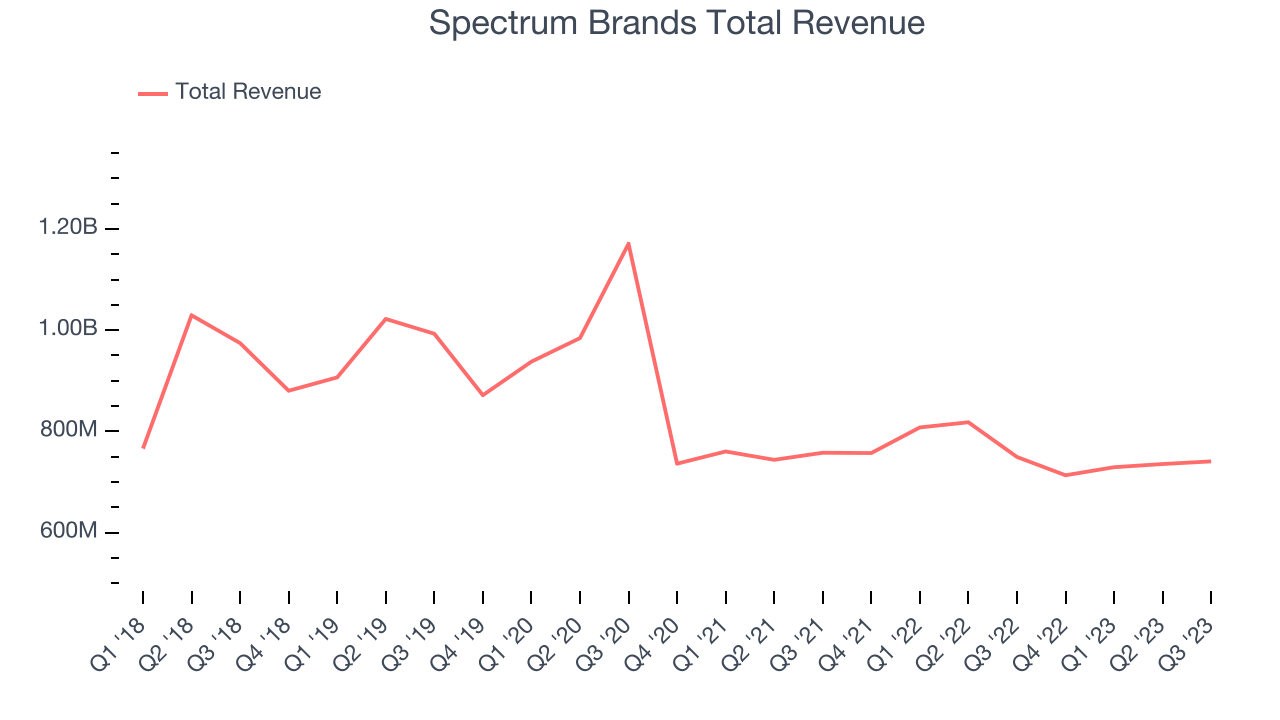

Household products company Spectrum Brands (NYSE:SPB) reported results in line with analysts' expectations in Q4 FY2023, with revenue down 1.2% year on year to $740.7 million. Turning to EPS, Spectrum Brands made a non-GAAP profit of $1.36 per share, improving from its profit of $0.48 per share in the same quarter last year.

Is now the time to buy Spectrum Brands? Find out by accessing our full research report, it's free.

Spectrum Brands (SPB) Q4 FY2023 Highlights:

- Revenue: $740.7 million vs analyst estimates of $739.7 million (small beat)

- Adjusted EBITDA: $113.7 million vs. analyst estimates of $86.4 million (big beat)

- EPS (non-GAAP): $1.36 vs analyst estimates of $0.99 (36.9% beat)

- Fiscal 2024 guidance: revenue (low single-digit percentage decline) below but Adjusted EBITDA (high single-digit percentage increase) ahead

- Free Cash Flow was -$528 million compared to -$91.7 million in the previous quarter

- Gross Margin (GAAP): 33%, up from 31.9% in the same quarter last year

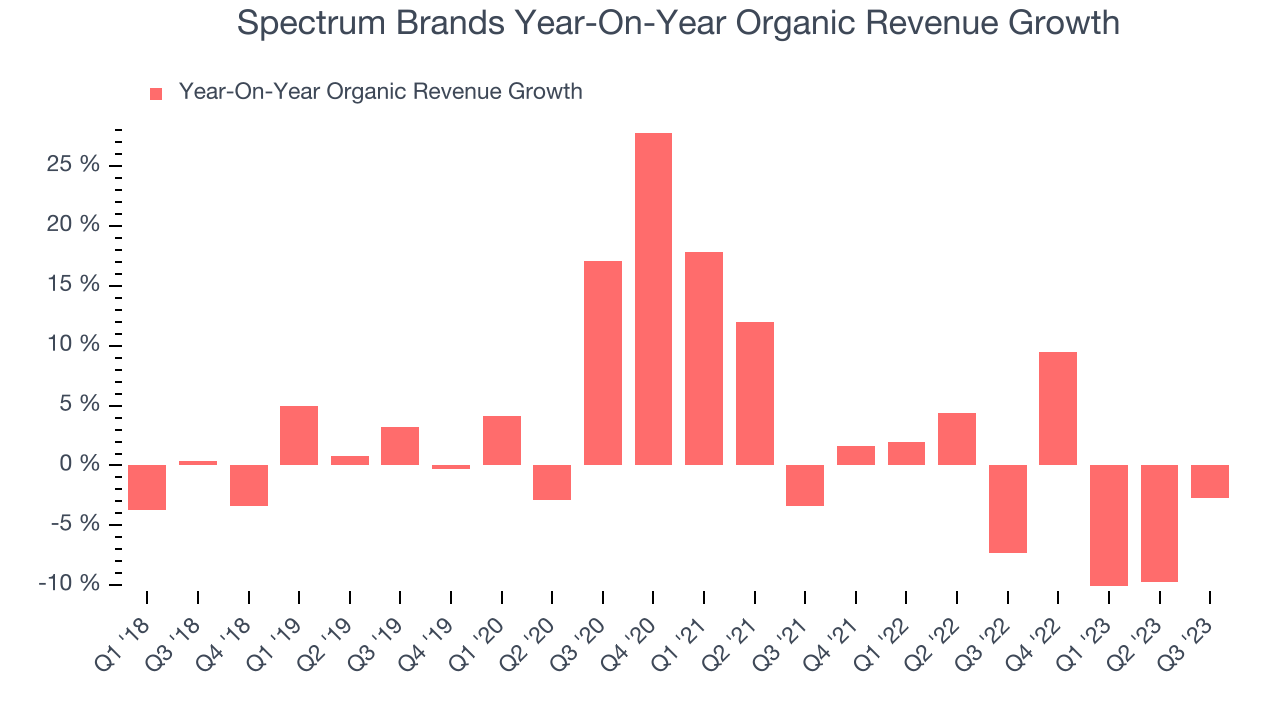

- Organic Revenue was down 2.7% year on year

“We have concluded a pivotal year for the business as we close out our fourth quarter. We have already paid down $1.6 billion of our outstanding debt with the proceeds from the sale of our HHI business and have ended the year in a net cash position. We have reduced our inventory by over $300 million since the beginning of the year while improving fill rates across all businesses. We have also improved our margin structure by driving cost improvements and exiting non-core unproductive categories. With the latest financial results for the quarter, we have started to transition our business from defending against the various headwinds and preserving cash to leaning into the opportunities that a strong balance sheet and improved margins present to us,” said David Maura, Chairman and Chief Executive Officer of Spectrum Brands.

A leader in multiple consumer product categories, Spectrum Brands (NYSE:SPB) is a diversified company with a portfolio of trusted brands spanning home appliances, garden care, personal care, and pet care.

Household Products

Household products companies engage in the manufacturing, distribution, and sale of goods that maintain and enhance the home environment. This includes cleaning supplies, home improvement tools, kitchenware, small appliances, and home decor items. Companies within this sector must focus on product quality, innovation, and cost efficiency to remain competitive. Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options.

Sales Growth

Spectrum Brands is larger than most consumer staples companies and benefits from economies of scale, giving it an edge over its smaller competitors.

As you can see below, the company's revenue has declined over the last three years, dropping 9.7% annually. This is among the worst in the consumer staples industry, where demand is typically stable.

This quarter, Spectrum Brands reported a rather uninspiring 1.2% year-on-year revenue decline, in line with Wall Street's estimates. Looking ahead, analysts expect sales to grow 1.2% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business's performance excluding the impacts of foreign currency fluctuations and one-time events such as mergers, acquisitions, and divestitures.

Spectrum Brands's demand has been falling over the last eight quarters, and on average, its organic sales have declined by 1.5% year on year.

In the latest quarter, Spectrum Brands's organic sales fell 2.7% year on year. This decrease was an improvement from the 7.3% year-on-year decline it posted 12 months ago. It's always great to see a business improve its prospects.

Key Takeaways from Spectrum Brands's Q4 Results

Although Spectrum Brands, which has a market capitalization of $2.74 billion, has been burning cash over the last 12 months, its more than $1.86 billion in cash on hand gives it the flexibility to continue prioritizing growth over profitability.

We were impressed by how significantly Spectrum Brands blew past analysts' Adjusted EBITDA and EPS expectations this quarter. That stood out as a positive in these results. The company's fiscal 2024 outlook was mixed, with revenue missing but Adjusted EBITDA guided above. Overall, this was a solid quarter for Spectrum Brands. The stock is flat after reporting and currently trades at $76.9 per share.

Spectrum Brands may have had a decent quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.