Data warehouse-as-a-service Snowflake (NYSE:SNOW) beat analysts' expectations in Q4 FY2024, with revenue up 31.5% year on year to $774.7 million. It made a non-GAAP profit of $0.35 per share, improving from its profit of $0.13 per share in the same quarter last year.

Is now the time to buy Snowflake? Find out by accessing our full research report, it's free.

Snowflake (SNOW) Q4 FY2024 Highlights:

- Revenue: $774.7 million vs analyst estimates of $759.6 million (2% beat)

- EPS (non-GAAP): $0.35 vs analyst estimates of $0.18 ($0.17 beat)

- Product Revenue Guidance for Q1 2025 is $747.5 million at the midpoint (vs analysts' estimates of $770.1 million)

- Free Cash Flow of $324.5 million, up from $102.3 million in the previous quarter

- Net Revenue Retention Rate: 131%, down from 135% in the previous quarter

- Gross Margin (GAAP): 68.8%, up from 65.1% in the same quarter last year

- Market Capitalization: $77.07 billion

- CEO Frank Slootman is retiring

“Snowflake finished fiscal 2024 with a 38% year-over-year product revenue growth, totaling $2.67 billion. Non-GAAP adjusted free cash flow was $810 million, representing 56% year-over-year growth,” said Frank Slootman, Chairman of the Board, Snowflake.

Founded in 2013 by three French engineers who spent decades working for Oracle, Snowflake (NYSE:SNOW) provides a data warehouse-as-a-service in the cloud that allows companies to store large amounts of data and analyze it in real time.

Data Storage

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

Sales Growth

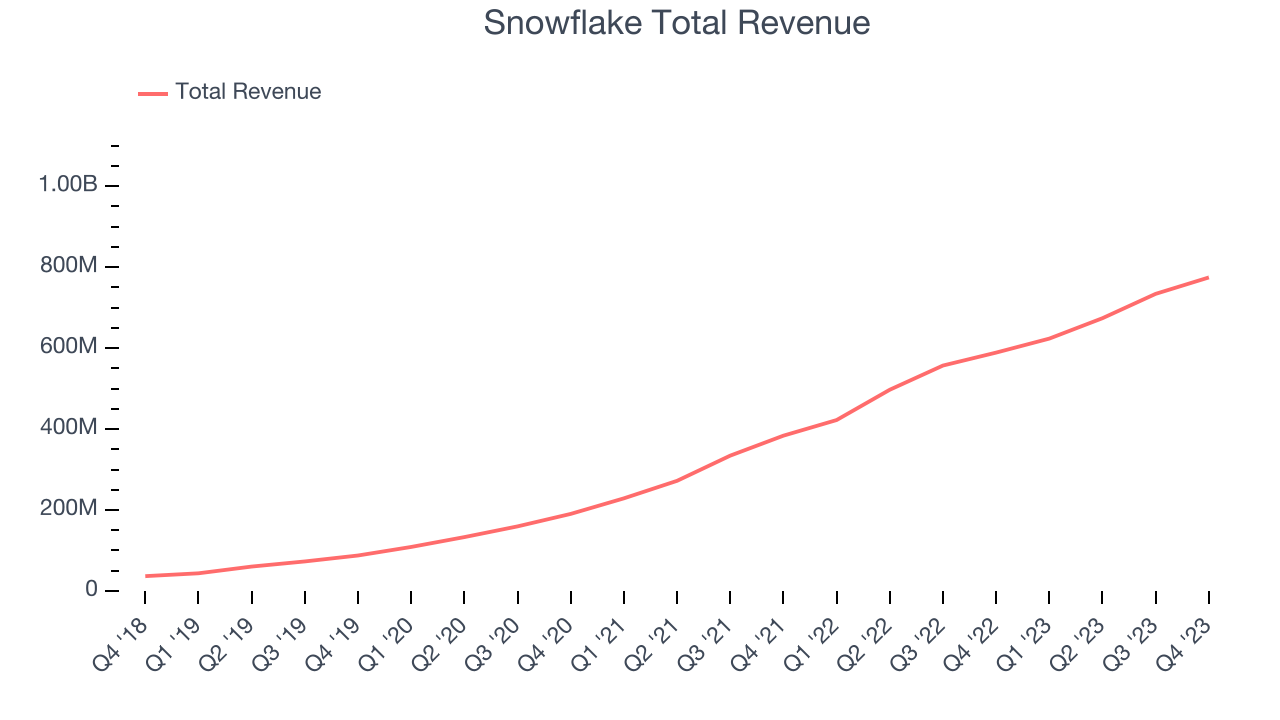

As you can see below, Snowflake's revenue growth has been exceptional over the last two years, growing from $383.8 million in Q4 FY2022 to $774.7 million this quarter.

Unsurprisingly, this was another great quarter for Snowflake with revenue up 31.5% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $40.53 million in Q4 compared to $60.16 million in Q3 2024. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Product revenue guidance for Q1 2025 came in at $747.5 million at the midpoint, missing analyst estimates.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

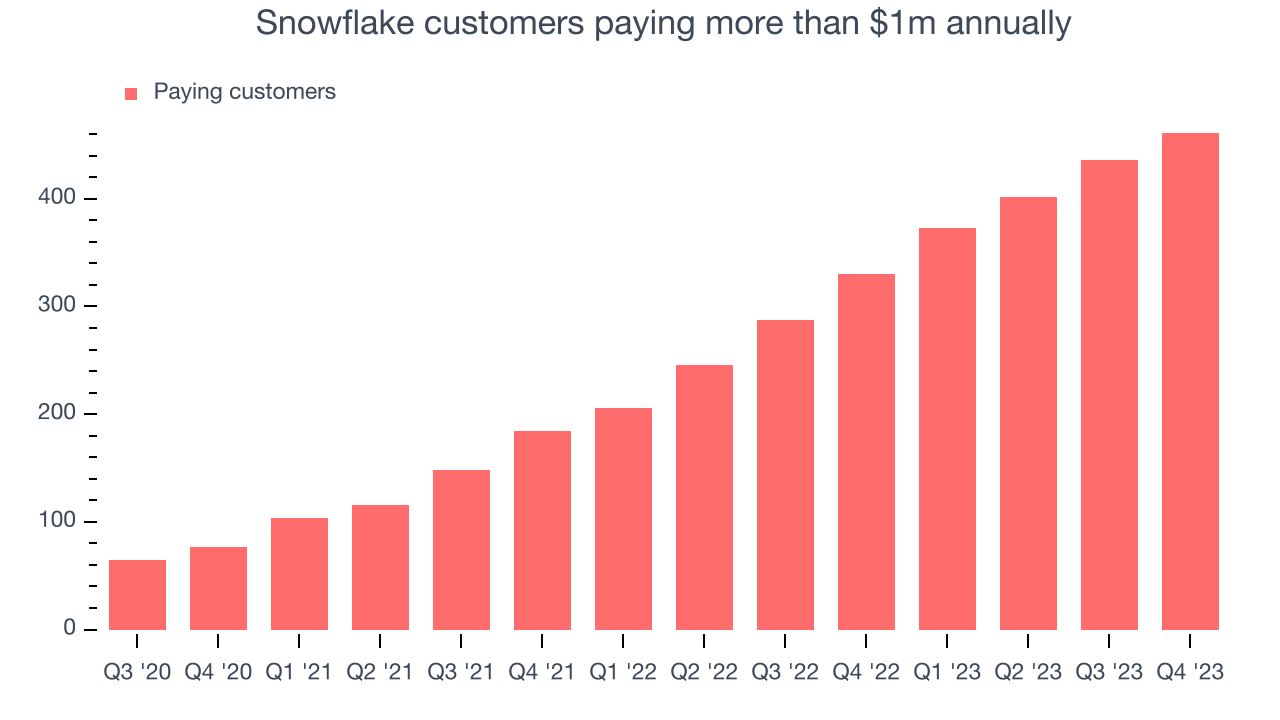

Large Customers Growth

This quarter, Snowflake reported 461 enterprise customers paying more than $1m annually, an increase of 25 from the previous quarter. That's a bit fewer contract wins than last quarter and quite a bit below what we've typically observed over the past four quarters, suggesting that its sales momentum with large customers is slowing.

Key Takeaways from Snowflake's Q4 Results

Snowflake delivered strong free cash flow, while still growing revenue at 30%+, which is certainly an impressive feat. On the other hand, its net revenue retention declined again and product guidance for Q1 missed analysts' estimates. Overall, this quarter's results seemed mixed. The market reacted negatively to the news of CEO Frank Slootman retirin and the stock is down 22.2% after reporting, trading at $178.9 per share.

So should you invest in Snowflake right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.