averaged 1.1% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company's monetization of its consumers has fallen.

This quarter, RE/MAX's revenue fell 8.3% year on year to $78.29 million but beat Wall Street's estimates by 1.3%. The company is guiding for a 6% year-on-year revenue decline next quarter to $77.5 million, an improvement from the 10.6% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects revenue to decline 2.6% over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

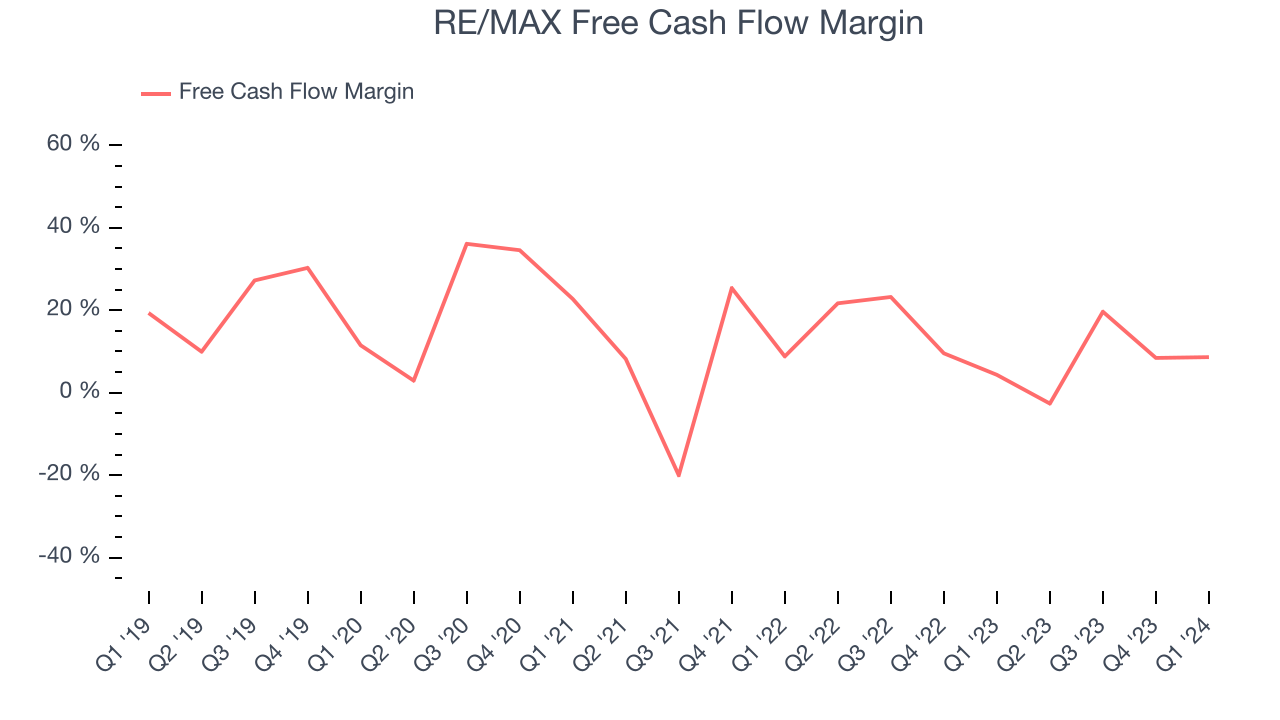

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, RE/MAX has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 11.9%, slightly better than the broader consumer discretionary sector.

RE/MAX's free cash flow came in at $6.76 million in Q1, equivalent to a 8.6% margin and up 82.2% year on year.

Key Takeaways from RE/MAX's Q1 Results

It was encouraging to see RE/MAX narrowly top analysts' revenue expectations this quarter. We were also happy its EPS narrowly outperformed Wall Street's estimates. That the company reaffirmed full year revenue and adjusted EBITDA guidance means the company is on track. On the other hand, its operating margin missed and its number of agents fell short of Wall Street's estimates. Overall, this was a fine quarter for RE/MAX. The stock is up 5.3% after reporting and currently trades at $7.55 per share.

So should you invest in RE/MAX right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.