Data warehouse-as-a-service Snowflake (NYSE:SNOW) reported Q3 FY2023 results topping analyst expectations, with revenue up 66.5% year on year to $557 million. Snowflake made a GAAP loss of $200.9 million, down on its loss of $154.8 million, in the same quarter last year.

Is now the time to buy Snowflake? Access our full analysis of the earnings results here, it's free.

Snowflake (SNOW) Q3 FY2023 Highlights:

- Revenue: $557 million vs analyst estimates of $538.9 million (3.36% beat)

- EPS (non-GAAP): $0.11 vs analyst estimates of $0.05 ($0.06 beat)

- Product revenue guidance for Q4 2023 is $537.5 million at the midpoint

- Free cash flow of $64.9 million, up 20.6% from previous quarter

- Net Revenue Retention Rate: 165%, down from 171% previous quarter

- Customers: 7,292, up from 6,808 in previous quarter

- Gross Margin (GAAP): 65.7%, up from 63.8% same quarter last year

Founded in 2013 by three French engineers who spent decades working for Oracle, Snowflake (NYSE:SNOW) provides a data warehouse-as-a-service in the cloud that allows companies to store large amounts of data and analyze it in real time.

Data is the lifeblood of the internet and software in general, and the amount of data created is growing at an accelerating pace. Likewise, the importance of storing the data in scalable and efficient formats continues to rise, especially as the diversity of the data and associated use cases expand from analyzing simple, structured data to high-scale processing of unstructured data, images, audio and video.

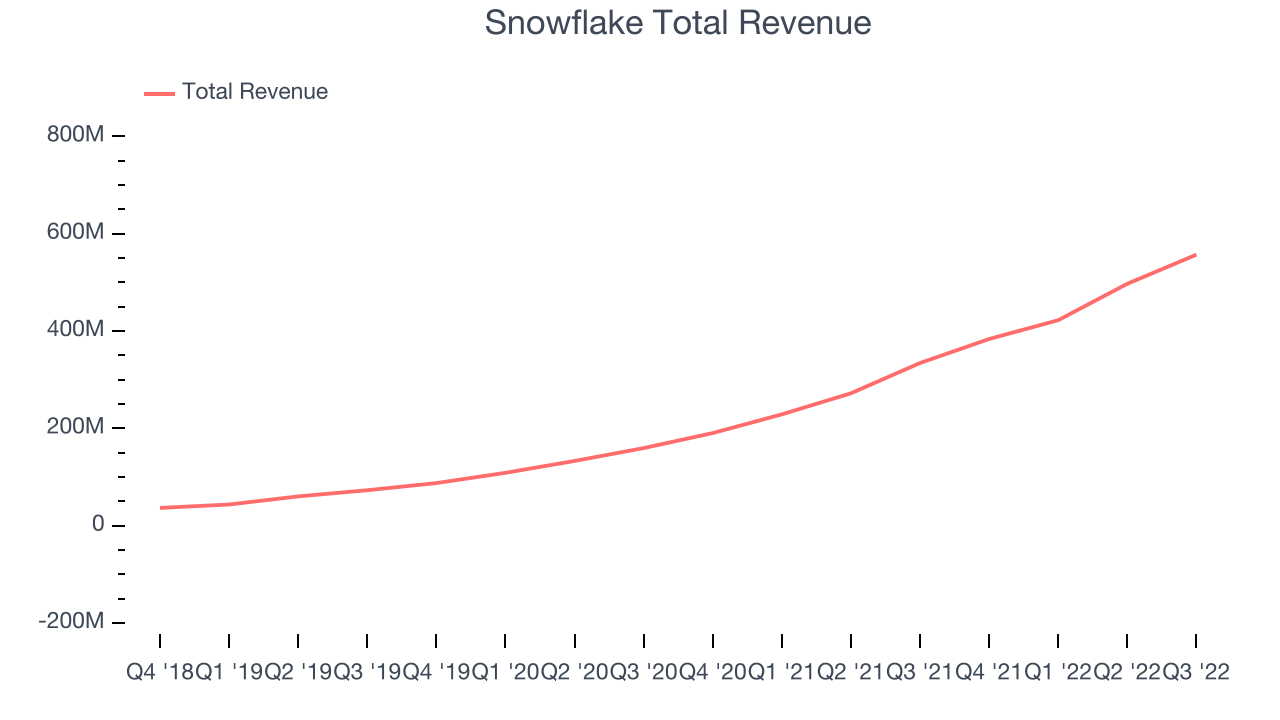

Sales Growth

As you can see below, Snowflake's revenue growth has been incredible over the last two years, growing from quarterly revenue of $159.6 million in Q3 FY2021, to $557 million.

And while we saw even higher rates of growth previously, the revenue growth was still very strong; up a rather splendid 66.5% year on year. But the growth did slow down compared to last quarter, as the revenue increased by just $59.7 million in Q3, compared to $74.8 million in Q2 2023. We'd like to see revenue increase by a greater amount each quarter, but a one-off fluctuation is usually not concerning.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 48.9% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

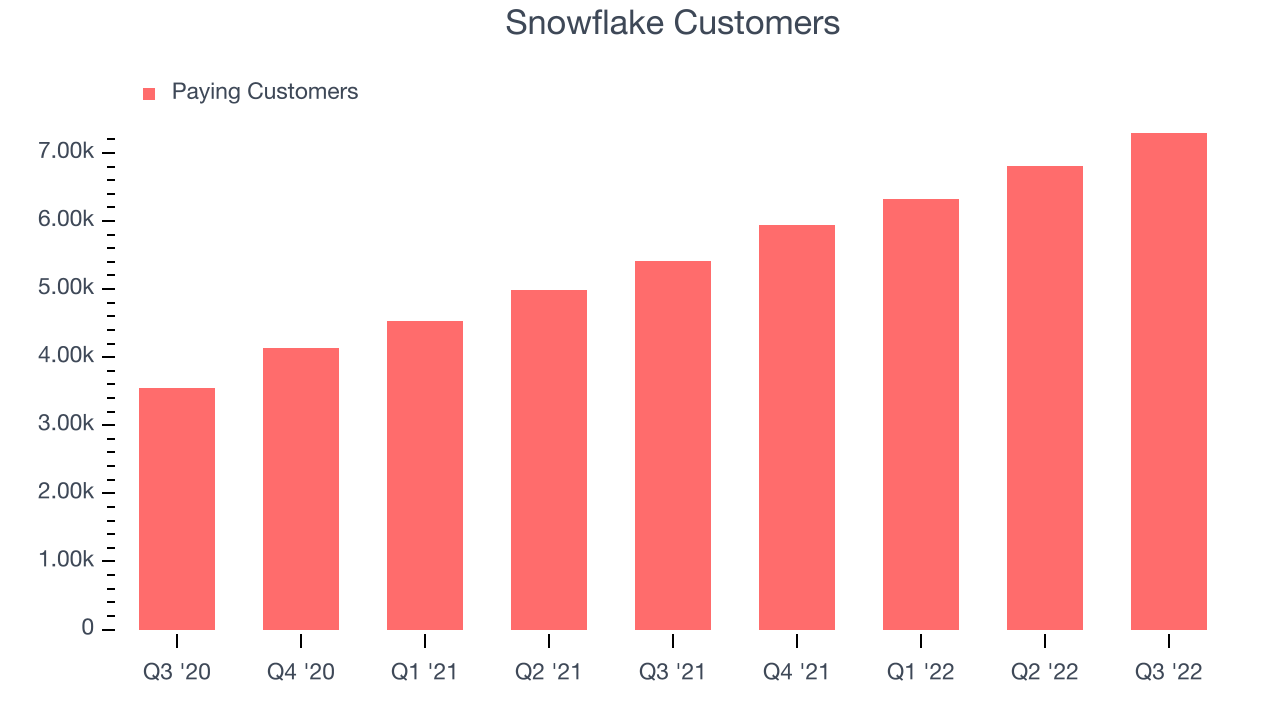

Customer Growth

You can see below that Snowflake reported 7,292 customers at the end of the quarter, an increase of 484 on last quarter. That's in line with the customer growth we have seen over the last couple of quarters, suggesting that the company can maintain its current sales momentum.

Key Takeaways from Snowflake's Q3 Results

Sporting a market capitalization of $43.6 billion, more than $3.94 billion in cash and with positive free cash flow over the last twelve months, we're confident that Snowflake has the resources it needs to pursue a high growth business strategy.

We were impressed by strong free cash flow Snowflake delivered this quarter. And we were also excited to see that it outperformed analysts' revenue expectations. On the other hand, it was less good to see the deterioration in revenue retention rate. Zooming out, we think this was still a decent, albeit mixed, quarter, showing the company is staying on target. But the market was likely expecting more and the company is down 11.9% on the results and currently trades at $125.79 per share.

Should you invest in Snowflake right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.