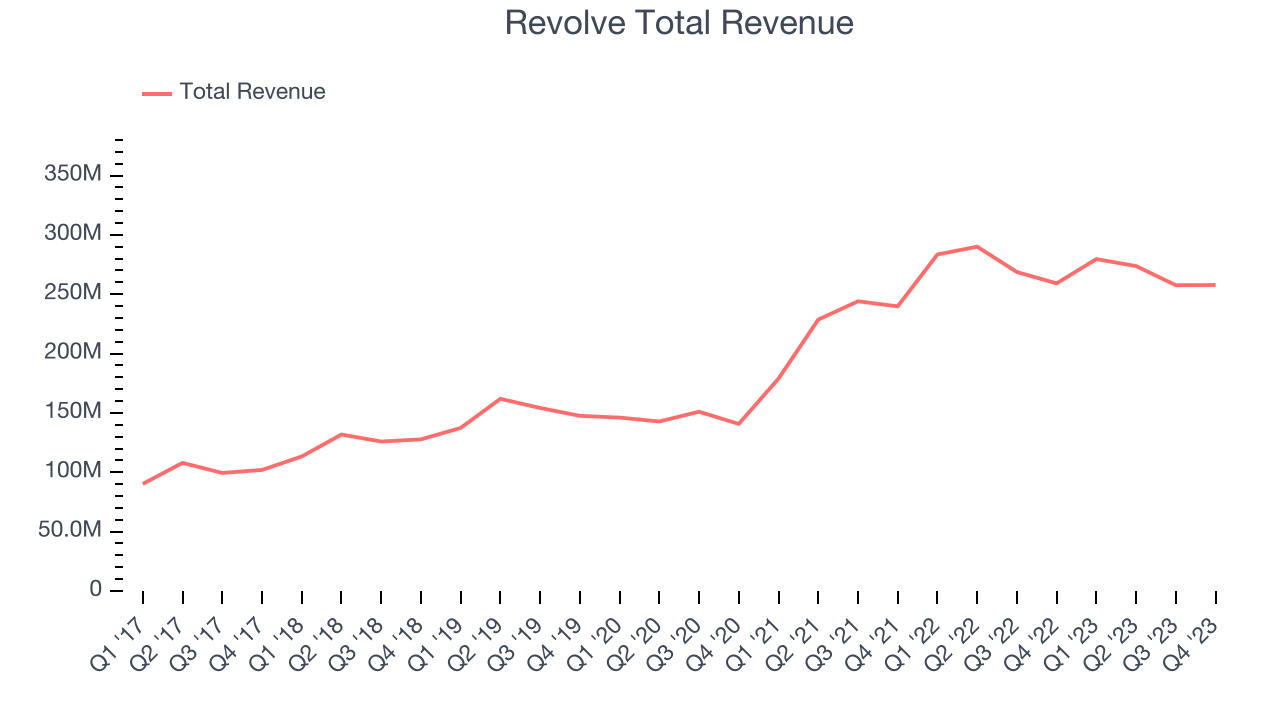

Online fashion retailer Revolve Group (NASDAQ: RVLV) announced better-than-expected results in Q4 FY2023, with revenue flat year on year at $257.8 million. It made a GAAP profit of $0.05 per share, down from its profit of $0.11 per share in the same quarter last year.

Revolve (RVLV) Q4 FY2023 Highlights:

- Revenue: $257.8 million vs analyst estimates of $246 million (4.8% beat)

- EPS: $0.05 vs analyst estimates of $0.02 ($0.03 beat)

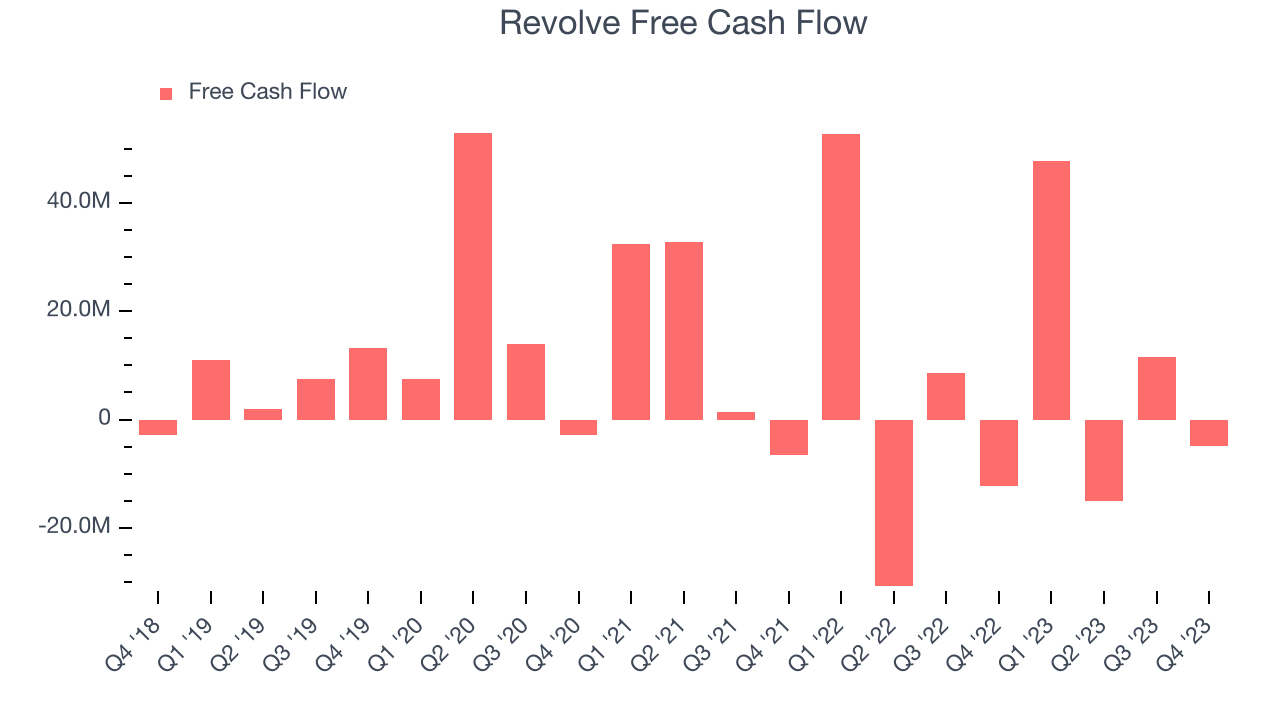

- Free Cash Flow was -$4.96 million, down from $11.49 million in the previous quarter

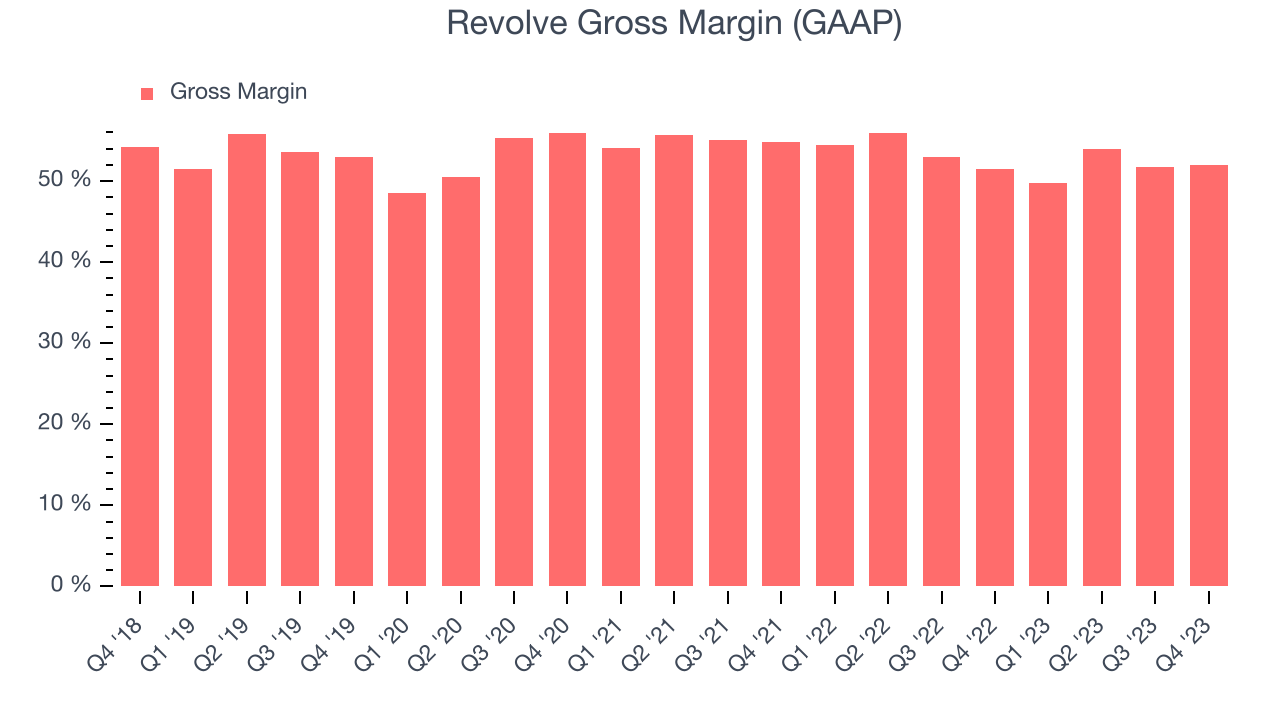

- Gross Margin (GAAP): 52%, up from 51.4% in the same quarter last year

- Trailing 12 months Active Customers : 2.54 million, up 203,000 year on year

- Market Capitalization: $1.22 billion

Launched in 2003 by software engineers Michael Mente and Mike Karanikolas, Revolve Group (NASDAQ: RVLV) is a next generation fashion retailer that leverages social media and a community of fashion influencers to drive its merchandising strategy.

Revolve Group is focused on Millennials and Generation Z customers, who spend significant amounts of time on social media, and often look to social media and digital content from influencers as their source of inspiration and discovery and to inform their purchasing decisions. Revolve has taken a data-driven buying and merchandising model, which monitors and also spends its marketing dollars on a network of over 3,500 social media influencers’ fashion choices on TikTok, Instagram, and YouTube. The company’s ‘read and react’ merchandising approach identifies and invests behind new trends in small initial order quantities. The company employs a “test and reorder” model, which like brick and mortar fast fashion peers creates scarcity, while also minimizing fashion risk.

The company has two main brands. Revolve which focuses on constant newness and a broad yet curated assortment of premium apparel and footwear, accessories and beauty products. Its Forward brand is meant to offer an emerging luxury brand feel.

Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Revolve Group (NYSE: RVLV) competes with Stitchfix (NASDAQ: SFIX), The RealReal (NASDAQ:REAL), Poshmark (NASDAQ: POSH), Asos (AIM:ASC), and boohoo group (AIM:BOO).

Sales Growth

Revolve's revenue growth over the last three years has been strong, averaging 25.5% annually. This quarter, Revolve beat analysts' estimates but reported a year on year revenue decline of 0.5%.

Usage Growth

As an online retailer, Revolve generates revenue growth by expanding its number of buyers and the average order size in dollars.

Over the last two years, Revolve's active buyers, a key performance metric for the company, grew 23.9% annually to 2.54 million. This is strong growth for a consumer internet company.

In Q4, Revolve added 203,000 active buyers, translating into 8.7% year-on-year growth.

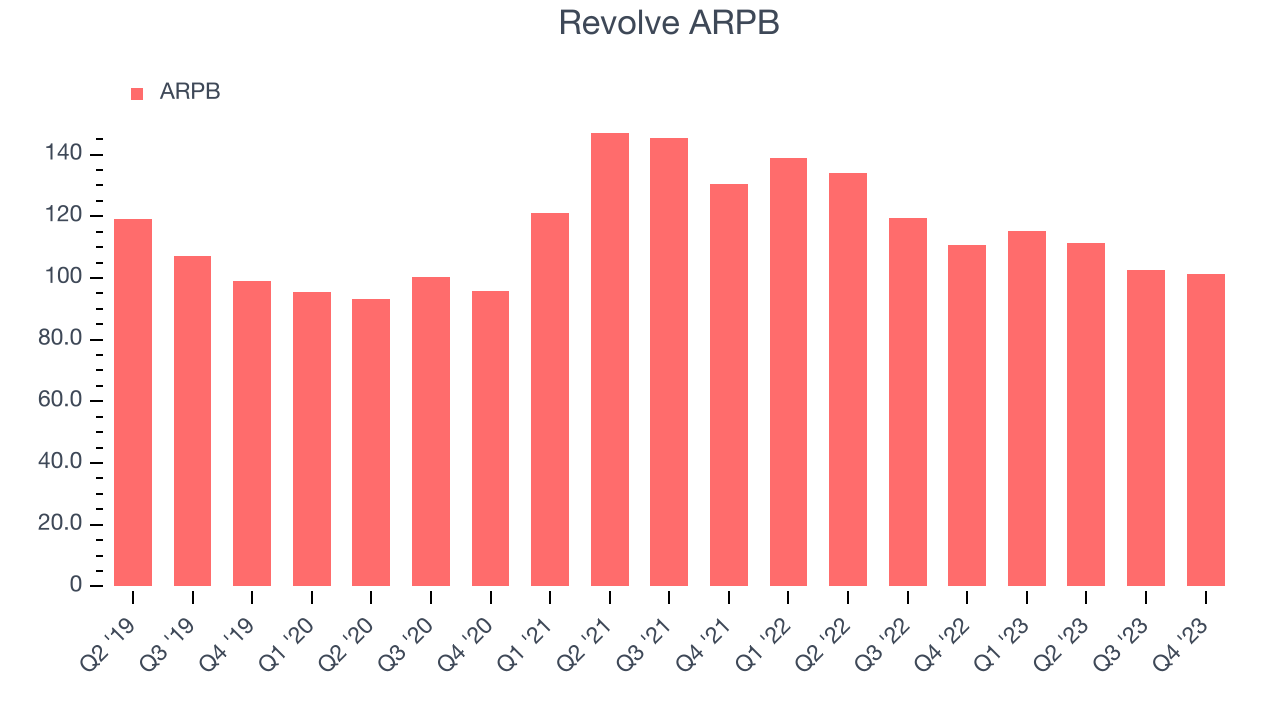

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track for consumer internet businesses like Revolve because it measures how much customers spend per order.

Revolve's ARPB has declined over the last two years, averaging 10.4%. Although it's unfortunate to see the company lose its pricing power, it was still able to achieve strong buyer growth. This quarter, ARPB declined 8.5% year on year to $101.37 per buyer.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor.

Revolve's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 52% this quarter, up 0.6 percentage points year on year.

For online retail (separate from online marketplaces) businesses like Revolve, these aforementioned costs typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure expenses. After paying for these expenses, Revolve had $0.52 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

Revolve's gross margins have been trending down over the past year, averaging 51.9%. This weakness isn't great as Revolve's margins are already slightly below other consumer internet companies and falling margins point to potentially deteriorating pricing power.

User Acquisition Efficiency

Consumer internet businesses like Revolve grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It's expensive for Revolve to acquire new users as the company has spent 58% of its gross profit on sales and marketing expenses over the last year. This relative inefficiency indicates that Revolve's product offering can be easily replicated and that it must continue investing to maintain its growth trajectory.

Profitability & Free Cash Flow

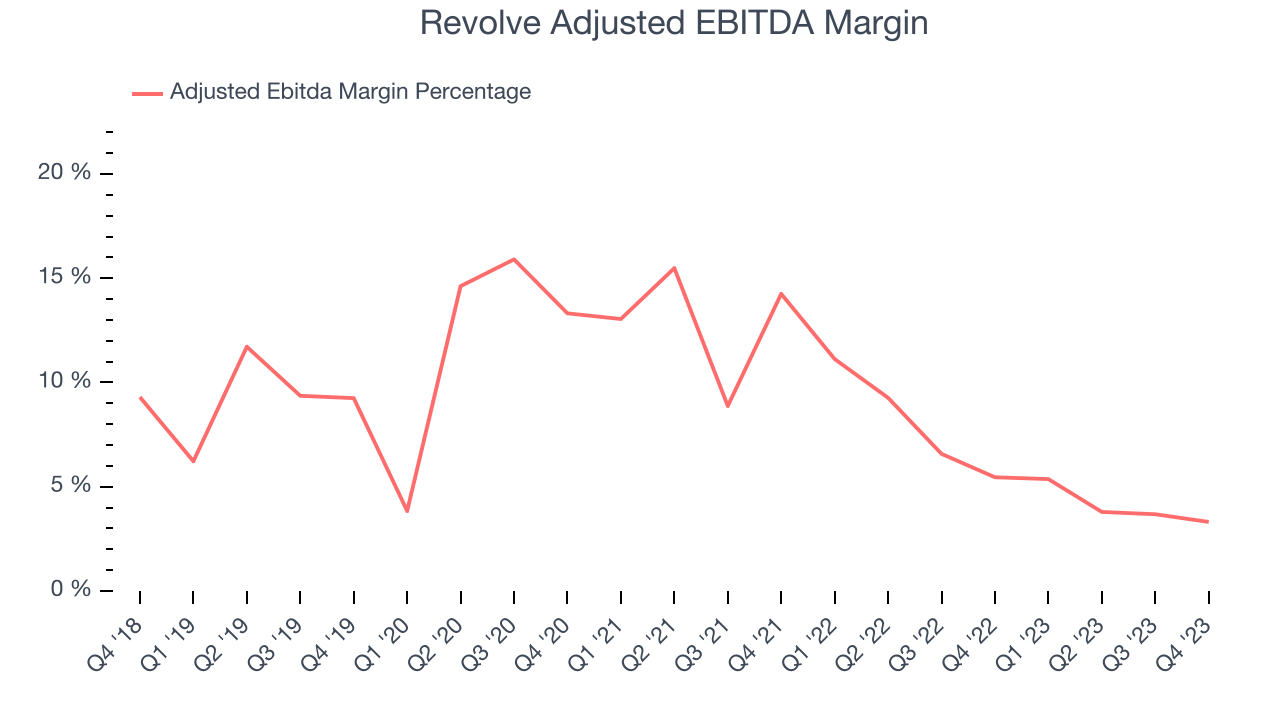

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

This quarter, Revolve's EBITDA came in at $8.54 million, resulting in a 3.3% margin. The company has also shown above-average profitability for a consumer internet business over the last four quarters, with average EBITDA margins of 4.1%.

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Revolve burned through $4.96 million in Q4, increasing the cash burn by 59.6% year on year.

Revolve has generated $39.14 million in free cash flow over the last 12 months, or 3.7% of revenue. This FCF margin stems from its efficient business model and enables it to reinvest in its business without depending on the capital markets.

Key Takeaways from Revolve's Q4 Results

It was great to see Revolve beat analysts' revenue expectations this quarter. We were also glad it expanded its user base. On the other hand, its revenue growth regrettably slowed. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 3% after reporting and currently trades at $17.99 per share.

Is Now The Time?

When considering an investment in Revolve, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in the case of Revolve, we'll be cheering from the sidelines. Although its revenue growth has been good over the last three years, Wall Street expects growth to deteriorate from here. And while its growth in active buyers has been strong, the downside is its ARPU has declined over the last two years. On top of that, its sales and marketing efficiency is sub-average.

At the moment Revolve trades at 24.3x next 12 months EV-to-EBITDA. While we have no doubt one can find things to like about the company, we think there might be better opportunities in the market and at the moment don't see many reasons to get involved.

Wall Street analysts covering the company had a one-year price target of $16.76 per share right before these results (compared to the current share price of $17.99), implying they didn't see much short-term potential in the Revolve.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.