Athletic apparel company Under Armour (NYSE:UAA) will be announcing earnings results tomorrow morning. Here's what to look for.

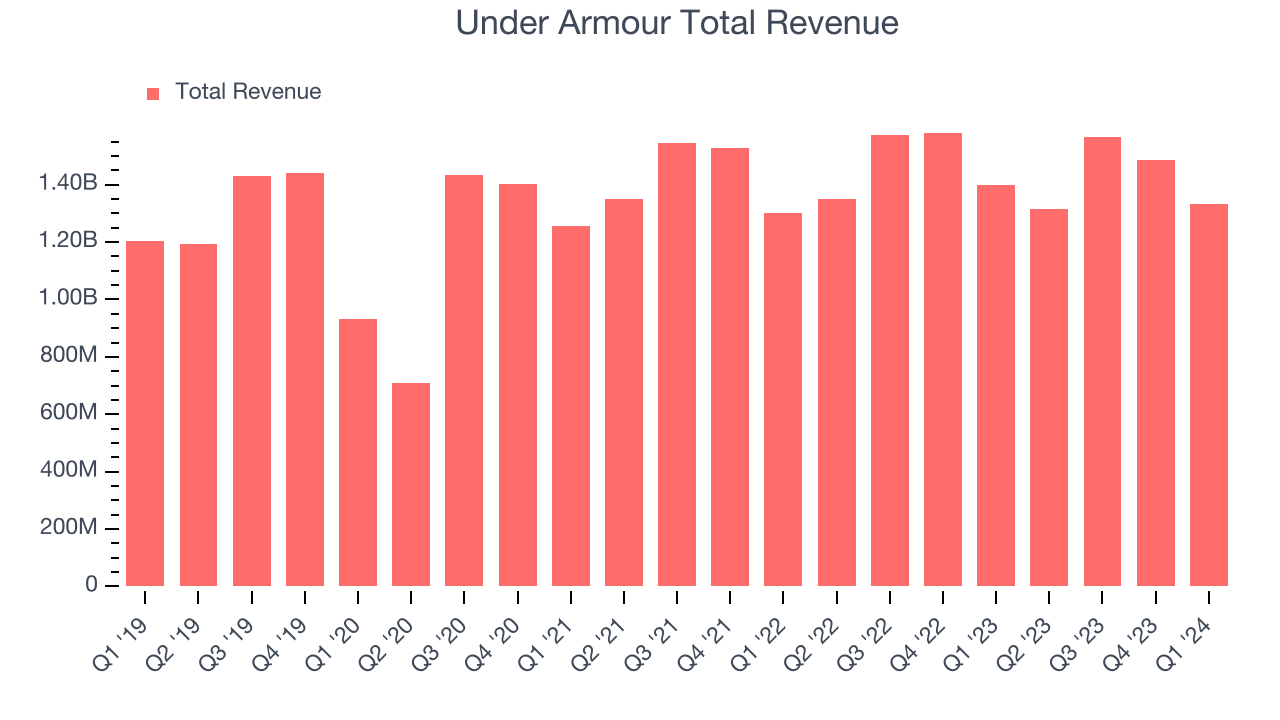

Under Armour met analysts' revenue expectations last quarter, reporting revenues of $1.33 billion, down 4.7% year on year. It was a slower quarter for the company, with underwhelming earnings guidance for the full year and a miss of analysts' constant currency revenue estimates.

Is Under Armour a buy or sell going into earnings? Read our full analysis here, it's free.

This quarter, analysts are expecting Under Armour's revenue to decline 13.4% year on year to $1.14 billion, a further deceleration from the 2.4% decrease it recorded in the same quarter last year. Adjusted loss is expected to come in at -$0.08 per share.

Heading into earnings, analysts covering the company have grown increasingly bearish with revenue estimates seeing 1 downward revisions over the last 30 days. Under Armour has only missed Wall Street's revenue estimates once over the last two years, exceeding top-line expectations by 1% on average.

Looking at Under Armour's peers in the apparel, accessories and luxury goods segment, some have already reported their Q2 results, giving us a hint as to what we can expect. Kontoor Brands's revenues decreased 1.5% year on year, beating analysts' expectations by 2.3%, and Levi's reported revenues up 7.8%, in line with consensus estimates. Kontoor Brands traded down 1.6% following the results while Levi's was also down 15.7%.

Read our full analysis of Kontoor Brands's results here and Levi's results here.

Investors in the apparel, accessories and luxury goods segment have had steady hands going into earnings, with share prices up 1.5% on average over the last month. Under Armour is down 5.1% during the same time and is heading into earnings with an average analyst price target of $14 (compared to the current share price of $6.45).

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.