Spectrum Brands (NYSE:SPB) Exceeds Q1 Expectations

Anthony Lee /

May 9, 2024

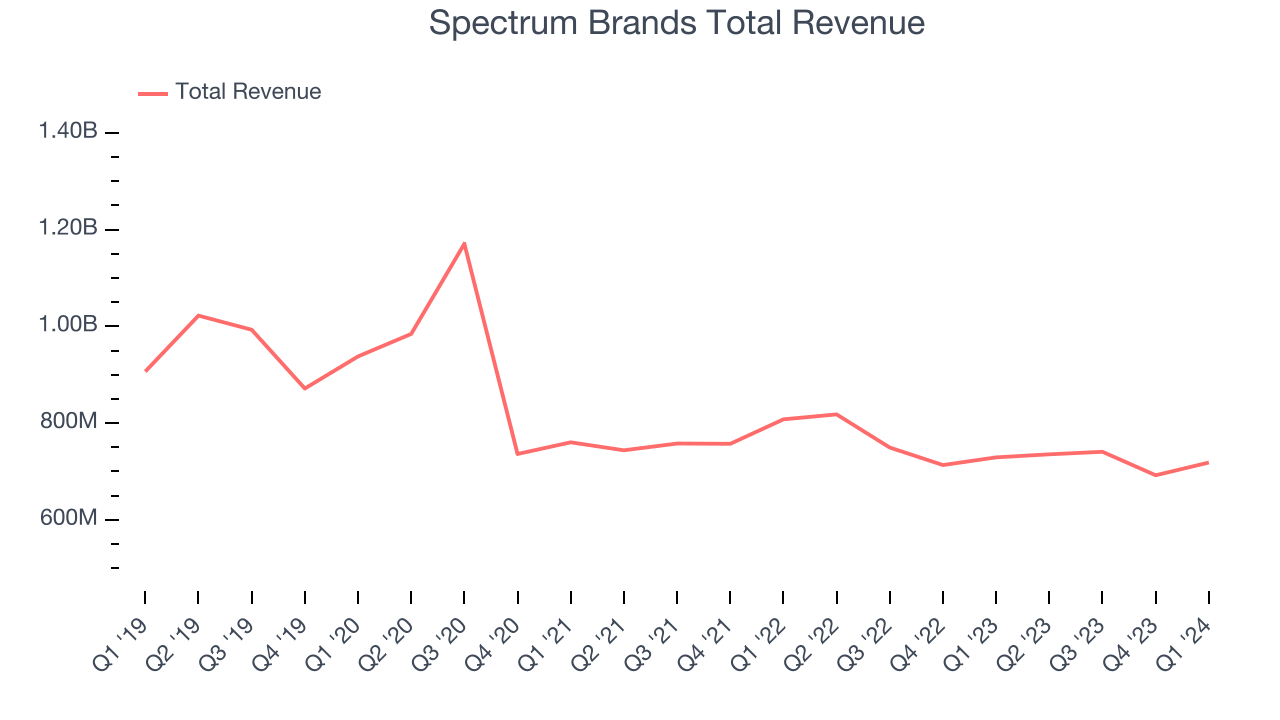

Household products company Spectrum Brands (NYSE:SPB) reported results ahead of analysts' expectations in Q1 CY2024, with revenue down 1.5% year on year to $718.5 million. It made a non-GAAP profit of $1.62 per share, improving from its loss of $0.14 per share in the same quarter last year.

Is now the time to buy Spectrum Brands? Find out in our full research report.

Spectrum Brands (SPB) Q1 CY2024 Highlights:

- Revenue: $718.5 million vs analyst estimates of $708.6 million (1.4% beat)

- Adjusted EBITDA: $62.3 million vs analyst estimates of $60.0 million (3.8% beat)

- Guidance for full year revenue now flat compared to 2023 (previously expected a decline)

- Gross Margin (GAAP): 38.1%, up from 29.5% in the same quarter last year

- Free Cash Flow was -$9 million compared to -$12.7 million in the previous quarter

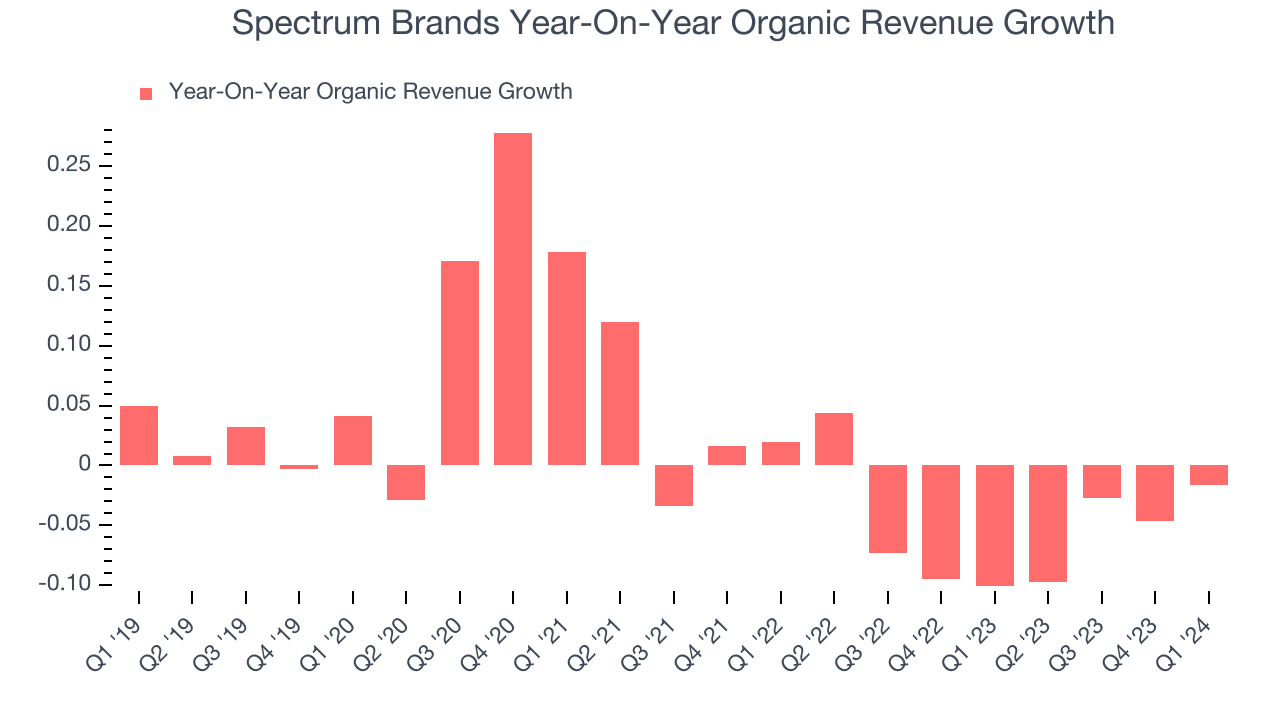

- Organic Revenue was down 1.6% year on year

- Market Capitalization: $2.56 billion

“We are pleased to report a strong second quarter of fiscal 24, building off the operating momentum we drove in our first quarter. Our sales performance improved sequentially and our operations produced a gross margin of 38.1%, an 870 basis point improvement over last year. Our net income increased $124.9 million and our Adjusted EBITDA, excluding investment income, more than doubled to $95.3 million. Net income margins increased to 6.9% and Adjusted EBITDA margins, excluding investment income, nearly doubled to 13.3%. Given our first half performance, and expectations for modest top-line growth in the second half of the year, we are raising our full year Earnings Framework and now expect net sales to be relatively flat and Adjusted EBITDA to grow in the low double-digits,“ said David Maura, Chairman and Chief Executive Officer of Spectrum Brands.

A leader in multiple consumer product categories, Spectrum Brands (NYSE:SPB) is a diversified company with a portfolio of trusted brands spanning home appliances, garden care, personal care, and pet care.

Household Products

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

Sales Growth

Spectrum Brands carries some recognizable brands and products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Spectrum Brands can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue has declined over the last three years, dropping 7.5% annually. This is among the worst in the consumer staples industry, where demand is typically stable.

This quarter, Spectrum Brands's revenue fell 1.5% year on year to $718.5 million but beat Wall Street's estimates by 1.4%. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business's performance excluding the impacts of foreign currency fluctuations and one-time events such as mergers, acquisitions, and divestitures.

Spectrum Brands's demand has been falling over the last eight quarters, and on average, its organic sales have declined by 5.1% year on year.

In the latest quarter, Spectrum Brands's organic sales fell 1.6% year on year. This decrease was an improvement from the 10.1% year-on-year decline it posted 12 months ago. It's always great to see a business improve its prospects.

Key Takeaways from Spectrum Brands's Q1 Results

We liked seeing Spectrum Brands beat analysts' adjusted EBITDA expectations this quarter. We were also excited its gross margin outperformed Wall Street's estimates. Lastly, the company raised its full year revenue outlook, now expecting it to be flat vs. 2023 compared to a prior expectation of a sales decline. Zooming out, we think this was a solid quarter. The stock is flat after reporting and currently trades at $84.52 per share.

Spectrum Brands may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.