Cyber security company SentinelOne (NYSE:S) missed analyst expectations in Q1 FY2024 quarter, with revenue up 70.5% year on year to $133.4 million. Guidance for the next quarter also missed analyst expectations with revenues guided to $141 million at the midpoint, or 7.28% below analyst estimates. SentinelOne made a GAAP loss of $106.9 million, down on its loss of $89.8 million, in the same quarter last year.

Is now the time to buy SentinelOne? Access our full analysis of the earnings results here, it's free.

SentinelOne (S) Q1 FY2024 Highlights:

- Revenue: $133.4 million vs analyst estimates of $136.6 million (2.36% miss)

- EPS (non-GAAP): -$0.15 vs analyst estimates of -$0.17

- Revenue guidance for Q2 2024 is $141 million at the midpoint, below analyst estimates of $152.1 million

- The company dropped revenue guidance for the full year, from $635.5 million to $595 million at the midpoint, a 6.37% decrease

- Free cash flow was negative $31.4 million, compared to negative free cash flow of $25.4 million in previous quarter

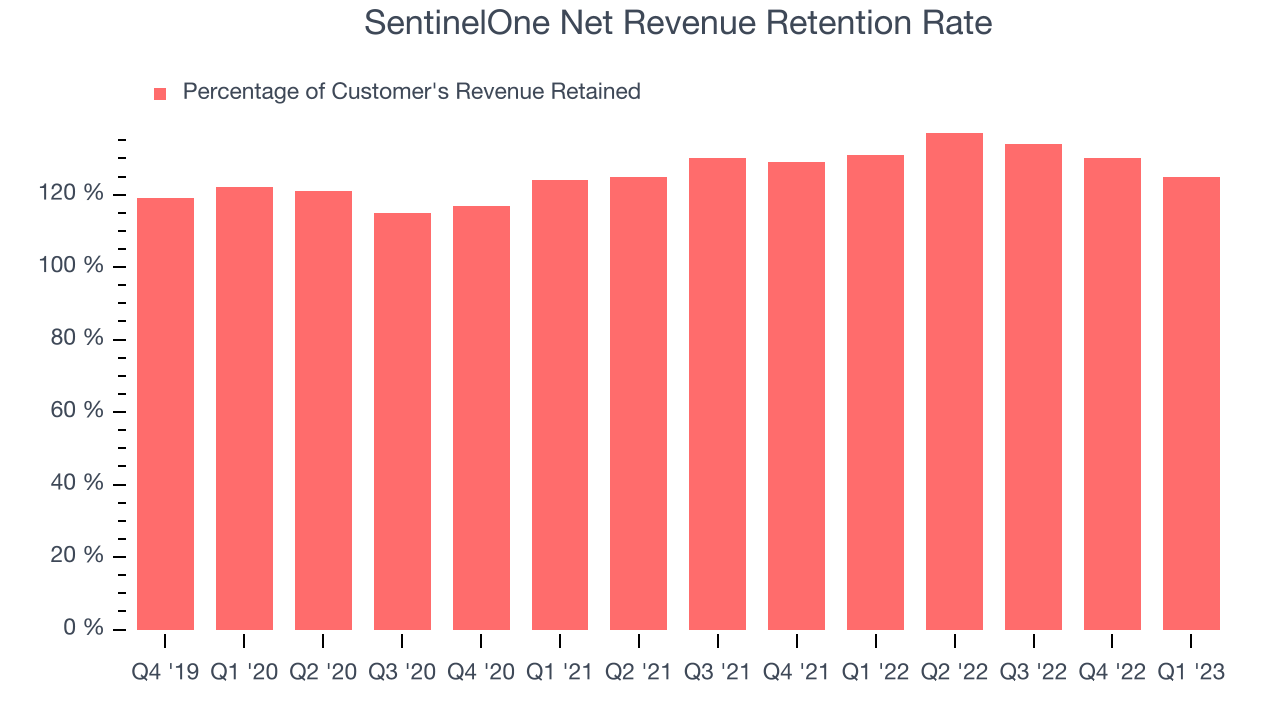

- Net Revenue Retention Rate: 125%, down from 130% previous quarter

- Customers: 10,680, up from 10,000 in previous quarter

- Gross Margin (GAAP): 68.1%, up from 65.3% same quarter last year

“Macro challenges remained, yet we continued to deliver high growth and margin improvement, demonstrating key strengths across our business. Once again we're leading the industry with the innovation in AI with our recently launched Purple AI: a one-of-a-kind innovation in cybersecurity that empowers enterprises with unparalleled capabilities to offer a real-time, autonomous response against cyber threats,” said Tomer Weingarten, CEO of SentinelOne.

With roots in the Israeli cyber intelligence community, SentinelOne (NYSE:S) provides software to help organizations efficiently detect, prevent, and investigate cyber attacks.

Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks. As the volume of internet enabled devices grows, every device that employees use to connect to business networks represents a potential risk. Endpoint security software enables businesses to protect devices (endpoints) that employees use for work purposes either on a network or in the cloud from cyber threats.

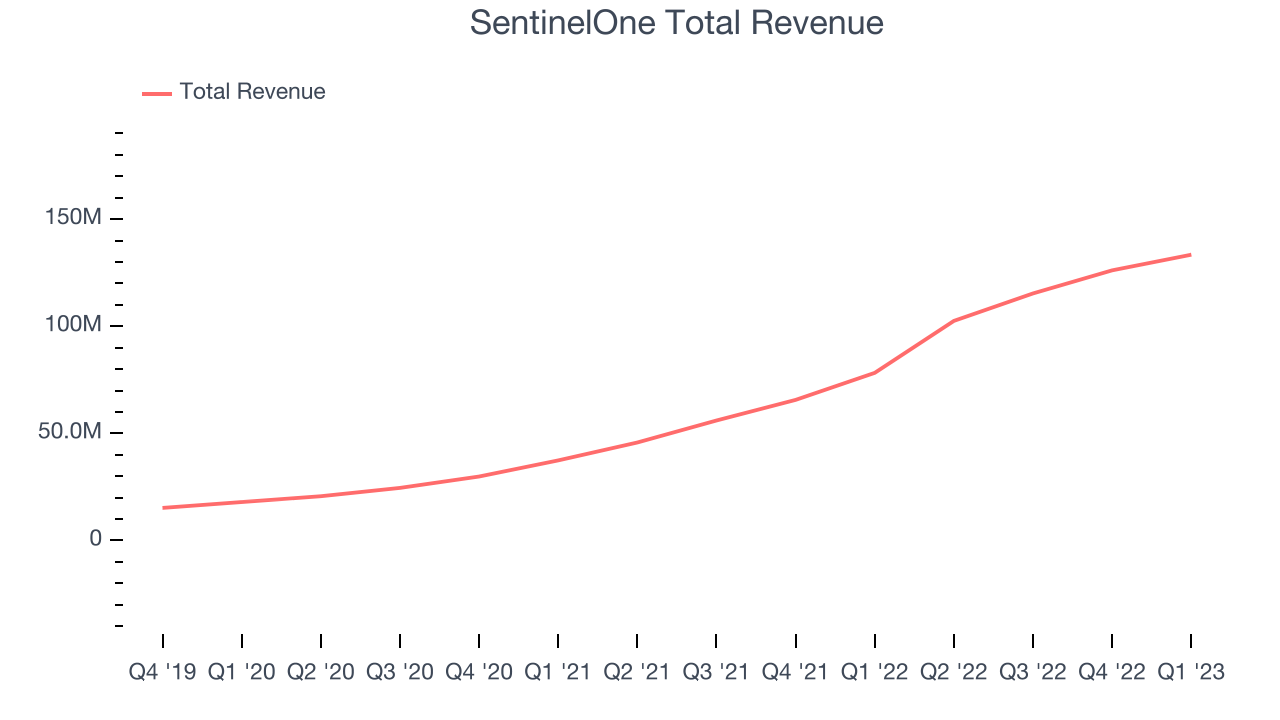

Sales Growth

As you can see below, SentinelOne's revenue growth has been incredible over the last two years, growing from quarterly revenue of $37.4 million in Q1 FY2022, to $133.4 million.

And while we saw even higher rates of growth previously, the revenue growth was still very strong; up a rather splendid 70.5% year on year. But the growth did slow down compared to last quarter, as the revenue increased by just $7.3 million in Q1, compared to $10.8 million in Q4 2023. We'd like to see revenue increase by a greater amount each quarter, but a one-off fluctuation is usually not concerning.

Guidance for the next quarter indicates SentinelOne is expecting revenue to grow 37.6% year on year to $141 million, slowing down from the 124% year-over-year increase in revenue the company had recorded in the same quarter last year. Ahead of the earnings results the analysts covering the company were estimating sales to grow 45.7% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Product Success

One of the best things about software as a service businesses (and a reason why they trade at such high multiples) is that customers tend to spend more with the company over time.

SentinelOne's net revenue retention rate, an important measure of how much customers from a year ago were spending at the end of the quarter, was at 125% in Q1. That means even if they didn't win any new customers, SentinelOne would have grown its revenue 25% year on year. Despite the recent drop this is still a good retention rate and a proof that SentinelOne's customers are satisfied with their software and are getting more value from it over time. That is good to see.

Key Takeaways from SentinelOne's Q1 Results

Since it has still been burning cash over the last twelve months it is worth keeping an eye on SentinelOne’s balance sheet, but we note that with a market capitalization of $6.23 billion and more than $718.2 million in cash, the company has the capacity to continue to prioritise growth over profitability.

It was good to see the company reduce cash burn this quarter. On the other hand, it was unfortunate to see that SentinelOne's revenue guidance missed analysts' expectations and indicates a pessimistic outlook. Overall, this quarter's results could have been better. The market was pricing the company for perfection and as a result of the miss it is down 32.5% on the results and currently trades at $14 per share.

SentinelOne may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.