Meat company Tyson Foods (NYSE:TSN) reported revenue ahead of Wall Street’s expectations in Q3 CY2024, with sales up 1.6% year on year to $13.57 billion. Its non-GAAP profit of $0.92 per share was also 33.6% above analysts’ consensus estimates.

Is now the time to buy Tyson Foods? Find out by accessing our full research report, it’s free.

Tyson Foods (TSN) Q3 CY2024 Highlights:

- Revenue: $13.57 billion vs analyst estimates of $13.43 billion (1% beat)

- Adjusted EPS: $0.92 vs analyst estimates of $0.69 (33.6% beat)

- EBITDA: $843 million vs analyst estimates of $763.4 million (10.4% beat)

- Initiated 2025 guidance calling for $2.0 billion of operating profit (2% beat)

- Gross Margin (GAAP): 7.8%, up from 3.1% in the same quarter last year

- Operating Margin: 3.9%, up from -3.5% in the same quarter last year

- EBITDA Margin: 6.2%, up from 4.7% in the same quarter last year

- Free Cash Flow was $369 million, up from -$52 million in the same quarter last year

- Sales Volumes were flat year on year (-0.6% in the same quarter last year)

- Market Capitalization: $20.93 billion

"We delivered significant improvement in profitability for the fourth quarter and full year. We also strengthened our financial position, with solid cash flow generation and a substantial reduction of our net leverage ratio," stated Donnie King, President & CEO of Tyson Foods.

Company Overview

Started as a simple trucking business, Tyson Foods (NYSE:TSN) today is one of the world’s largest producers of chicken, beef, and pork.

Perishable Food

The perishable food industry is diverse, encompassing large-scale producers and distributors to specialty and artisanal brands. These companies sell produce, dairy products, meats, and baked goods and have become integral to serving modern American consumers who prioritize freshness, quality, and nutritional value. Investing in perishable food stocks presents both opportunities and challenges. While the perishable nature of products can introduce risks related to supply chain management and shelf life, it also creates a constant demand driven by the necessity for fresh food. Companies that can efficiently manage inventory, distribution, and quality control are well-positioned to thrive in this competitive market. Navigating the perishable food industry requires adherence to strict food safety standards, regulations, and labeling requirements.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years.

Tyson Foods is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it's harder to find incremental growth when you've already penetrated the market.

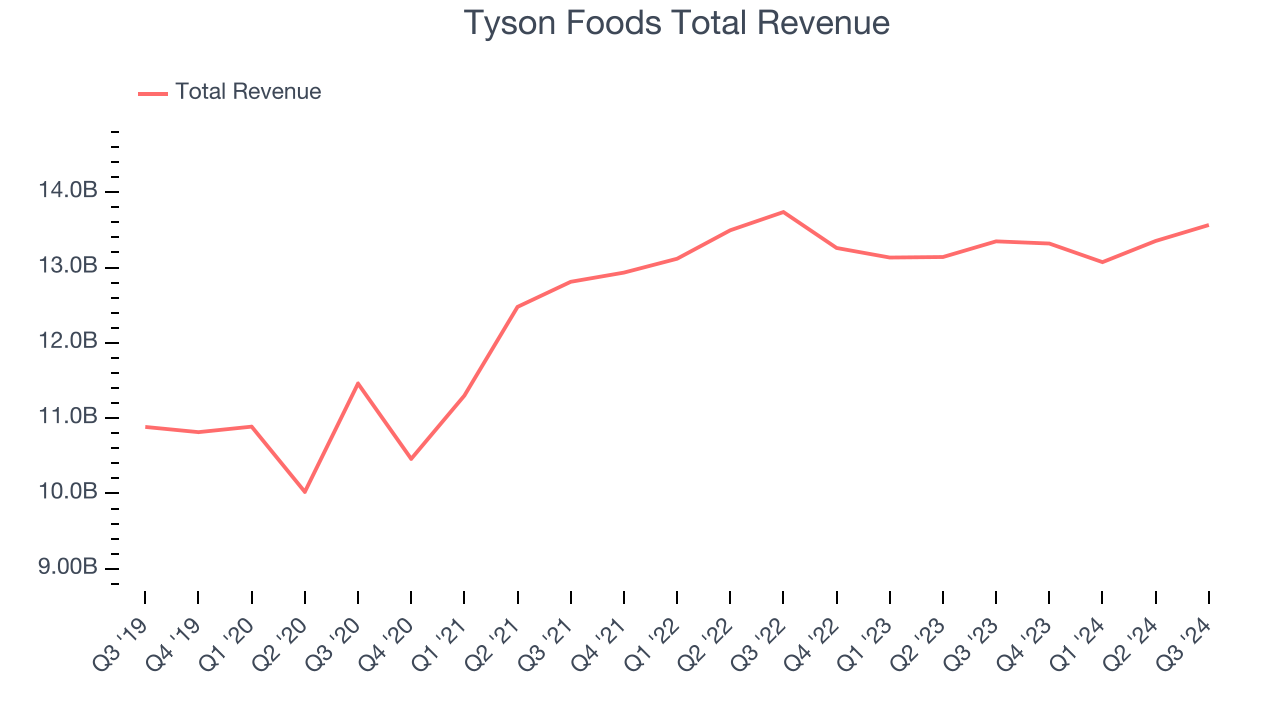

As you can see below, Tyson Foods’s 4.3% annualized revenue growth over the last three years was tepid, but to its credit, consumers bought more of its products.

This quarter, Tyson Foods reported modest year-on-year revenue growth of 1.6% but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 1.2% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and suggests its products will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Volume Growth

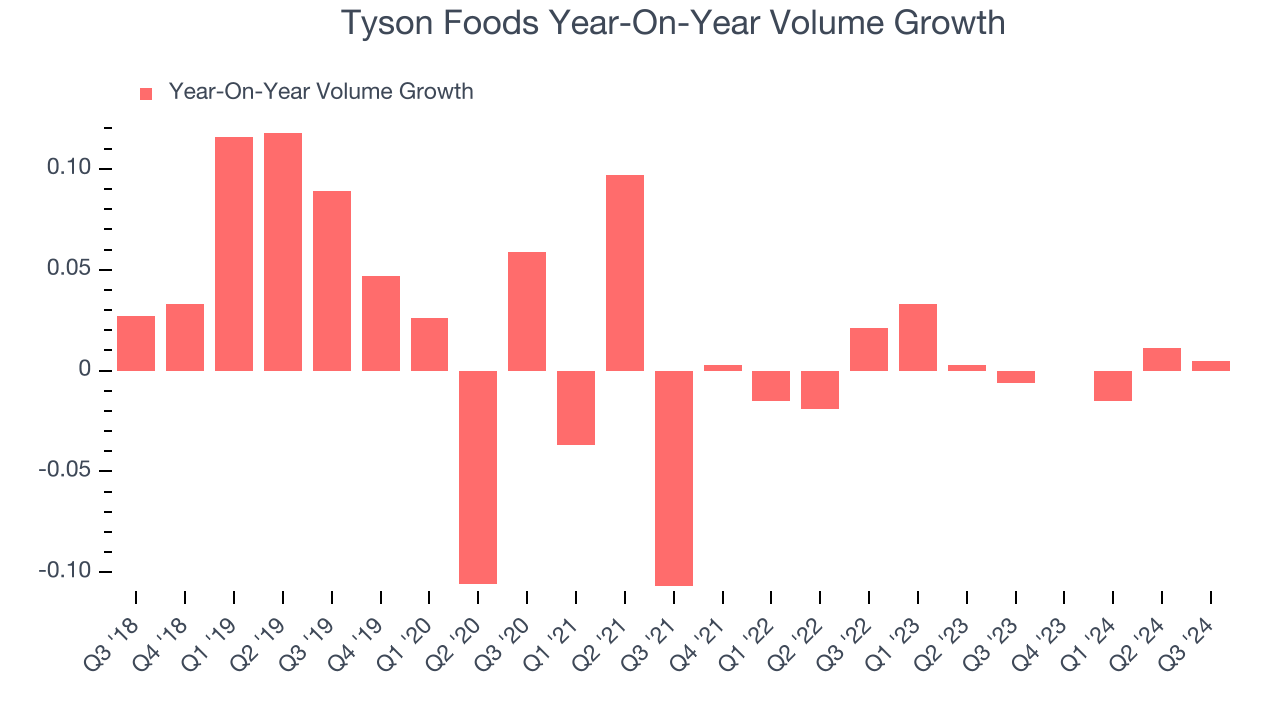

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Tyson Foods’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

In Tyson Foods’s Q3 2024, year on year sales volumes were flat. This result was more or less in line with the same quarter last year.

Key Takeaways from Tyson Foods’s Q3 Results

We were impressed by how significantly Tyson Foods blew past analysts’ gross margin and EBITDA expectations this quarter. We were also excited its operating profit guidance for 2025 outperformed Wall Street’s estimates. Zooming out, we think this was a solid quarter. The stock traded up 6.3% to $62.54 immediately after reporting.

Tyson Foods may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.