Snowflake (NYSE:SNOW) Q1: Beats Estimates But Share Price Drops

Jabin Bastian /

May 26, 2021

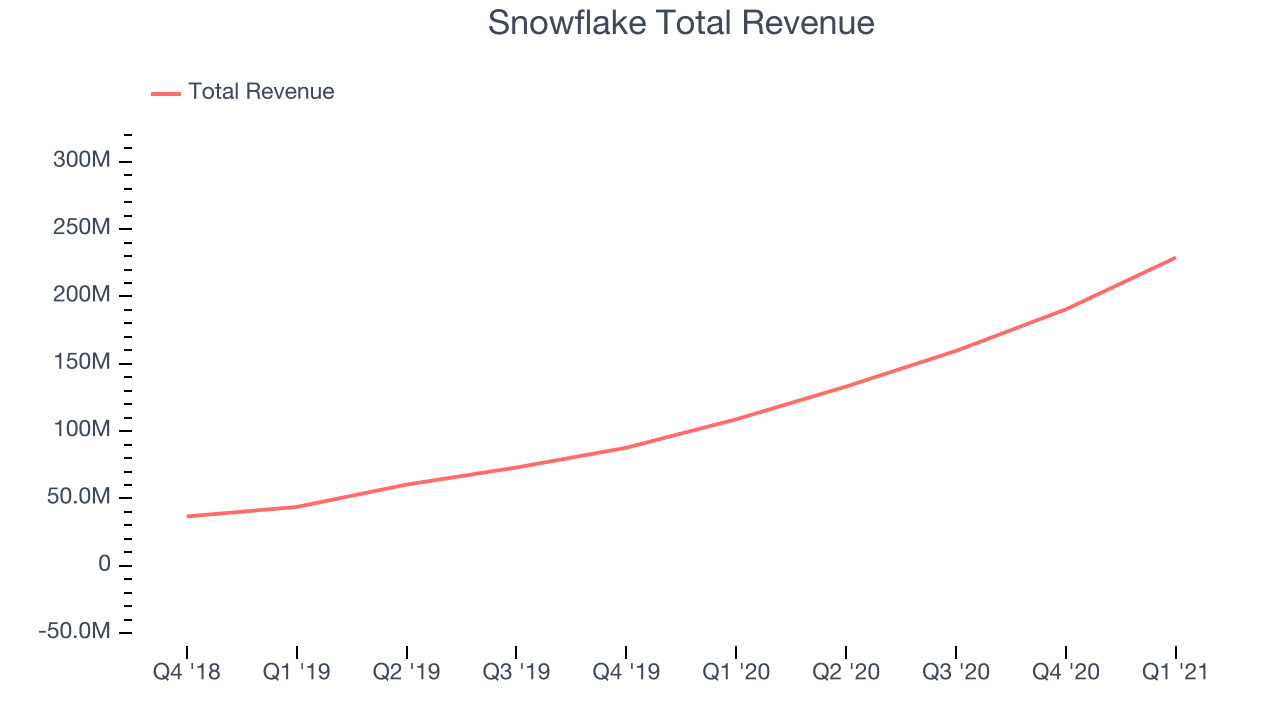

Data warehouse-as-a-service Snowflake (NYSE:SNOW) reported Q1 FY2022 results that beat analyst expectations, with revenue up 110% year on year to $228.9 million. Snowflake made a GAAP loss of $203.2 million, down on its loss of $93.6 million, in the same quarter last year.

What do these results signal for the future of Snowflake? Get early access our full analysis here

Snowflake (NYSE:SNOW) Q1 FY2022 Highlights:

- Revenue: $228.9 million vs analyst estimates of $213.3 million (7.29% beat)

- EPS (GAAP): -$0.70

- Product revenue guidance for Q2 2022 is $237.5 million at the midpoint

- Free cash flow of $12.9 million, up 76.9% from previous quarter

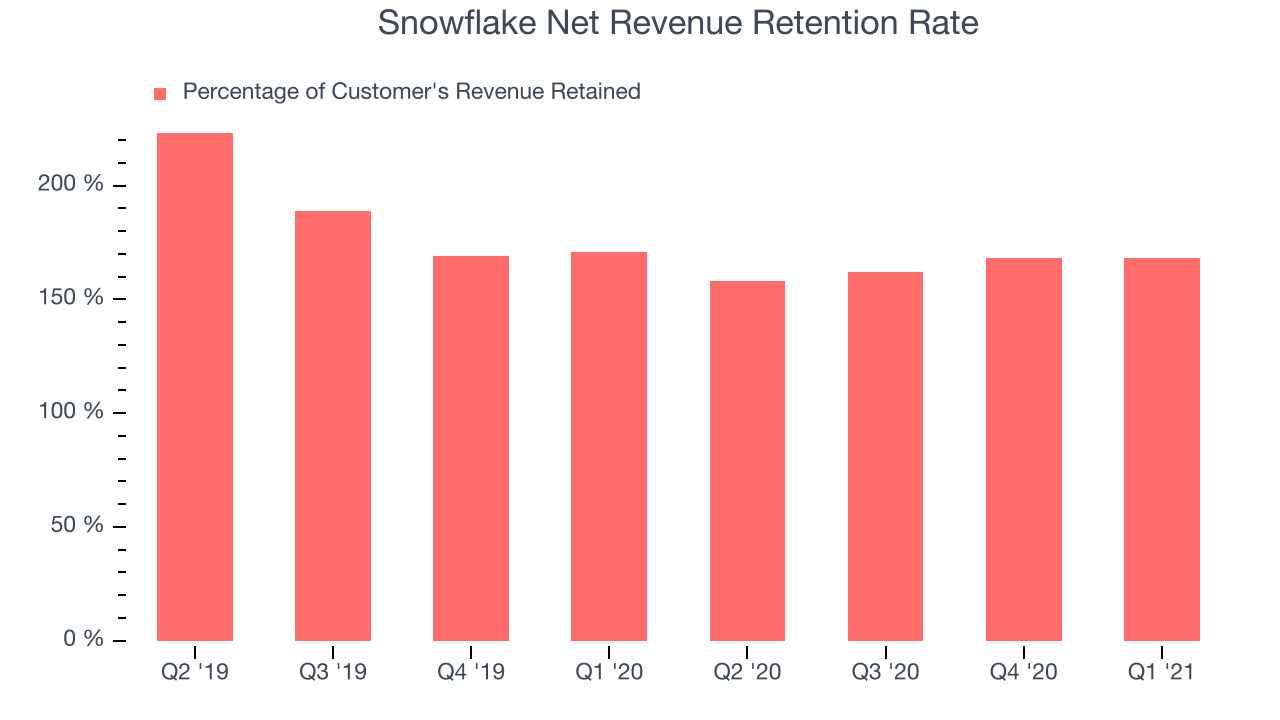

- Net Revenue Retention Rate: 168%, in line with previous quarter

- Customers: 4,532, up from 4,139 in previous quarter

- Gross Margin (GAAP): 57.4%, up from 56.4% previous quarter

- Updated valuation: Snowflake is down at $224.01 and now trades at 96.2x price-to-sales (LTM), compared to 112.8x just before the results.

“Snowflake reported strong Q1 results with triple-digit growth in product revenue, reflecting strength in customer consumption,” said Snowflake CEO Frank Slootman.

A Cheaper Answer To Complex Questions

Founded in 2013 by three French engineers who spent decades working for Oracle, Snowflake (NYSE:SNOW) provides a data warehouse-as-a-service in the cloud that allows companies store large amounts of data and analyze it in real time.

The amount of data generated and collected by companies has exploded and so has the need to analyze it, but it is still often stored in incompatible formats, spread across many different types of storages, and with increasing complexity slow to analyze. Snowflake’s platform separates the storage and analysis and makes it significantly faster, cheaper and easier for their customers to answer their data questions, often replacing number of different systems at once.

As you can see below, Snowflake's revenue growth has been incredible over the last twelve months, growing from $108.8 million to $228.9 million.

This was another standout quarter with the revenue up a splendid 110% year on year. On top of that, revenue increased $38.4 million quarter on quarter, a very strong improvement on the $30.8 million increase in Q4 2021, and a sign of re-acceleration of growth, which is very nice to see indeed.

There are others doing even better. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 90% year on year and is already up more than 400% since the IPO in December. You can find it on our platform for free.

Shared success

One of the best things about software as a service businesses (and a reason why they trade at such high multiples) is that customers tend to spend more with the company over time. Snowflake offers usage based pricing where customers pay separately for storage and for the minutes of computing time it takes to perform the analysis they require.

Snowflake's net revenue retention rate, an important measure of how much customers from a year ago were spending at the end of the quarter, was at 168% in Q1. That means even if they didn't win any new customers, Snowflake would have grown its revenue 68% year on year. Despite it going down over the last year that is still an absolutely exceptional retention rate, meaning Snowflake's software is extremely successful with their customers who are rapidly expanding the use of it across their organizations.

Key Takeaways from Snowflake's Q1 Results

With market capitalisation of $66.3 billion, more than $3.93 billion in cash and the fact it is operating close to free cash flow break-even, we're confident that Snowflake has the resources it needs to pursue a high growth business strategy.

We were impressed by the exceptional revenue growth Snowflake delivered this quarter. And we were also excited to see it that it outperformed Wall St’s revenue expectations. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. While market has a high expectations of Snowflake and it trades at very high multiples, we think it will continue to stand out as a compelling growth stock, arguably even more so than before.

PS. If you found this analysis useful, you will love our earnings alerts! We publish so fast, you often have the opportunity to buy or sell before the market has fully absorbed the information. Never miss out on the right time to invest again. Signup here for free early access.

The author has no position in any of the stocks mentioned.