Athletic apparel company Under Armour (NYSE:UAA) reported results in line with analysts' expectations in Q1 CY2024, with revenue down 4.8% year on year to $1.33 billion. It made a non-GAAP profit of $0.11 per share, down from its profit of $0.18 per share in the same quarter last year.

Under Armour (UAA) Q1 CY2024 Highlights:

- Revenue: $1.33 billion vs analyst estimates of $1.33 billion (small beat)

- EPS (non-GAAP): $0.11 vs analyst estimates of $0.08 ($0.03 beat)

- Company will undertake a restructuring

- CEO: "Due to a confluence of factors, including lower wholesale channel demand and inconsistent execution across our business, we are seizing this critical moment to make proactive decisions to build a premium positioning for our brand, which will pressure our top and bottom line in the near term"

- Full year revenue guidance: sales down low double-digit percentage rate (Wall Street Consensus was expecting 1.8% year on year growth)

- Full year EPS (non-GAAP) guidance: $0.20 at the midpoint, well below Wall Street Consensus of $0.59

- Gross Margin (GAAP): 45%, up from 43.4% in the same quarter last year

- Market Capitalization: $2.93 billion

Founded in 1996 by a former University of Maryland football player, Under Armour (NYSE:UAA) is an apparel brand specializing in sportswear designed to improve athletic performance.

Under Armour gained popularity through its moisture-wicking synthetic fabric, a revolutionary technology at the time, designed to keep athletes cool and dry during exercise. This set the company apart in its early days and remains a cornerstone of its product lines. The brand has since expanded its offerings to include compression wear, performance footwear, and sports accessories.

The company invests in research and development to enhance its products. This has led to the introduction of fabrics including "HeatGear" and "ColdGear", which regulate body temperature. The company has also created online fitness platforms and smart gear that integrate digital technology into workout apparel.

Under Armour’s marketing strategy has been an important part of the business. The brand has forged partnerships with high-profile athletes and teams across various sports, leveraging these relationships to enhance its visibility and appeal. Additionally, Under Armour's marketing campaigns often focus on the determination and grit of athletes, resonating with consumers who are passionate about fitness and sports.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Under Armour's primary competitors include Nike (NYSE:NKE), Lululemon (NASDAQ:LULU), Columbia Sportswear (NASDAQ:COLM), Adidas (ETR:ADS), and Puma (ETR:PUM).Sales Growth

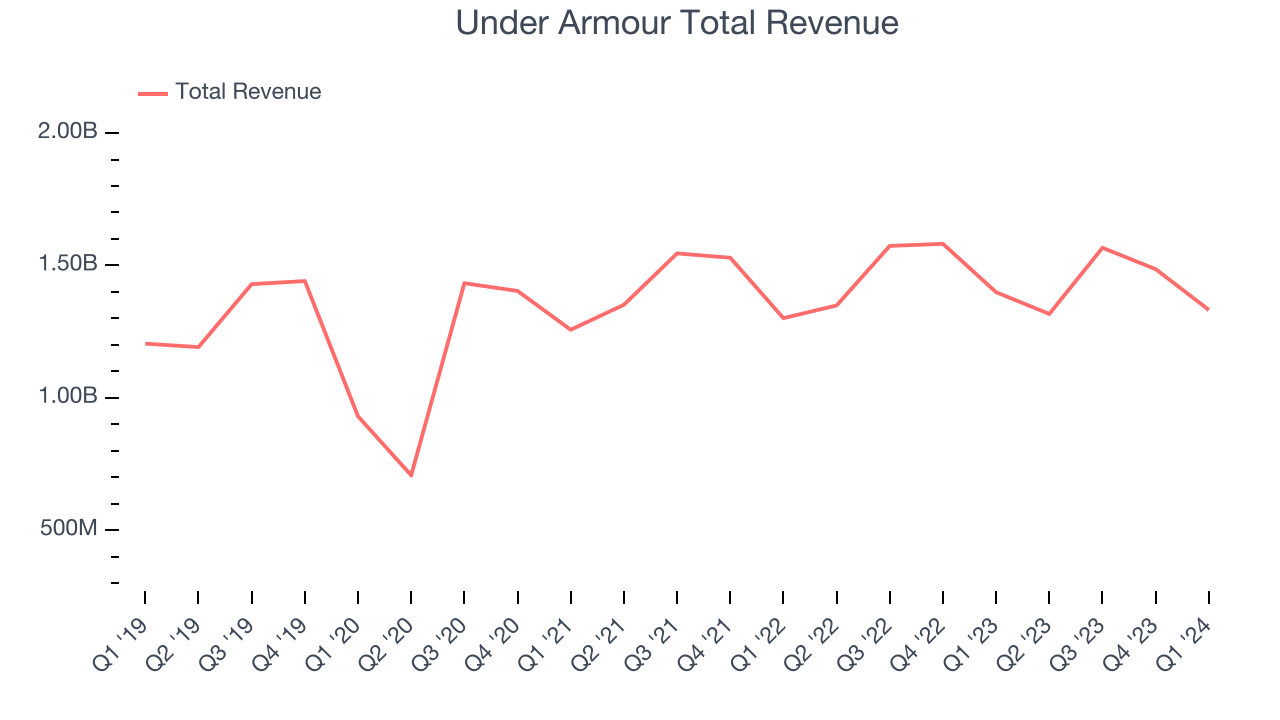

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Under Armour's annualized revenue growth rate of 2.7% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Under Armour's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Under Armour's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

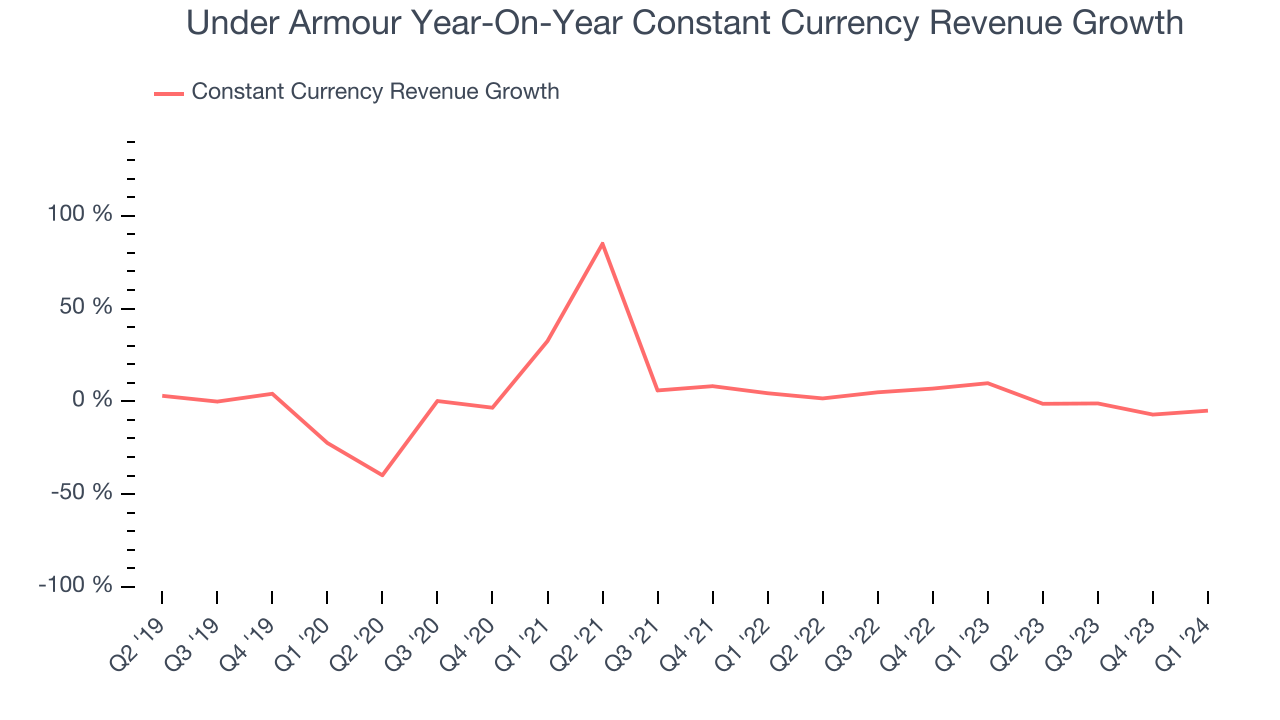

Under Armour also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 1.1% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see Under Armour's foreign exchange rates have been steady.

This quarter, Under Armour reported a rather uninspiring 4.8% year-on-year revenue decline to $1.33 billion of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 2% over the next 12 months, an acceleration from this quarter.

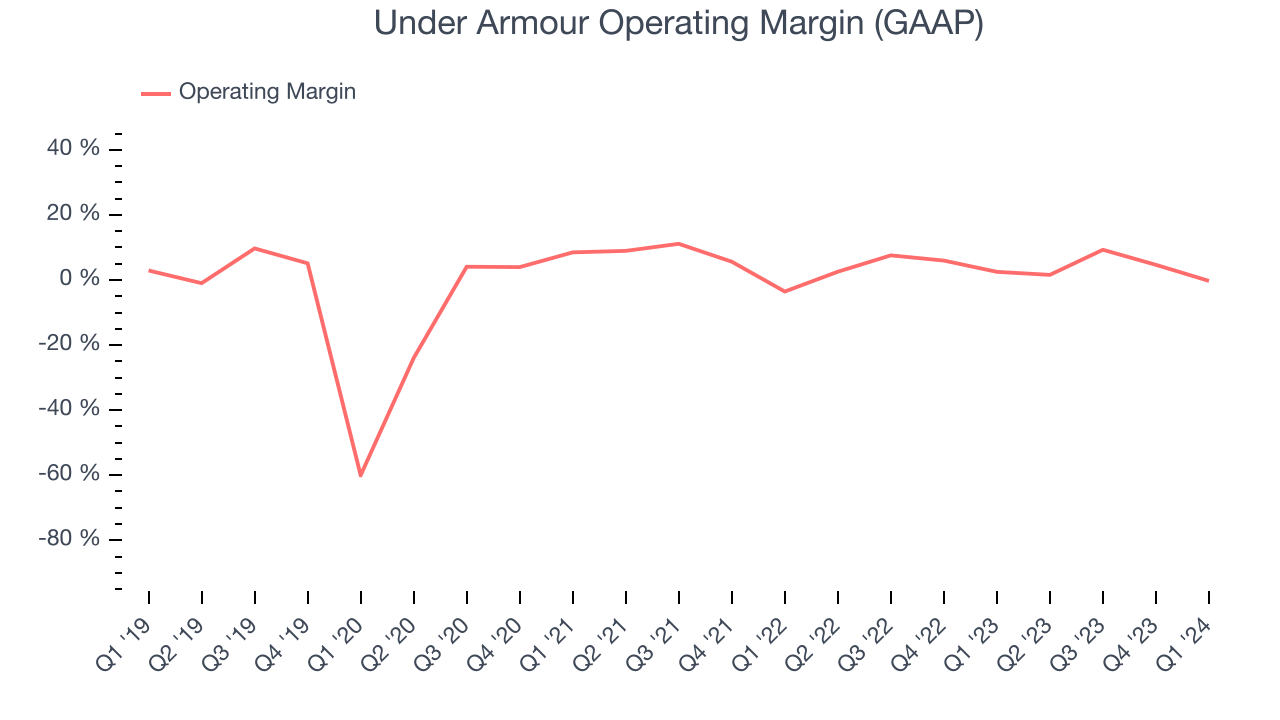

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Under Armour was profitable over the last two years but held back by its large expense base. Its average operating margin of 4.5% has been paltry for a consumer discretionary business.

This quarter, Under Armour generated an operating profit margin of negative 0.3%, down 2.8 percentage points year on year.

Over the next 12 months, Wall Street expects Under Armour to become more profitable. Analysts are expecting the company’s LTM operating margin of 4.1% to rise to 6.1%.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last four years, Under Armour cut its earnings losses and improved its EPS by 49.9% each year.

In Q1, Under Armour reported EPS at $0.11, down from $0.18 in the same quarter last year. Despite falling year on year, this print beat analysts' estimates by 45.7%. Over the next 12 months, Wall Street expects Under Armour to grow its earnings. Analysts are projecting its LTM EPS of $0.56 to climb by 5% to $0.59.

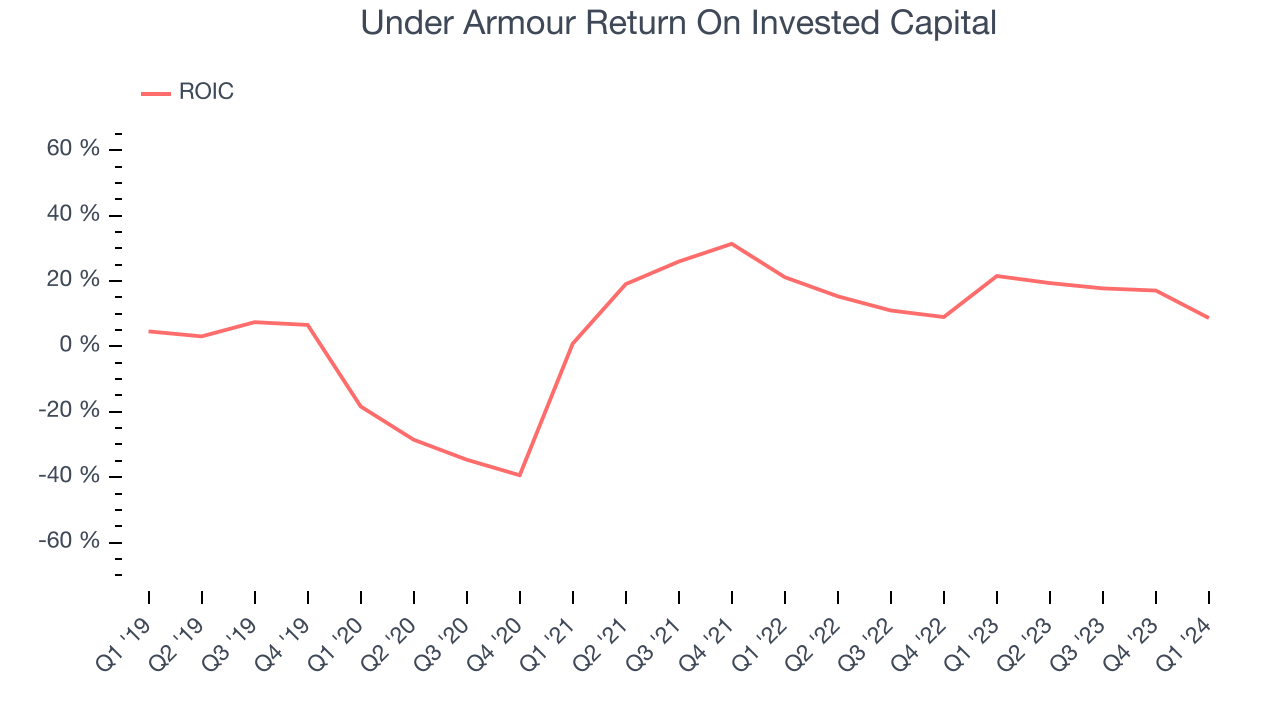

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Under Armour's five-year average return on invested capital was 6.8%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Under Armour's ROIC has significantly increased. This is a good sign, and we hope the company can continue improving.

Key Takeaways from Under Armour's Q1 Results

The quarter's results were fine, but the big news is a restructuring that Under Armour is initiating. To explain the rationale of the restructuring, the company's CEO stated that "Due to a confluence of factors, including lower wholesale channel demand and inconsistent execution across our business, we are seizing this critical moment to make proactive decisions to build a premium positioning for our brand, which will pressure our top and bottom line in the near term". Because of this, Under Armour provided full year guidance that was well below expectations for sales and EPS, as the company will have to endure some shorter-term pain to rightsize the business for the longer term. The stock is down 15.8% on the results and currently trades at $5.72 per share.

Is Now The Time?

Under Armour may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Under Armour, we'll be cheering from the sidelines. Its revenue growth has been weak over the last five years. And while its EPS growth over the last four years has been fantastic, the downside is its constant currency sales performance has been disappointing. On top of that, its low free cash flow margins give it little breathing room.

Under Armour's price-to-earnings ratio based on the next 12 months is 11.6x. While there are some things to like about Under Armour and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $15.50 per share right before these results (compared to the current share price of $5.72).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.