Website and ecommerce tools provider Squarespace (NYSE:SQSP) reported Q3 FY2023 results topping analysts' expectations, with revenue up 18.1% year on year to $257.1 million. Guidance for next quarter's revenue was also optimistic at $262.5 million at the midpoint, 2.3% above analysts' estimates. Turning to EPS, Squarespace made a GAAP loss of $0.12 per share, down from its profit of $0.07 per share in the same quarter last year.

Is now the time to buy Squarespace? Find out by accessing our full research report, it's free.

Squarespace (SQSP) Q3 FY2023 Highlights:

- Revenue: $257.1 million vs analyst estimates of $251.9 million (2% beat)

- EPS: -$0.12 vs analyst estimates of $0.12 ($0.24 miss)

- Revenue Guidance for Q4 2023 is $262.5 million at the midpoint, above analyst estimates of $256.5 million

- Free Cash Flow of $47.4 million, similar to the previous quarter

- Gross Margin (GAAP): 79.9%, down from 82.1% in the same quarter last year

"We are on track to exceed $1 billion in total revenue by the end of 2023, a significant milestone for Squarespace as we continue to expand our offerings and footprint globally," said Anthony Casalena, Founder & CEO of Squarespace.

Founded in New York City in 2003, Squarespace (NYSE:SQSP) is a platform for small businesses and creators to build their digital presences online.

E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

Sales Growth

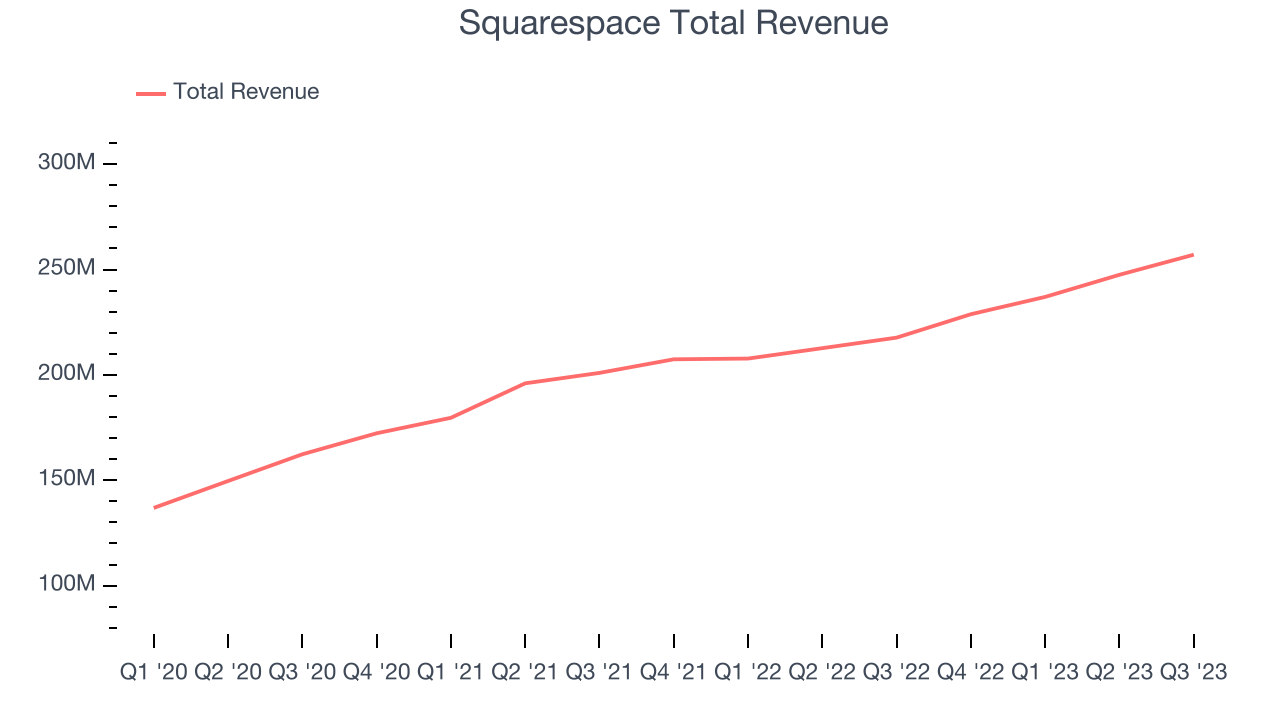

As you can see below, Squarespace's revenue growth has been mediocre over the last two years, growing from $201 million in Q3 FY2021 to $257.1 million this quarter.

This quarter, Squarespace's quarterly revenue was once again up 18.1% year on year. Looking at the last two quarters, we can see that Squarespace's revenue increased by $9.5 million in Q3 while it grew $10.5 million in Q2 2023. This steady quarter-on-quarter growth shows that the company can more or less maintain its growth trajectory.

Next quarter's guidance suggests that Squarespace is expecting revenue to grow 14.7% year on year to $262.5 million, improving on the 10.3% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.9% over the next 12 months before the earnings results announcement.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Key Takeaways from Squarespace's Q3 Results

With a market capitalization of $4.1 billion, Squarespace is among smaller companies, but its $257.1 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

It was good to see Squarespace's strong revenue guidance for next quarter, which topped analysts' expectations. We were also glad to see solid free cash flow. On the other hand, its gross margin declined. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is flat after reporting and currently trades at $30.09 per share.

So should you invest in Squarespace right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.