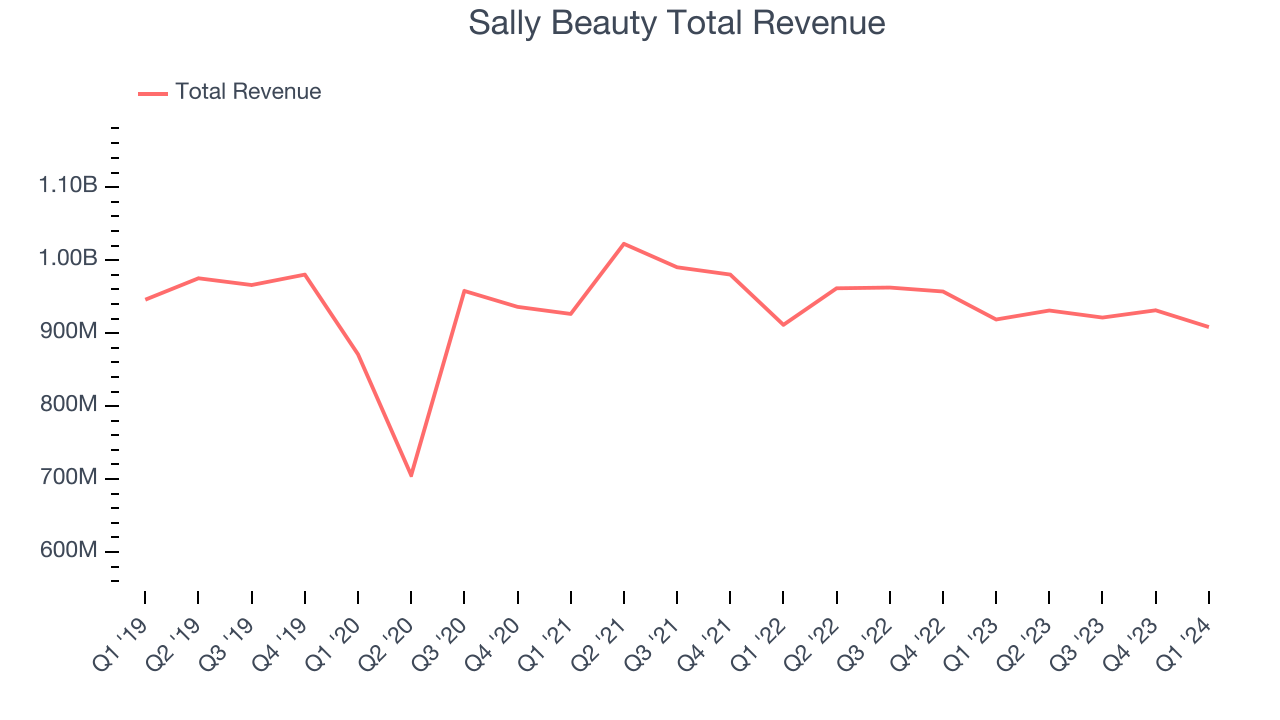

Beauty supply retailer Sally Beauty (NYSE:SBH) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 1.1% year on year to $908.4 million. It made a non-GAAP profit of $0.35 per share, down from its profit of $0.41 per share in the same quarter last year.

Is now the time to buy Sally Beauty? Find out by accessing our full research report, it's free.

Sally Beauty (SBH) Q1 CY2024 Highlights:

- Revenue: $908.4 million vs analyst estimates of $910.8 million (small miss)

- EPS (non-GAAP): $0.35 vs analyst expectations of $0.39 (11.2% miss)

- Gross Margin (GAAP): 51%, in line with the same quarter last year

- Free Cash Flow of $22.83 million, up from $7.52 million in the same quarter last year

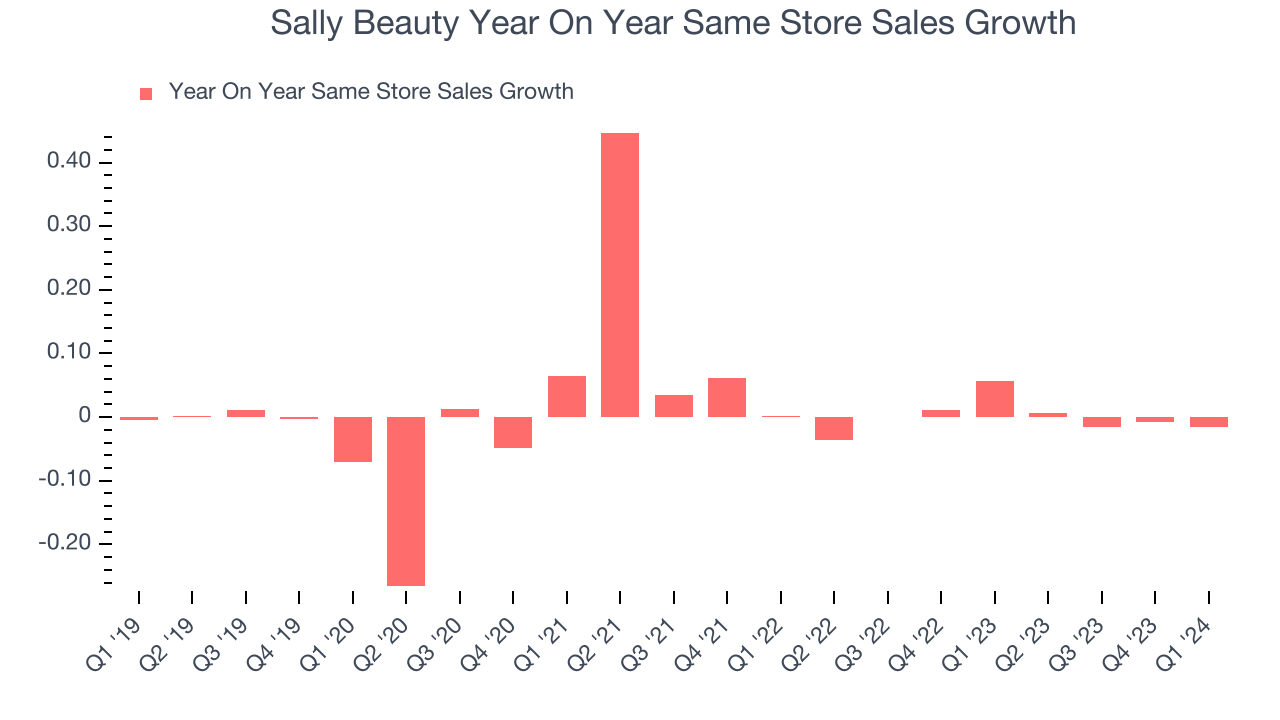

- Same-Store Sales were down 1.5% year on year

- Store Locations: 4,468 at quarter end, decreasing by 16 over the last 12 months

- Market Capitalization: $1.13 billion

“Our second quarter performance reflects the benefits of expanded distribution, product innovation and the strengthening of salon demand trends in our Beauty Systems Group segment, offset by moderating traffic and customer purchasing patterns in our Sally Beauty segment resulting from the inflationary environment,” said Denise Paulonis, President and Chief Executive Officer.

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE:SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Beauty and Cosmetics Retailer

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Sales Growth

Sally Beauty is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

As you can see below, the company's revenue has declined over the last four years, dropping 1.1% annually as its store count and sales at existing, established stores have both shrunk.

This quarter, Sally Beauty missed Wall Street's estimates and reported a rather uninspiring 1.1% year-on-year revenue decline, generating $908.4 million in revenue. Looking ahead, Wall Street expects sales to grow 1.3% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

Sally Beauty's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 0% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Sally Beauty's same-store sales fell 1.5% year on year. This decline was a reversal from the 5.7% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Sally Beauty's Q1 Results

We struggled to find many strong positives in these results. Its revenue and EPS missed analysts' expectations. Overall, this was a bad quarter for Sally Beauty. The company is down 4.5% on the results and currently trades at $10.33 per share.

Sally Beauty may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.