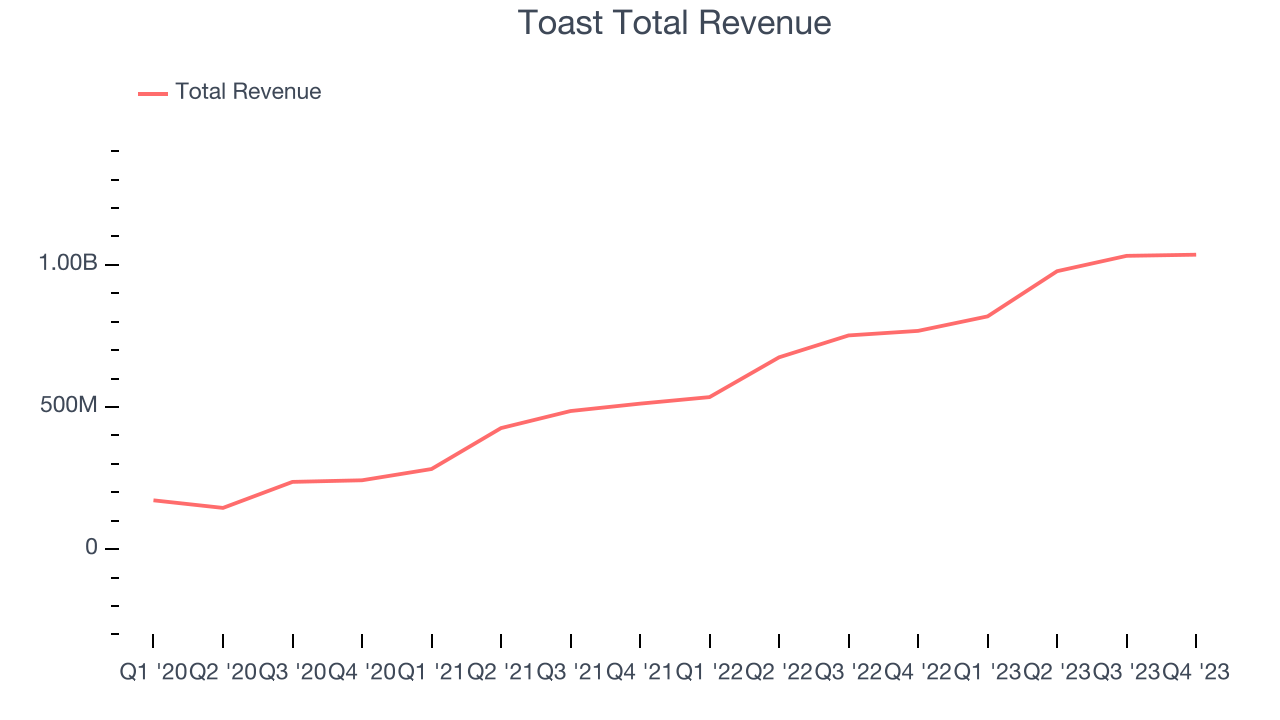

Restaurant software platform Toast (NYSE:TOST) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 34.7% year on year to $1.04 billion. It made a GAAP loss of $0.07 per share, down from its loss of $0.04 per share in the same quarter last year.

Toast (TOST) Q4 FY2023 Highlights:

- Revenue: $1.04 billion vs analyst estimates of $1.02 billion (1.9% beat)

- EPS: -$0.07 vs analyst estimates of -$0.11 (35.8% beat)

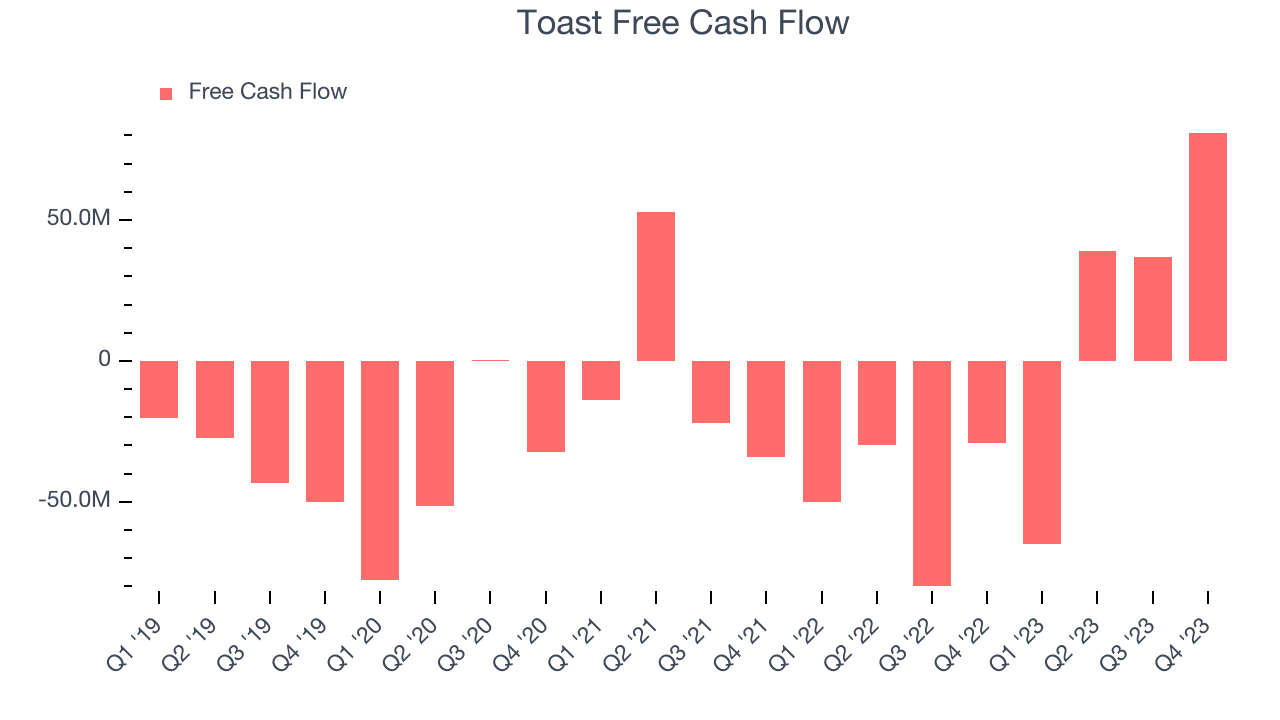

- Free Cash Flow of $81 million, up 119% from the previous quarter

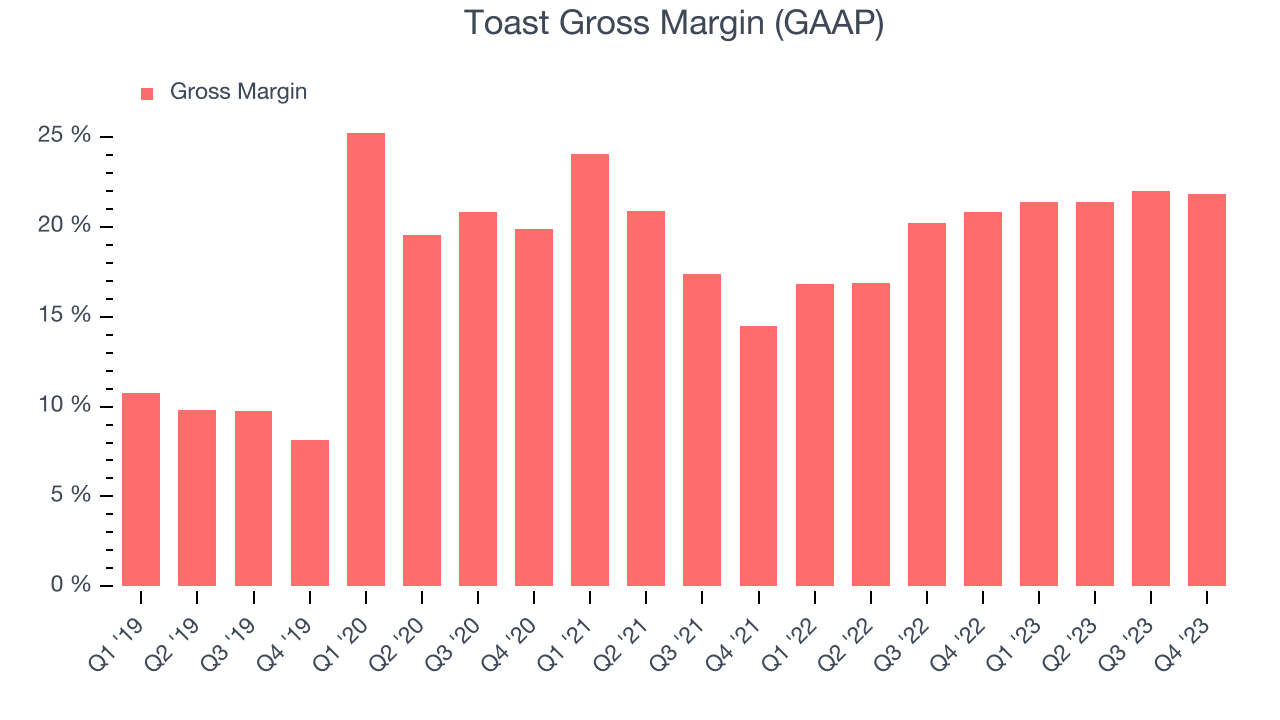

- Gross Margin (GAAP): 21.8%, up from 20.8% in the same quarter last year

- Market Capitalization: $10.89 billion

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE:TOST) provides integrated point-of-sale (POS) hardware, software, and payments solutions for restaurants.

Many restaurants still rely on manual processes or antiquated one off technology solutions to manage operations, which results in a myriad of operational inefficiencies. Today’s restaurants must juggle online ordering, delivery, takeout, and curbside pickup orders, and are expected to communicate timing for order completion to both customers and employees. Layer on demand managing menu changes, incorporating marketing and loyalty programs, and keeping track of employee payroll and tracking supplies, and the need for a modern vertical specific software operating system targeted at restaurants becomes clear.

Toast is a cloud-based, end-to-end software and payments platform that is built specifically for restaurants. The company offers a range of functionality that includes the ability to accept and process payments, manage kitchen display systems, along with payroll and labor. It also has a marketing component that allows restaurants to build loyalty programs and email marketing, and even has Toast Capital, which provides working capital through small business loans. In 2021 prior to its IPO, Toast acquired xtraCHEF, which added functionality for supply chain management, such as accounts payable automation and inventory management. The Toast platform also has a range of integrations with third parties like DoorDash for delivery or Staples for supplies.

The value proposition for restaurants is to generate a virtuous cycle between restaurants, their employees, customers, and suppliers. Happy customers increase sales and tips, improving employee morale, and so forth. Additionally, the end-to-end nature of the operating system allows restaurants analytics and insights that leads to better decisions and improved restaurant performance.

Hospitality & Restaurant Software

Enterprise resource planning (ERP) and customer relationship management (CRM) are two of the largest software categories dominated by the likes of Microsoft, Oracle, and Salesforce.com. Today, the secular trend of mass customization is driving vertical software that customizes ERP and CRM functions for specific industry requirements. Restaurants are a prime example where a set of customized software providers have sprung up in recent years to create unique operating systems that blend tax and accounting software, order management and delivery, along with supply chain management. Hotels and other hospitality providers are another example.

Toast’s main competitors are a mix of legacy restaurant systems like Oracle’s Micros (NYSE:ORCL), Par Technology Corp (NYSE:PAR), and NCR (NYSE:NCR) along with newer general purpose POS technologies readily configurable to restaurants such as Square (NASDAQ: SQ), Shopify (NYSE:SHOP), along with Olo (NYSE:OLO) and a host of mostly private pure play rivals.

Sales Growth

As you can see below, Toast's revenue growth has been exceptional over the last two years, growing from $512 million in Q4 FY2021 to $1.04 billion this quarter.

Unsurprisingly, this was another great quarter for Toast with revenue up 34.7% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $4 million in Q4 compared to $54 million in Q3 2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Toast's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 21.8% in Q4.

That means that for every $1 in revenue the company had $0.22 left to spend on developing new products, sales and marketing, and general administrative overhead. Toast's gross margin is poor for a SaaS business and we'd like to see it start improving.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Toast's free cash flow came in at $81 million in Q4, turning positive over the last year.

Toast has burned through $92 million of cash over the last 12 months, resulting in a negative 2.4% free cash flow margin. This low FCF margin stems from Toast's poor unit economics or a constant need to reinvest in its business to stay competitive.

Key Takeaways from Toast's Q4 Results

It was encouraging to see Toast narrowly top analysts' revenue expectations this quarter. We also found the continuing momentum in free cash flow promising. Zooming out, we think this was a decent quarter, showing that the company is staying on target. The stock is up 11.8% after reporting and currently trades at $21.5 per share.

Is Now The Time?

When considering an investment in Toast, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Toast is a solid business. We'd expect growth rates to moderate from here, but its .

Toast's price-to-sales ratio based on the next 12 months is 2.1x, suggesting that the market is expecting more steady growth, relative to the hottest tech stocks. There are definitely things to like about Toast and there's no doubt it's a bit of a market darling, at least for some. But when considering the company against the backdrop of the software landscape, it seems there's a lot of optimism already priced in. We wonder whether there might be better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $19.76 per share right before these results (compared to the current share price of $21.50).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.