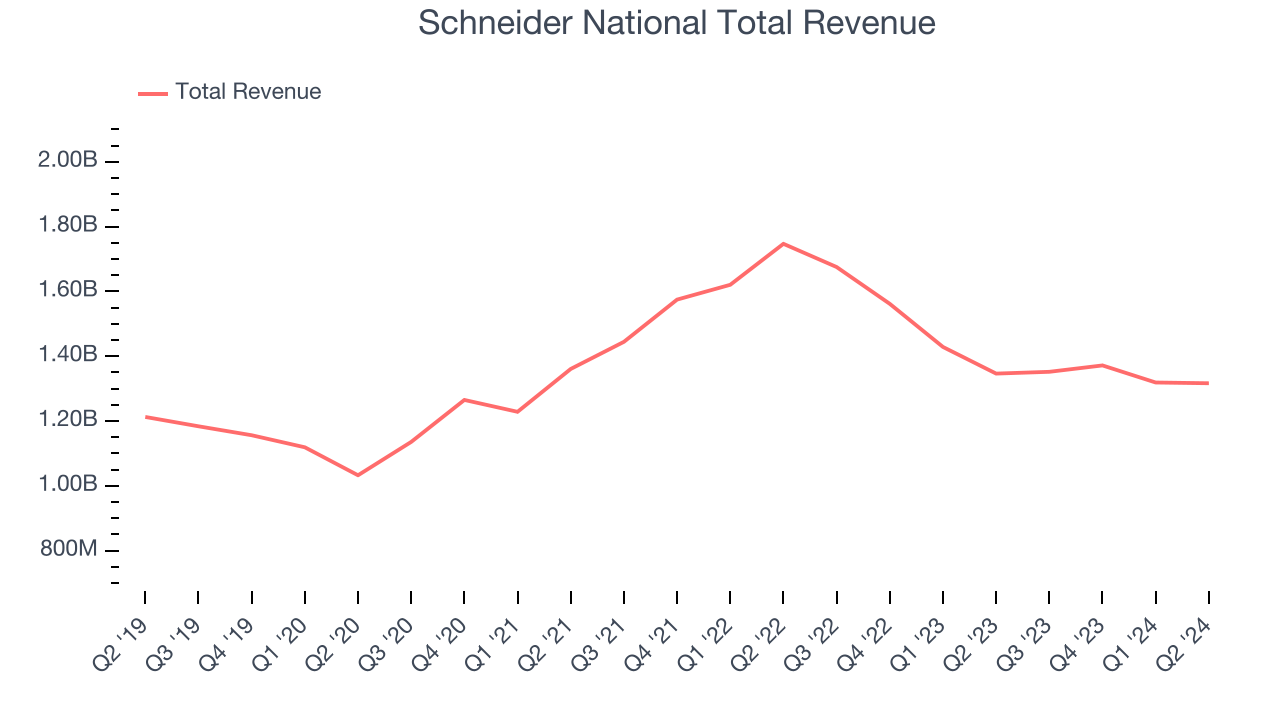

Transportation company Schneider (NYSE:SNDR) fell short of analysts' expectations in Q2 CY2024, with revenue down 2.2% year on year to $1.32 billion. It made a non-GAAP profit of $0.21 per share, down from its profit of $0.45 per share in the same quarter last year.

Is now the time to buy Schneider National? Find out by accessing our full research report, it's free.

Schneider National (SNDR) Q2 CY2024 Highlights:

- Revenue: $1.32 billion vs analyst estimates of $1.35 billion (2.7% miss)

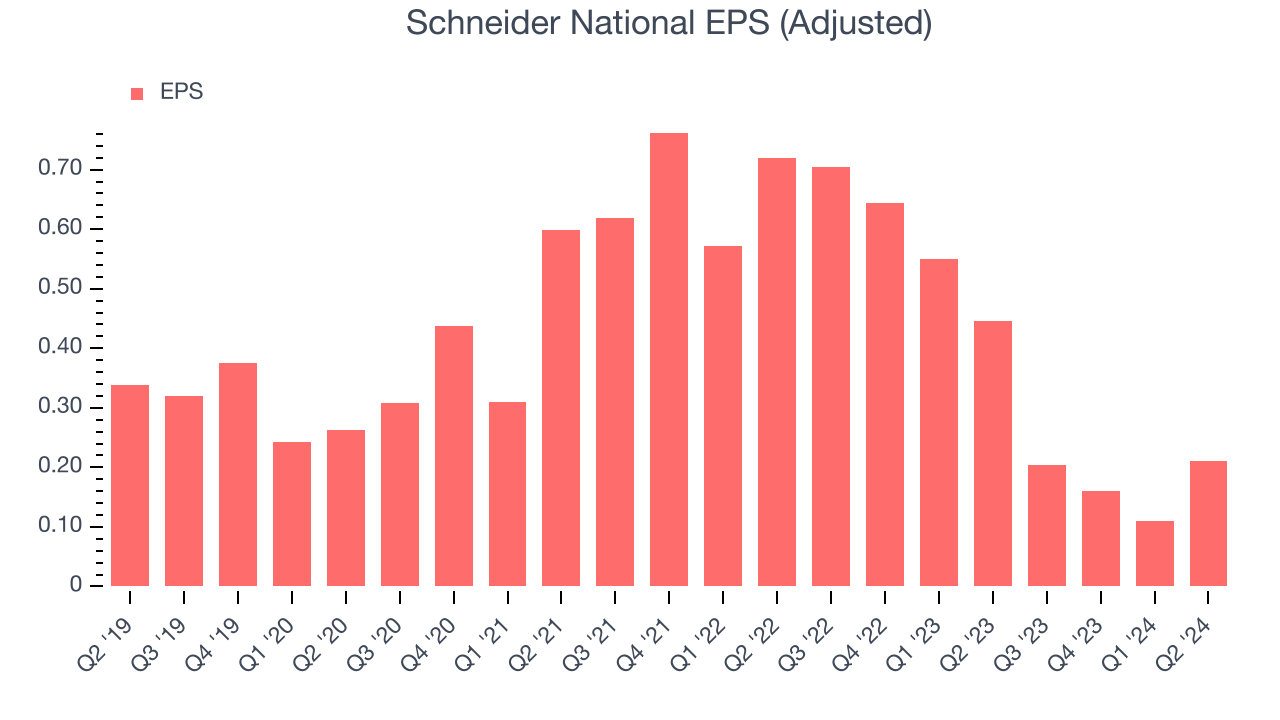

- EPS (non-GAAP): $0.21 vs analyst estimates of $0.18 (18.2% beat)

- EPS (non-GAAP) Guidance for the full year is $0.85 at the midpoint, beating analysts' estimates by 4.7%

- Gross Margin (GAAP): 16.2%, down from 18.7% in the same quarter last year

- Free Cash Flow of $108 million is up from -$9.35 million in the previous quarter

- Market Capitalization: $4.72 billion

“The second quarter showed continued progress toward market equilibrium as evidenced by moderate seasonality and a tightening spot market,” said Mark Rourke, President and Chief Executive Officer of Schneider.

Employing thousands of drivers across the country to make deliveries, Schneider (NYSE:SNDR) makes full truckload and intermodal deliveries regionally and across borders.

Ground Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, especially last-mile delivery, presenting opportunities for ground transportation companies. The industry continues to invest in data, analytics, and autonomous fleets to optimize efficiency and find the most cost-effective routes. Despite the essential services this industry provides, ground transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Regrettably, Schneider National's sales grew at a weak 1.4% compounded annual growth rate over the last five years. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Schneider National's history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 8.4% annually.

We can better understand the company's revenue dynamics by analyzing its most important segments, Truckload and Logistics, which are 41% and 24.2% of revenue. Over the last two years, Schneider National's Truckload revenue (road freight) averaged 1.2% year-on-year growth. On the other hand, its Logistics revenue (supply chain, warehousing) averaged 20% declines.

This quarter, Schneider National missed Wall Street's estimates and reported a rather uninspiring 2.2% year-on-year revenue decline, generating $1.32 billion of revenue. Looking ahead, Wall Street expects sales to grow 5.8% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

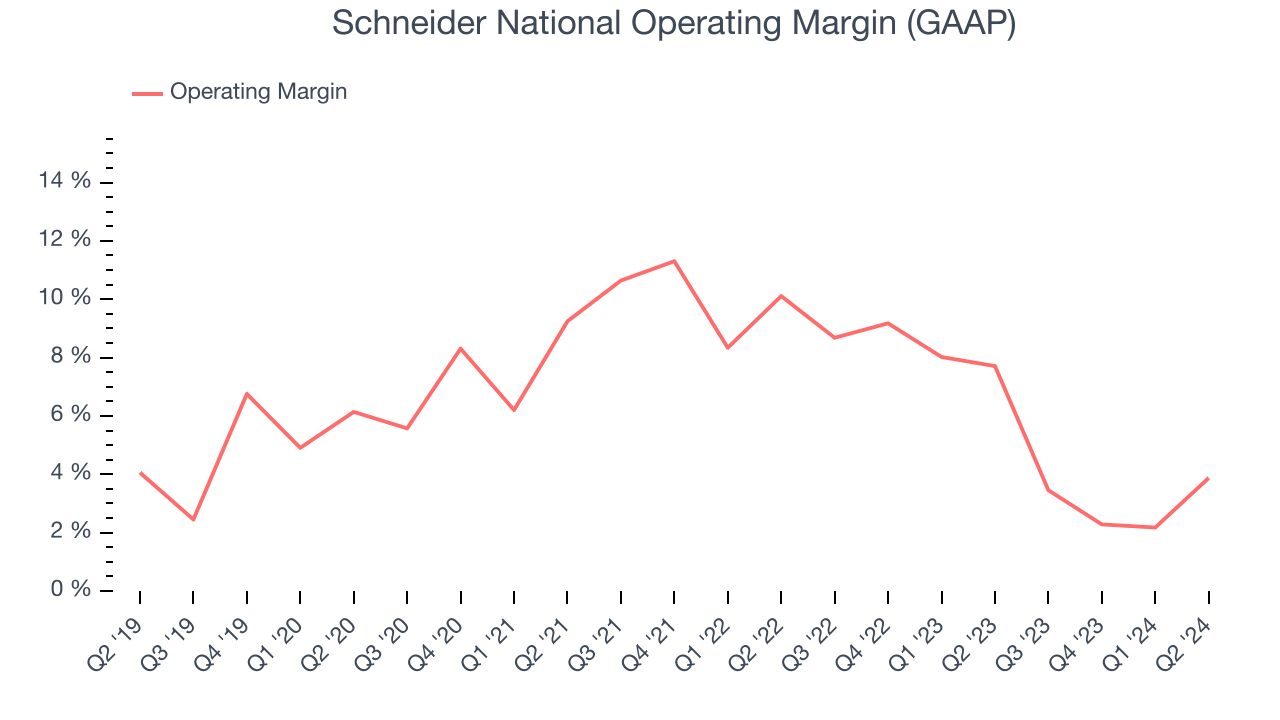

Schneider National was profitable over the last five years but held back by its large expense base. It demonstrated mediocre profitability for an industrials business, producing an average operating margin of 7%. This result isn't too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Schneider National's annual operating margin decreased by 2.1 percentage points over the last five years. The company's performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn't pass those costs onto its customers.

This quarter, Schneider National generated an operating profit margin of 3.9%, down 3.8 percentage points year on year. Since Schneider National's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Sadly for Schneider National, its EPS declined by 13.7% annually over the last five years while its revenue grew by 1.4%. This tells us the company became less profitable on a per-share basis as it expanded.

Diving into the nuances of Schneider National's earnings can give us a better understanding of its performance. As we mentioned earlier, Schneider National's operating margin declined by 2.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. Schneider National's two-year annual EPS declines of 49.4% were bad and lower than its two-year revenue performance.

In Q2, Schneider National reported EPS at $0.21, down from $0.45 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. Over the next 12 months, Wall Street expects Schneider National to grow its earnings. Analysts are projecting its EPS of $0.69 in the last year to climb by 66.6% to $1.14.

Key Takeaways from Schneider National's Q2 Results

We enjoyed seeing Schneider National exceed analysts' EPS expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street's estimates. On the other hand, its revenue missed due to weaker-than-anticipated Truckload sales, but the strong bottom-line print trumped any top-line weakness. Overall, this was a solid quarter for Schneider National. The stock traded up 4.1% to $28 immediately after reporting.

So should you invest in Schneider National right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.