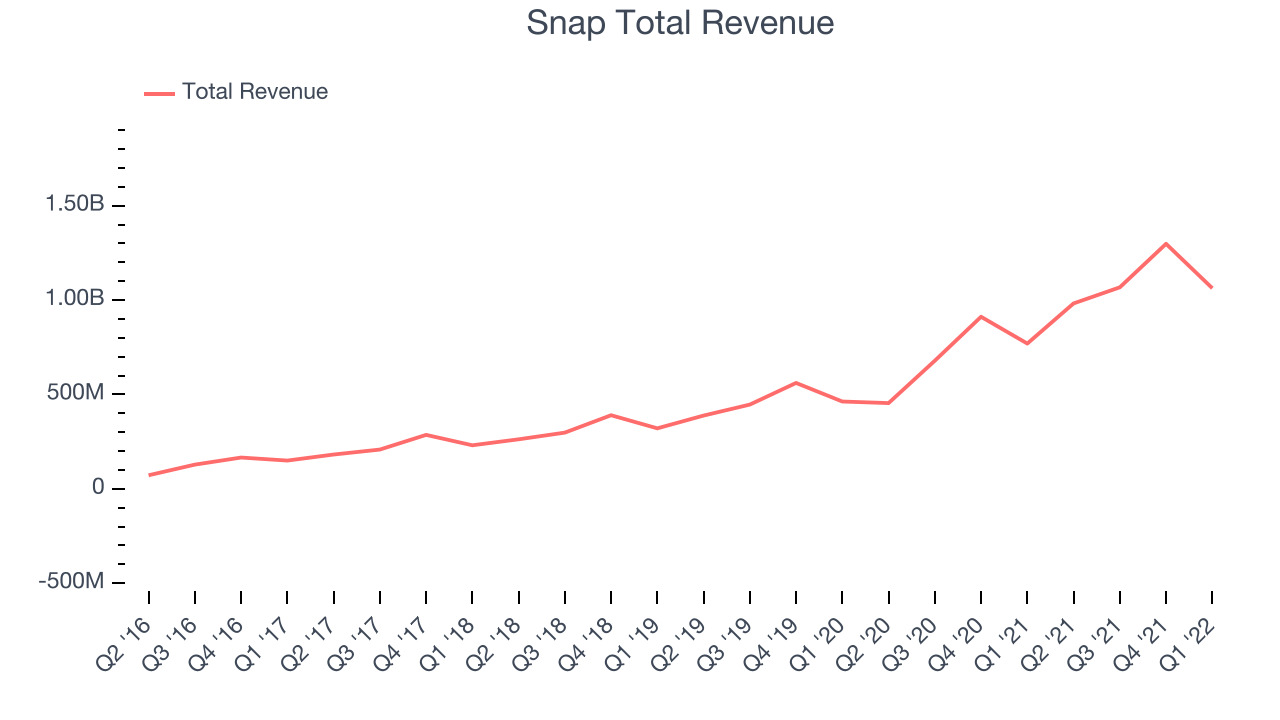

Social network Snapchat (NYSE: SNAP) missed analyst expectations in Q1 FY2022 quarter, with revenue up 38% year on year to $1.06 billion. Snap made a GAAP loss of $359.6 million, down on its loss of $286.8 million, in the same quarter last year.

Is now the time to buy Snap? Access our full analysis of the earnings results here, it's free.

Snap (SNAP) Q1 FY2022 Highlights:

- Revenue: $1.06 billion vs analyst estimates of $1.06 billion (0.57% miss)

- EPS (non-GAAP): -$0.02 vs analyst estimates of $0.01 (-$0.03 miss)

- Free cash flow of $106.2 million, down 33.9% from previous quarter

- Gross Margin (GAAP): 60.3%, up from 46.3% same quarter last year

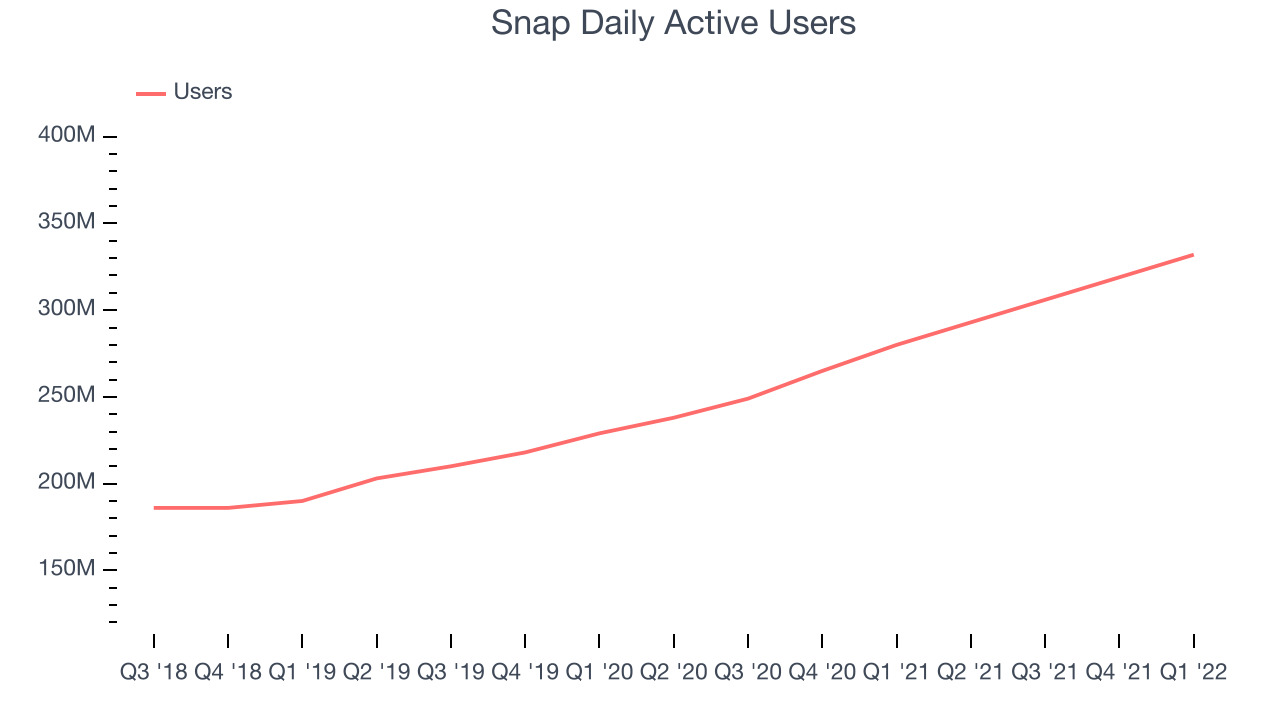

- Daily Active Users: 332 million, up 52 million year on year

“Our first quarter results reflect the underlying momentum in our business through a challenging operating environment, as we grew our community 18% year-over-year to reach 332 million, and grew our revenue 38% year-over-year to reach $1.06 billion for the quarter,” said Evan Spiegel, CEO.

Founded by Stanford University students Evan Spiegel, Reggie Brown, and Bobby Murphy, and originally called Picaboo, Snapchat (NYSE: SNAP) is an image centric social media network.

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Sales Growth

Snap's revenue growth over the last three years has been exceptional, averaging 53.1% annually.

This quarter, Snap reported an excellent 38% year on year revenue growth, but this result fell short of what analysts were expecting.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 38.1% over the next twelve months.

There are others doing even better than Snap. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 150% since the IPO last December. You can find it on our platform for free.

Usage Growth

As a social network, Snap can generate revenue growth by increasing user numbers, and by charging more for the ads each user is exposed to.

Over the last two years the number of Snap's daily active users, a key usage metric for the company, grew 20.5% annually to 332 million users. This is a strong growth for a consumer internet company.

In Q1 the company added 52 million daily active users, translating to a 18.5% growth year on year.

Key Takeaways from Snap's Q1 Results

With a market capitalization of $49.9 billion, more than $5 billion in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

We enjoyed seeing Snap’s impressive revenue growth this quarter. And we were also glad to see the user growth. On the other hand, it was unfortunate to see that Snap missed analysts' revenue expectations. Zooming out, we think this was still a decent, albeit mixed, quarter, showing the company is staying on target. The company is up 8.2% on the results in the afterhours and currently trades at $31.79 per share.

Should you invest in Snap right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.