Data and analytics software provider Teradata (NYSE:TDC) reported results in line with analyst expectations in Q1 FY2023 quarter, with revenue down 4.03% year on year to $476 million. Teradata made a GAAP profit of $40 million, improving on its profit of $36 million, in the same quarter last year.

Is now the time to buy Teradata? Access our full analysis of the earnings results here, it's free.

Teradata (TDC) Q1 FY2023 Highlights:

- Revenue: $476 million vs analyst estimates of $473 million (small beat)

- EPS (non-GAAP): $0.61 vs analyst expectations of $0.61 (small miss)

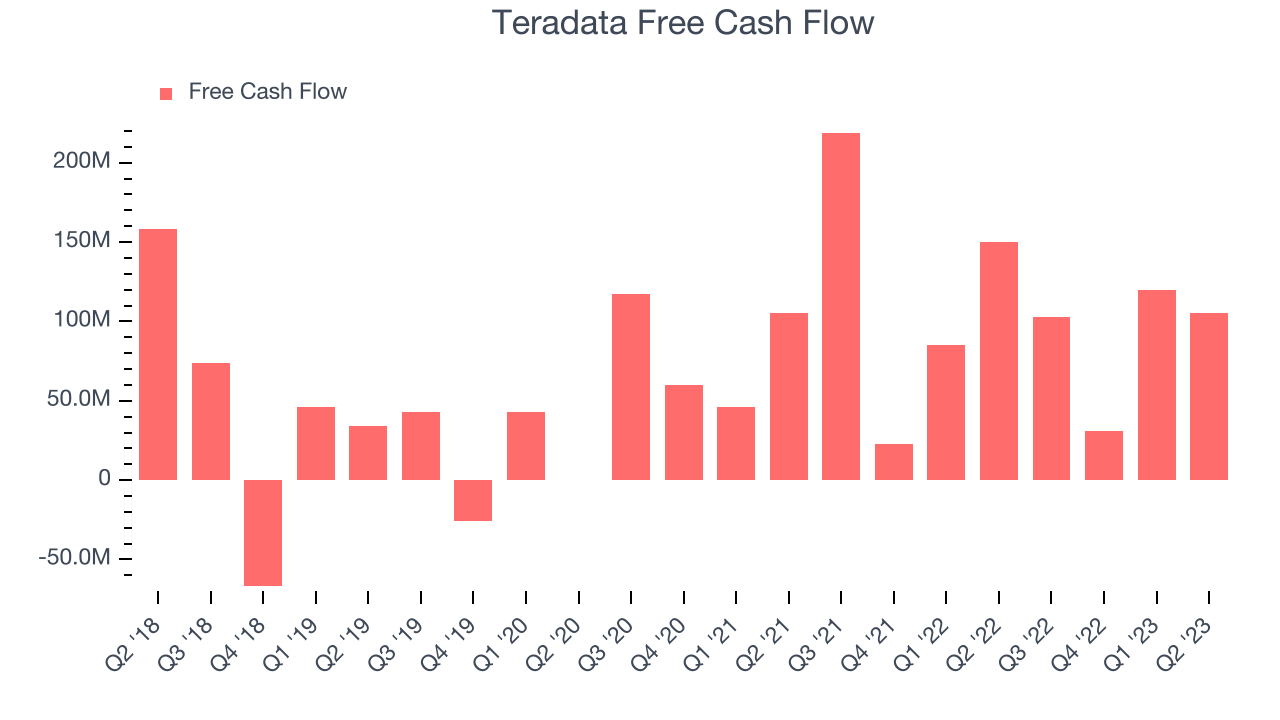

- Free cash flow of $105 million, down 12.5% from previous quarter

“Teradata is off to a strong start in 2023 with sequential growth in total ARR, and we closed one of the largest deals in Teradata’s history…tangible proof points of our cloud-first strategy in action,” said Steve McMillan, President and CEO, Teradata.

Part of point-of-sale and ATM company NCR from 1991 to 2007, Teradata (NYSE:TDC) offers a software-as-service platform that helps organizations manage their data across multiple storages and analyze it.

Generating insights from system level data is an increasing priority for most businesses, but to do so requires connecting and analyzing piles of data stored and siloed in separate databases. This is the demand driver for cloud based data infrastructure software providers, who can more readily integrate, distribute and process information vs. legacy on-premise software providers.

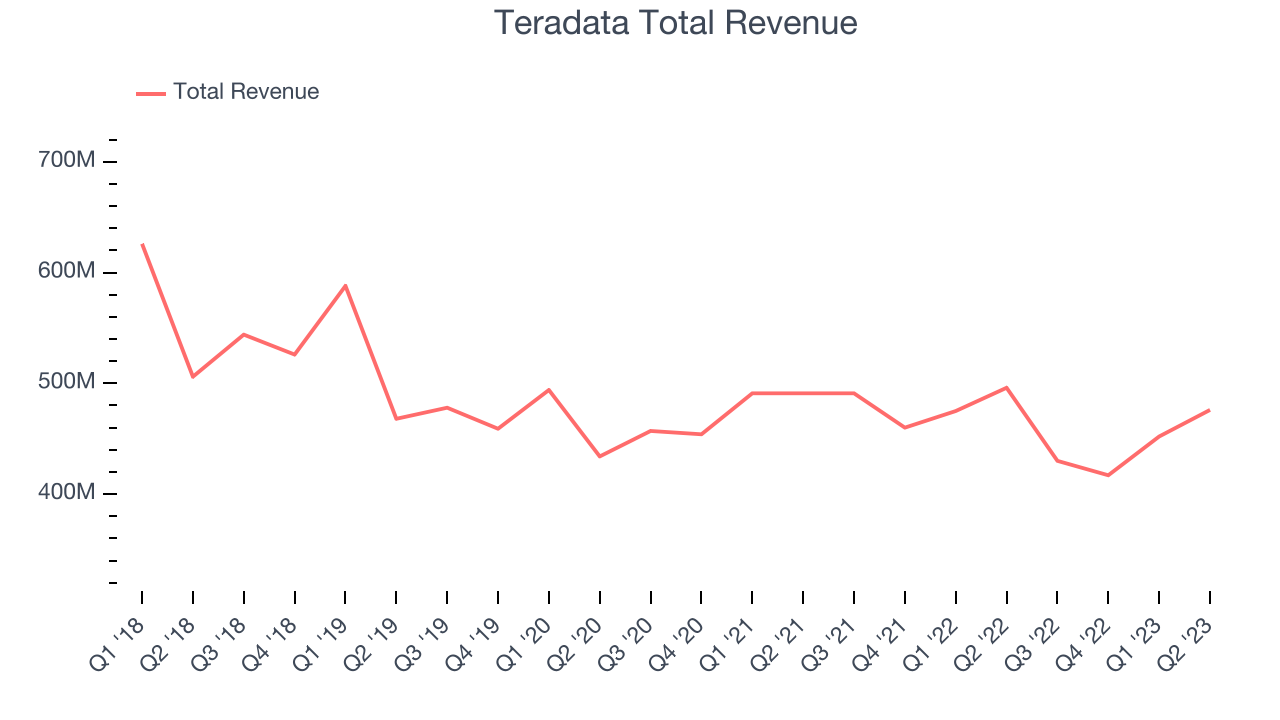

Sales Growth

As you can see below, Teradata's revenue has been declining over the last two years, shrinking from quarterly revenue of $491 million in Q1 FY2021, to $476 million.

Teradata's quarterly revenue was down again 4.03% year on year. Ahead of the earnings results the analysts covering the company were estimating sales to grow 3.48% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Cash Is King

If you have followed StockStory for a while, you know that we put an emphasis on cash flow. Why, you ask? We believe that in the end cash is king, as you can't use accounting profits to pay the bills. Teradata's free cash flow came in at $105 million in Q1, down 30% year on year.

Teradata has generated $359 million in free cash flow over the last twelve months, an impressive 20.2% of revenues. This extremely high FCF margin is a result of Teradata asset lite business model and strong competitive positioning, and provides it the option to return capital to shareholders while still having plenty of cash to invest in the business.

Key Takeaways from Teradata's Q1 Results

With a market capitalization of $4.16 billion Teradata is among smaller companies, but its more than $551 million in cash and positive free cash flow over the last twelve months put it in a very strong position to invest in growth.

Zooming out, we think this was an ok quarter for Teradata, showing the company is staying on target. The company is flat on the results and currently trades at $41.14 per share.

Should you invest in Teradata right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.