Funeral services company Service International (NYSE:SCI) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 1.6% year on year to $1.05 billion. It made a non-GAAP profit of $0.89 per share, down from its profit of $0.93 per share in the same quarter last year.

Service International (SCI) Q1 CY2024 Highlights:

- Revenue: $1.05 billion vs analyst estimates of $1.02 billion (2.7% beat)

- EPS (non-GAAP): $0.89 vs analyst estimates of $0.85 (4.6% beat)

- Full year 2024 EPS (non-GAAP): $3.65, in line with analyst estimates

- Gross Margin (GAAP): 26.2%, down from 28.1% in the same quarter last year

- Free Cash Flow of $140.3 million, down 23.5% from the previous quarter

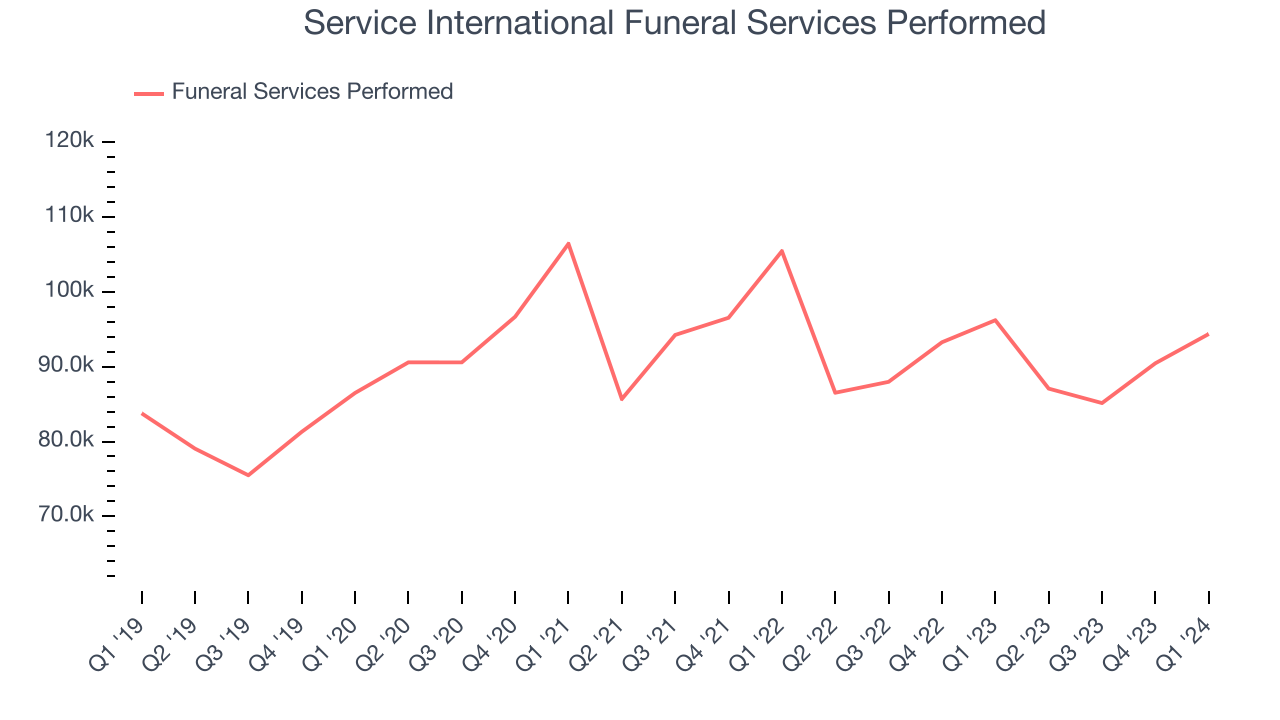

- Funeral Services Performed: 94,366 vs analyst estimates of 92,874 (1.6% beat)

- Market Capitalization: $10.51 billion

Founded in 1962, Service International (NYSE: SCI) is a leading provider of death care products and services in North America.

Service International’s primary business involves owning and operating funeral homes and cemeteries, offering a range of services that cater to the diverse needs of families during difficult times. The company's extensive network includes over 1,500 funeral homes and around 400 cemeteries. These facilities provide traditional funeral, cremation, and cemetery services while selling funeral and cemetery products like caskets, urns, and burial vaults.

Service International allows its customers to customize their funeral and memorial services. This approach extends to pre-planning services, where individuals can arrange their funeral and cemetery needs in advance, providing peace of mind for themselves and their families.

Service International’s Dignity Memorial brand is one of the largest networks of funeral, cremation, and cemetery service providers in North America. Under this brand, it offers the Dignity Planning process, which includes online tools and resources to help families plan and personalize services.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Service International's primary competitors include Carriage Services (NYSE:CSV), Park Lawn (TSX:PLC), and Matthews International (NASDAQ:MATW).Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. Service International's annualized revenue growth rate of 5.2% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Service International's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Service International's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

We can dig even further into the company's revenue dynamics by analyzing its number of funeral services performed, which reached 94,366 in the latest quarter. Over the last two years, Service International's funeral services performed averaged 3.2% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company's monetization of its consumers has risen.

This quarter, Service International reported reasonable year-on-year revenue growth of 1.6%, and its $1.05 billion of revenue topped Wall Street's estimates by 2.7%. Looking ahead, Wall Street expects sales to grow 2.2% over the next 12 months, an acceleration from this quarter.

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

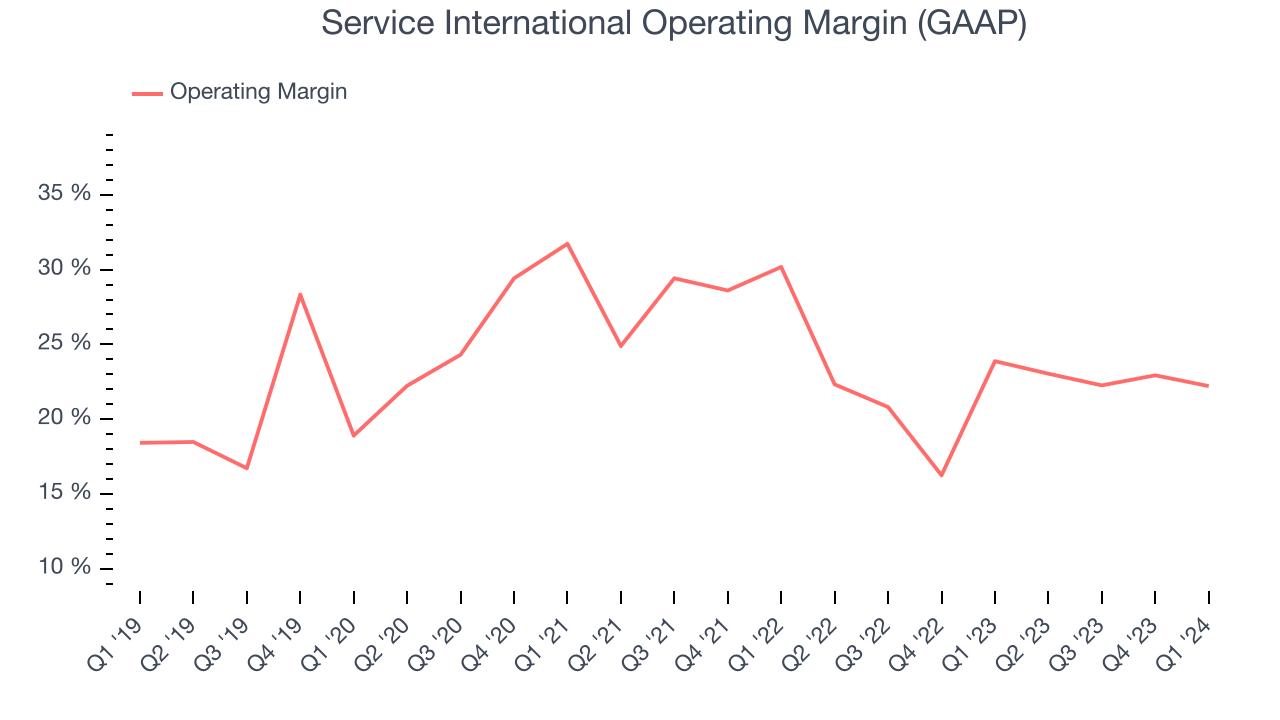

Service International has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 21.7%.

This quarter, Service International generated an operating profit margin of 22.2%, down 1.7 percentage points year on year.

Over the next 12 months, Wall Street expects Service International to maintain its LTM operating margin of 22.6%.EPS

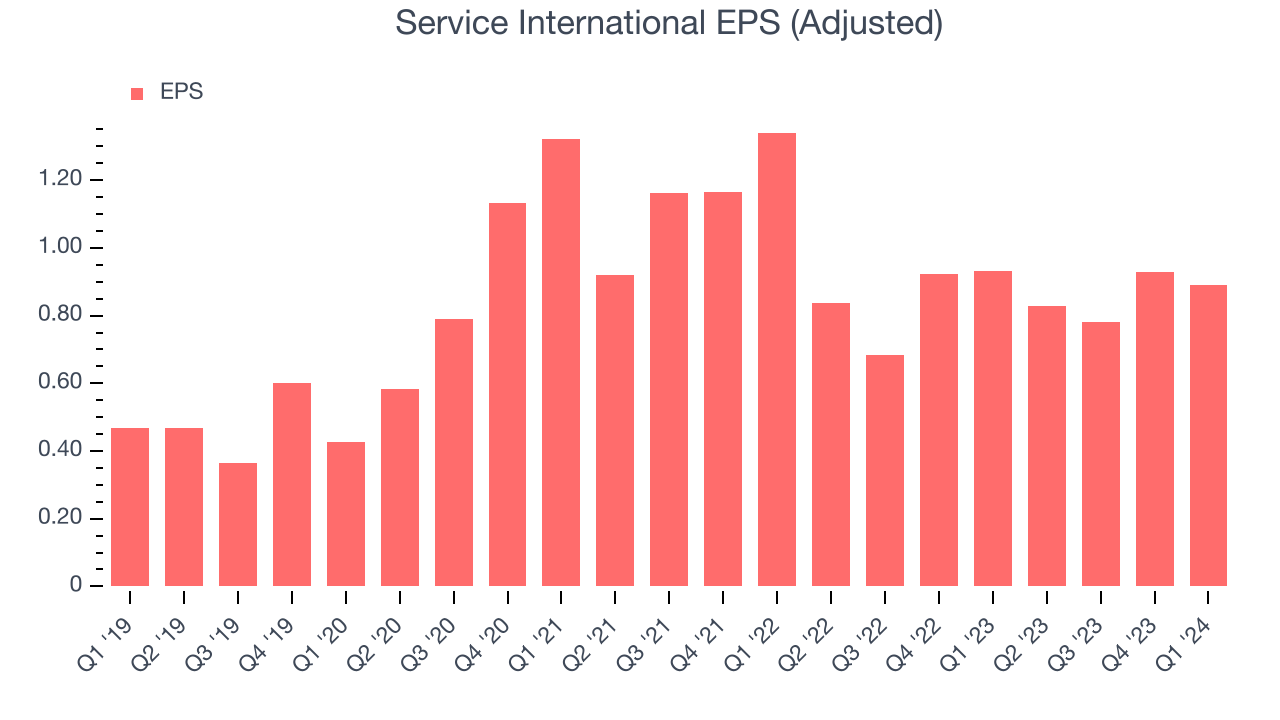

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last five years, Service International's EPS grew 91.5%, translating into a solid 13.9% compounded annual growth rate. This performance is materially higher than its 5.2% annualized revenue growth over the same period. Let's dig into why.

While we mentioned earlier that Service International's operating margin declined this quarter, a five-year view shows its margin has expanded 3.8 percentage points while its share count has shrunk 20.2%. Improving profitability and share buybacks are positive signs as they juice EPS growth relative to revenue growth.In Q1, Service International reported EPS at $0.89, down from $0.93 in the same quarter last year. Despite falling year on year, this print beat analysts' estimates by 4.6%. Over the next 12 months, Wall Street expects Service International to grow its earnings. Analysts are projecting its LTM EPS of $3.43 to climb by 9.5% to $3.76.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

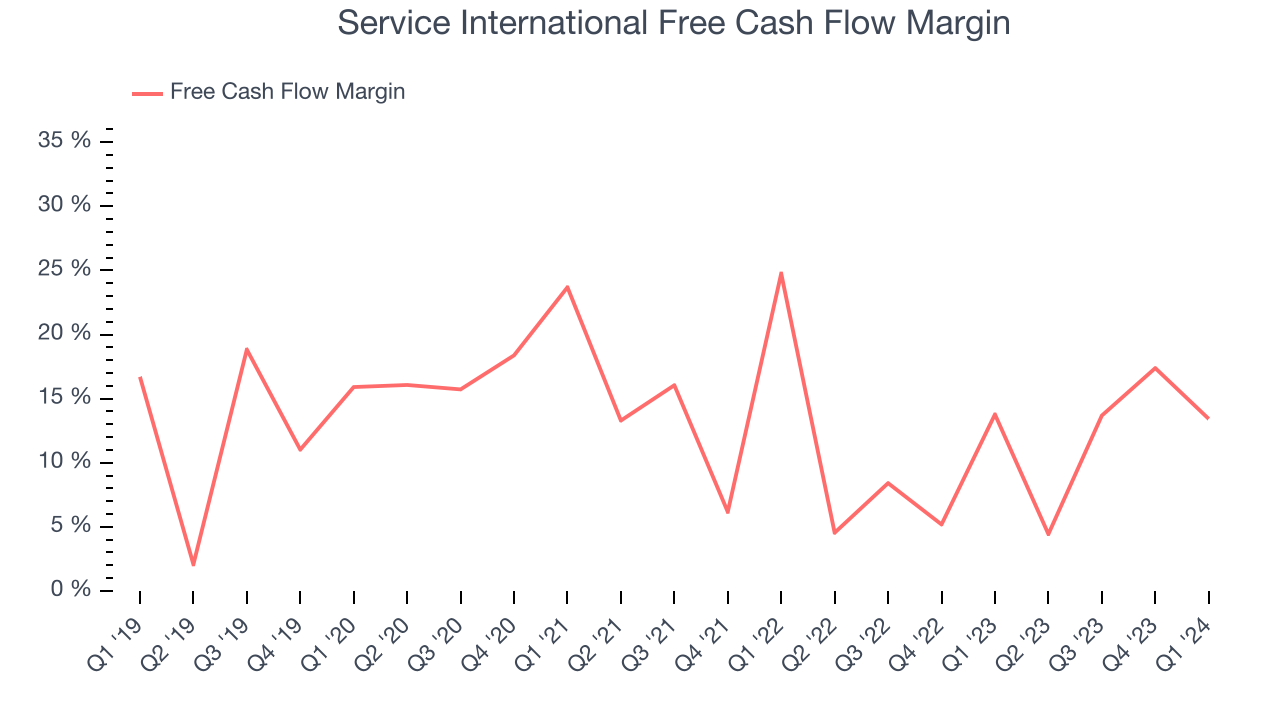

Over the last two years, Service International has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 10.2%, slightly better than the broader consumer discretionary sector.

Service International's free cash flow came in at $140.3 million in Q1, equivalent to a 13.4% margin and in line with the same quarter last year.

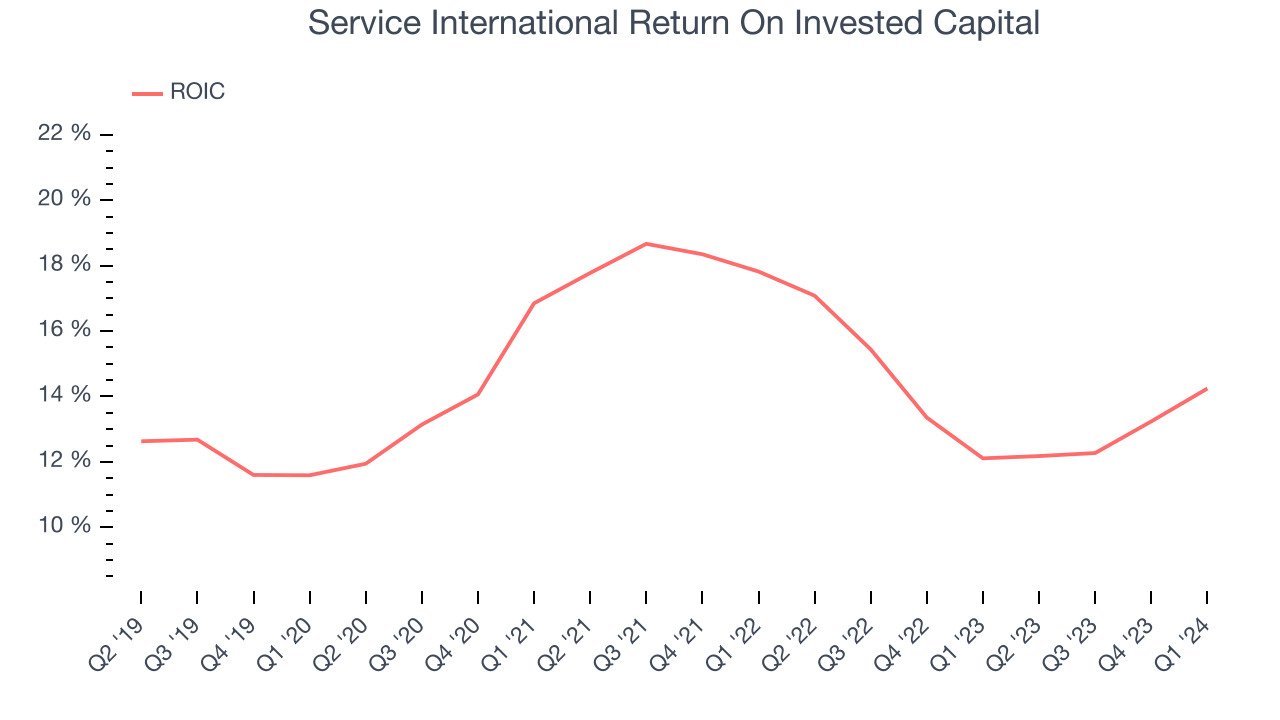

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Service International's five-year average return on invested capital was 14.5%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Service International's ROIC averaged 1 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Service International reported $205.6 million of cash and $4.68 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $1.21 billion of EBITDA over the last 12 months, we view Service International's 3.7x net-debt-to-EBITDA ratio as safe. We also see its $249.9 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Service International's Q1 Results

It was good to see Service International beat analysts' revenue expectations this quarter based on higher-than-expected volumes (funeral services performed). We were also happy its EPS narrowly outperformed Wall Street's estimates. For the full year, EPS guidance was right in line with expectations, showing no surprises in the business. Zooming out, we think this was a decent quarter, showing that the company is staying on target. The stock is flat after reporting and currently trades at $71.96 per share.

Is Now The Time?

Service International may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Service International, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last five years, and analysts expect growth to deteriorate from here. And while its impressive operating margins show it has a highly efficient business model, unfortunately, its number of funeral services performed has been disappointing.

Service International's price-to-earnings ratio based on the next 12 months is 19.0x. While we've no doubt one can find things to like about Service International, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $77.50 per share right before these results (compared to the current share price of $71.96).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.