Website and ecommerce tools provider Squarespace (NYSE:SQSP) reported Q4 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 18.3% year on year to $270.7 million. Guidance for next quarter's revenue was also better than expected at $275.5 million at the midpoint, 1.2% above analysts' estimates. It made a GAAP profit of $0.04 per share, down from its profit of $0.14 per share in the same quarter last year.

Squarespace (SQSP) Q4 FY2023 Highlights:

- Revenue: $270.7 million vs analyst estimates of $263.2 million (2.9% beat)

- EPS: $0.04 vs analyst estimates of $0.13 (-$0.09 miss)

- Revenue Guidance for Q1 2024 is $275.5 million at the midpoint, above analyst estimates of $272.3 million

- Management's revenue guidance for the upcoming financial year 2024 is $1.18 billion at the midpoint, beating analyst estimates by 1.3% and implying 16.6% growth (vs 16.7% in FY2023)

- Free Cash Flow of $57.23 million, up 20.9% from the previous quarter

- Gross Margin (GAAP): 74.3%, down from 82.5% in the same quarter last year

- Market Capitalization: $4.59 billion

Founded in New York City in 2003, Squarespace (NYSE:SQSP) is a platform for small businesses and creators to build their digital presences online.

Today, only slightly more than half of US small and midsize businesses have an online presence, and for many that do, they are outdated and lack modern functionality. It has long been difficult and expensive for small businesses or entrepreneurs to build and manage websites and online stores, let alone manage online marketing activities.

With Squarespace, entrepreneurs and small businesses can create a website or online store quickly with little to no technical skill for less than a few hundred dollars per year. Although there are many website builders and e-commerce platforms in the market, Squarespace has differentiated itself in two key ways. The first is a heavy focus on design, its website templates are generally more curated and polished than its rivals. Second, by creating an all-in-one platform that has functionality ranging from basic websites to more complex ecommerce sites, Squarespace can facilitate many different types of online businesses: product, services, content, and subscription. Over time, Squarespace has been growing out the range of its commerce capabilities through integrations with other vendors like Quickbooks (for tax management) and with acquisitions like Tock, which added the ability to book reservations for restaurant and hospitality businesses.

E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

Squarespace’s main competitors are Wix (NASDAQ: WIX), GoDaddy (NYSE: GDDY), and Shopify (NYSE:SHOP).

Sales Growth

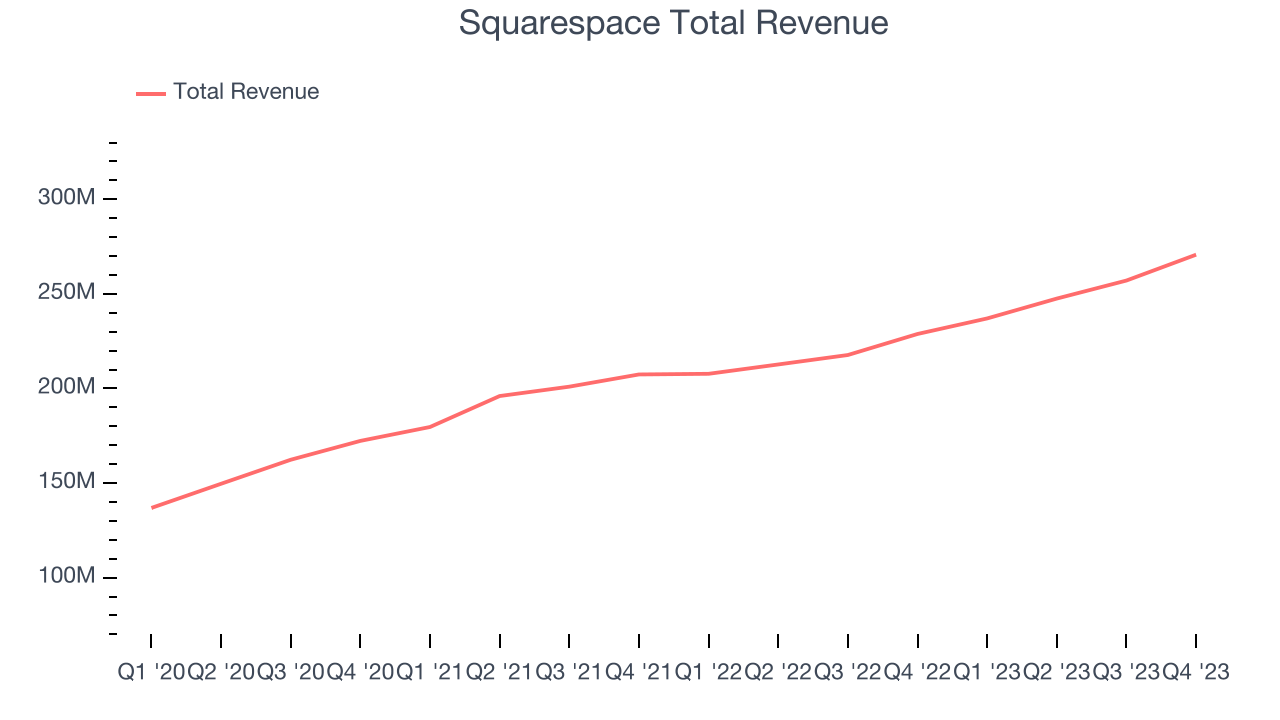

As you can see below, Squarespace's revenue growth has been mediocre over the last two years, growing from $207.4 million in Q4 FY2021 to $270.7 million this quarter.

This quarter, Squarespace's quarterly revenue was once again up 18.3% year on year. We can see that Squarespace's revenue increased by $13.66 million quarter on quarter, which is a solid improvement from the $9.53 million increase in Q3 2023. Shareholders should applaud the acceleration of growth.

Next quarter's guidance suggests that Squarespace is expecting revenue to grow 16.2% year on year to $275.5 million, improving on the 14.1% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $1.18 billion at the midpoint, growing 16.6% year on year compared to the 16.8% increase in FY2023.

Profitability

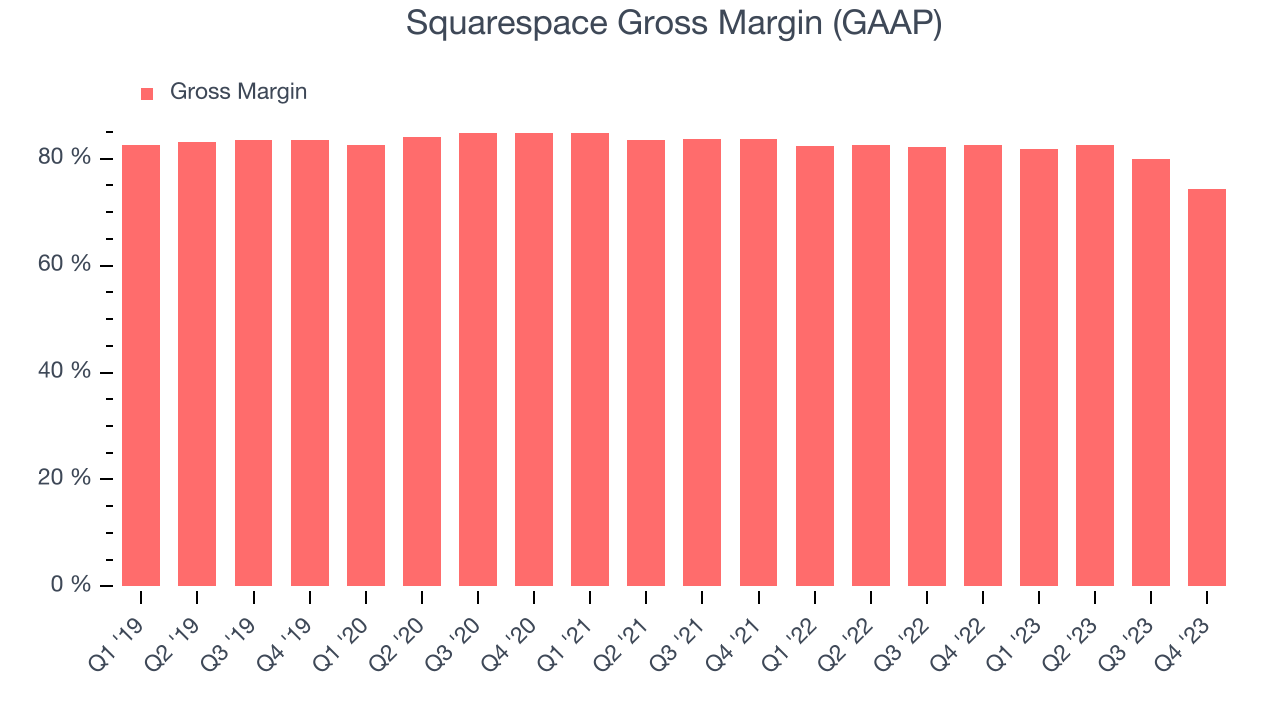

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Squarespace's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 74.3% in Q4.

That means that for every $1 in revenue the company had $0.74 left to spend on developing new products, sales and marketing, and general administrative overhead. Despite its decline over the last year, Squarespace's gross margin is still around the average of a typical SaaS businesses. Gross margin has a major impact on a company’s ability to develop new products and invest in marketing, which may ultimately determine the winner in a competitive market. This makes it a critical metric to track for the long-term investor.

Cash Is King

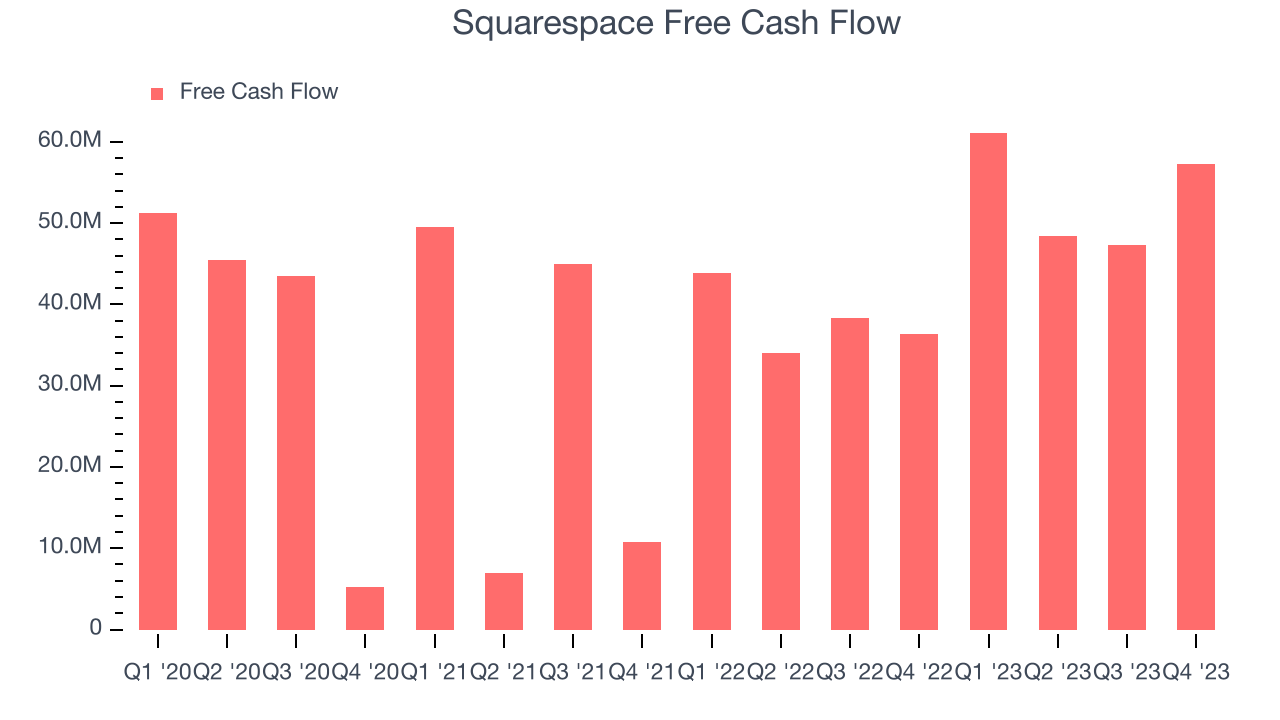

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Squarespace's free cash flow came in at $57.23 million in Q4, up 57.2% year on year.

Squarespace has generated $214.1 million in free cash flow over the last 12 months, an impressive 21.2% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from Squarespace's Q4 Results

Revenue beat, which is always encouraging. However, profitability missed, leading to EPS below expectations. We were glad that next quarter and the full year's revenue guidance was strong and above Wall Street estimates. Overall, this quarter's results seemed fairly positive, with good guidance as a key bright spot. The stock is flat after reporting and currently trades at $33.6 per share.

Is Now The Time?

When considering an investment in Squarespace, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Squarespace is a good business. Although its with analysts expecting growth to slow from here, its impressive gross margins indicate excellent business economics.

Squarespace's price-to-sales ratio based on the next 12 months is 4.1x, suggesting that the market is expecting more moderate growth, relative to the hottest tech stocks. There are definitely things to like about Squarespace and there's no doubt it's a bit of a market darling, at least for some. But when considering the company against the backdrop of the software landscape, it seems there's a lot of optimism already priced in. We wonder whether there might be better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $35.18 per share right before these results (compared to the current share price of $33.60).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.