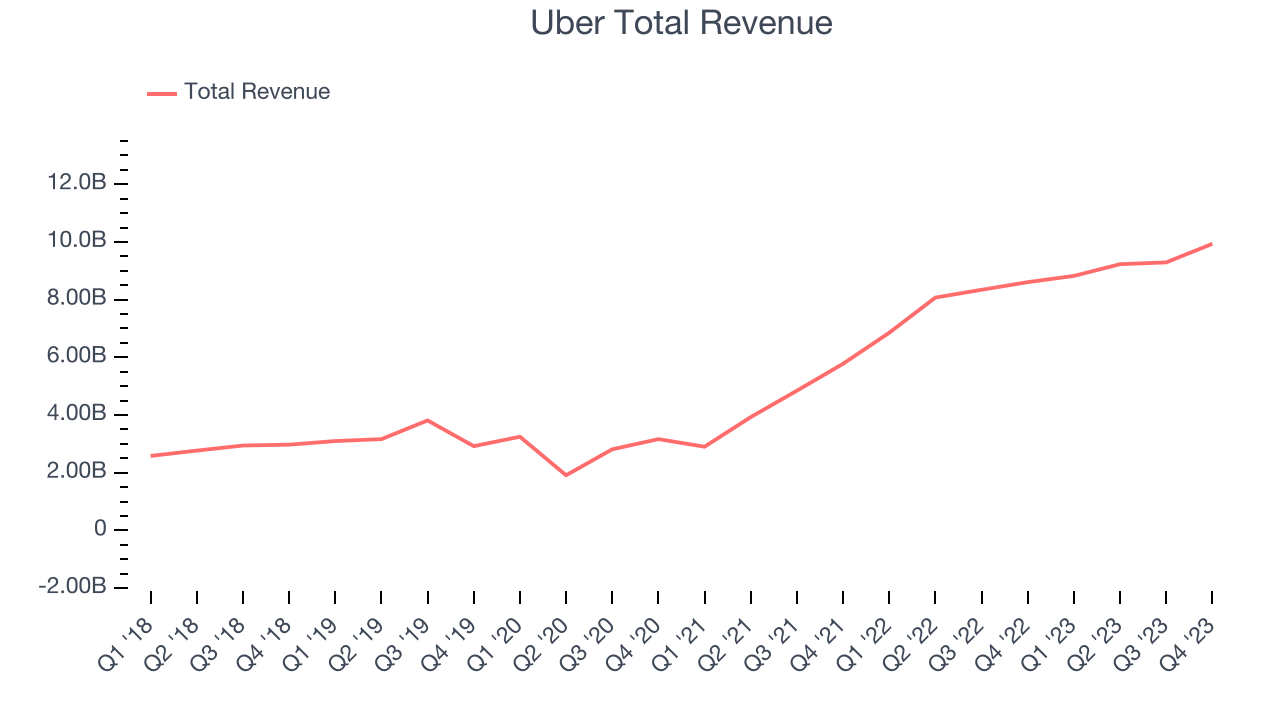

Ride sharing and on demand delivery service Uber (NYSE: UBER) reported results ahead of analysts' expectations in Q4 FY2023, with revenue up 15.4% year on year to $9.94 billion. It made a GAAP profit of $0.66 per share, improving from its profit of $0.29 per share in the same quarter last year.

Uber (UBER) Q4 FY2023 Highlights:

- Revenue: $9.94 billion vs analyst estimates of $9.76 billion (1.8% beat)

- EPS: $0.66 vs analyst estimates of $0.17 (293% beat)

- Free Cash Flow of $768 million, down 15.1% from the previous quarter

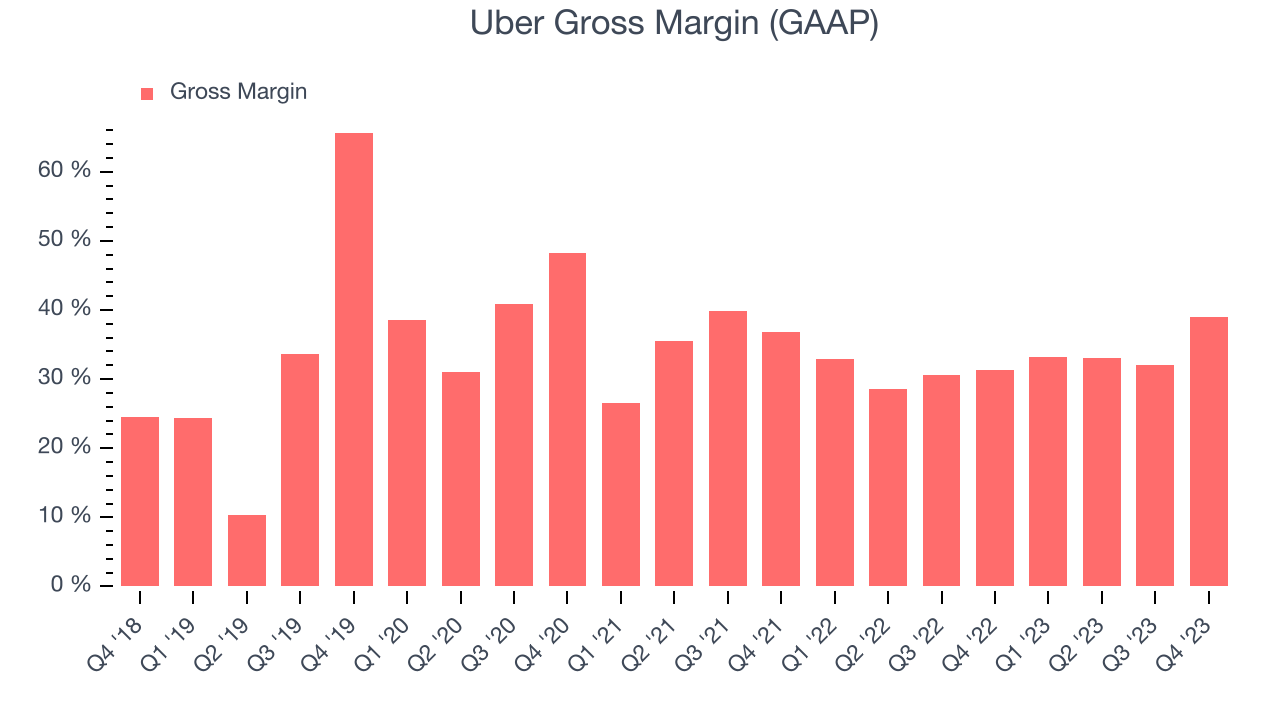

- Gross Margin (GAAP): 39%, up from 31.3% in the same quarter last year

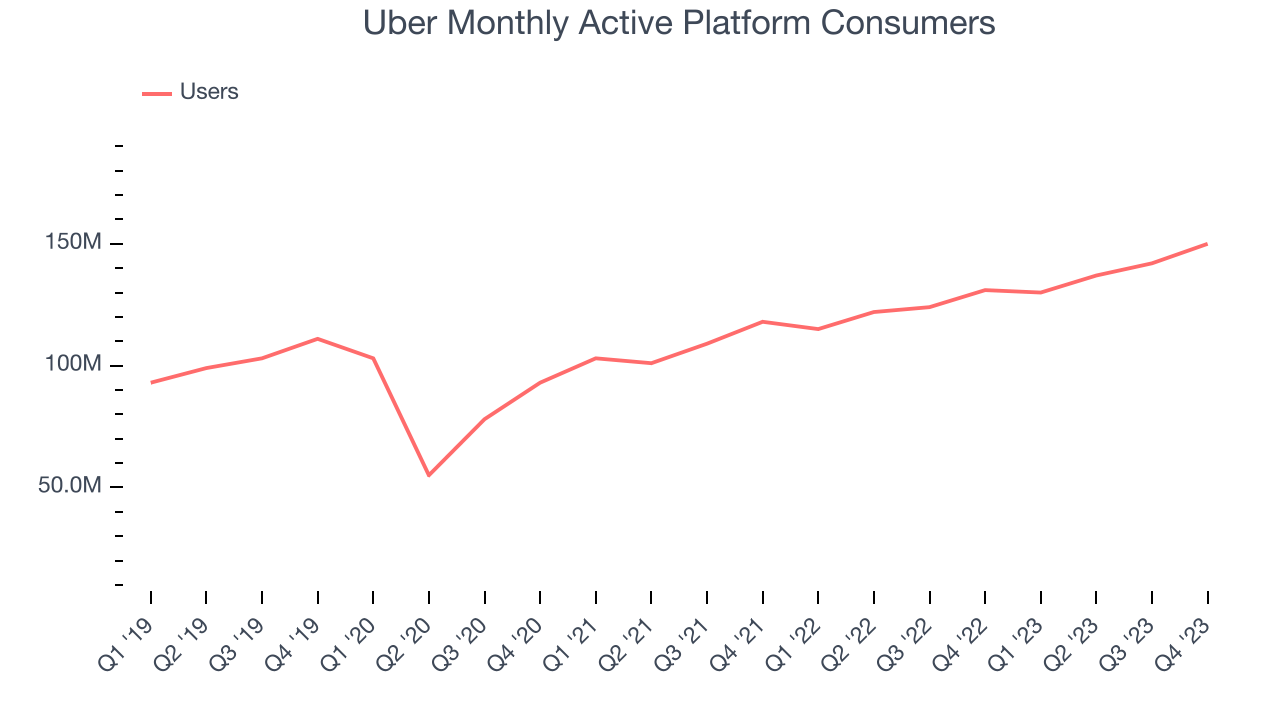

- Monthly Active Platform Consumers: 150 million, up 19 million year on year

- Powered nearly 26 million Daily Trips in 2023 and made its first full-year GAAP profit

- Market Capitalization: $145 billion

Born out of a winter night thought: "What if you could request a ride from your phone?" Uber (NYSE: UBER) operates a global network of on demand services, most prominently ride hailing and food delivery, and freight.

Uber pioneered the online ride hailing model, allowing users to summon taxi’s via their mobile devices, an innovation that disrupted modern transportation. The company next expanded into food delivery with UberEats, and has grown a trucking brokerage business, Uber Freight. It is the largest global ride sharing network, with majority market share in the most countries it operates in.

The company’s value propositions are multiple. For individuals, Uber effectively lowered the cost per mile for taxi transportation vs. legacy cabs, while providing ease of use and convenience. For drivers, it has provided flexible earning opportunities. While for restaurants and merchants, Uber’s platform has allowed them to expand their consumer reach, and provided an online presence.

Gig Economy

The iPhone changed the world, ushering in the era of the “always-on” internet and “on-demand” services - anything someone could want is just a few taps away. Likewise, the gig economy sprang up in a similar fashion, with a proliferation of tech-enabled freelance labor marketplaces, which work hand and hand with many on demand services. Individuals can now work on demand too. What began with tech enabled platforms that aggregated riders and drivers has expanded over the past decade to include food delivery, groceries, and now even a plumber or graphic designer are all just a few taps away.

Uber competes with rival Lyft (NASDAQ: LYFT) in ride hailing and DoorDash (NYSE:DASH), Just Eat Takeaway (ENXTAM:TKWY), Delivery Hero (XTRA: DHER), and Deliveroo (LSE:ROO).

Sales Growth

Uber's revenue growth over the last three years has been exceptional, averaging 56.8% annually. This quarter, Uber beat analysts' estimates and reported 15.4% year-on-year revenue growth.

Usage Growth

As a gig economy marketplace, Uber generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, Uber's users, a key performance metric for the company, grew 13.9% annually to 150 million. This is solid growth for a consumer internet company.

In Q4, Uber added 19 million users, translating into 14.5% year-on-year growth.

Revenue Per User

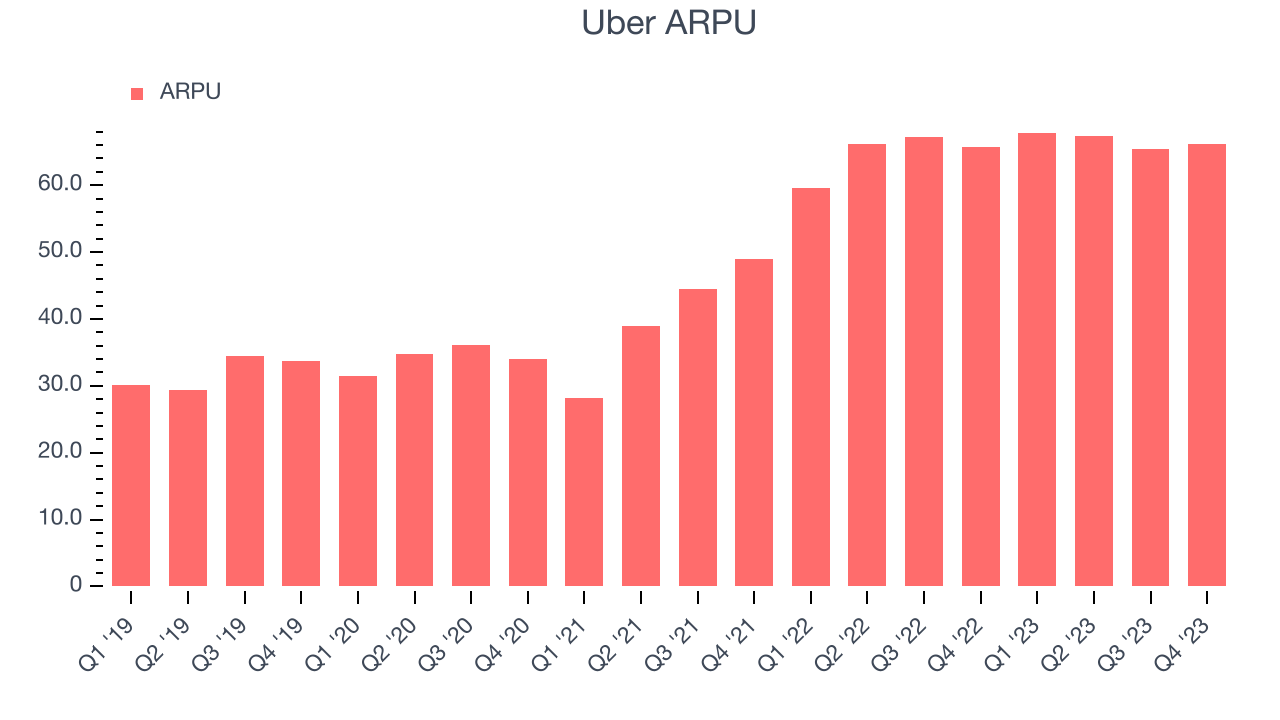

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Uber because it measures how much the company earns in transaction fees from each user. This number also informs us about Uber's take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Uber's ARPU growth has been exceptional over the last two years, averaging 35.1%. The company's ability to increase prices while growing its users demonstrates its platform's value, as its users are spending significantly more than last year. This quarter, ARPU grew 0.8% year on year to $66.24 per user.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor. Uber's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 39% this quarter, up 7.7 percentage points year on year.

For gig economy businesses like Uber, these aforementioned costs typically include server hosting, customer support, and payment processing fees. Another cost of revenue could also be insurance to protect against liabilities arising from providing transportation, housing, or freelance work services. After paying for these expenses, Uber had $0.39 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

Uber's gross margins have been trending up over the last 12 months, averaging 34.3%. This is a welcome development, as Uber's margins are below the industry average, and rising margins could suggest improved demand and pricing power.

User Acquisition Efficiency

Unlike enterprise software that's typically sold by dedicated sales teams, consumer internet businesses like Uber grow from a combination of product virality, paid advertisement, and incentives.

Uber is efficient at acquiring new users, spending 34.7% of its gross profit on sales and marketing expenses over the last year. This level of efficiency indicates relatively solid competitive positioning, giving Uber the freedom to invest its resources into new growth initiatives.

Profitability & Free Cash Flow

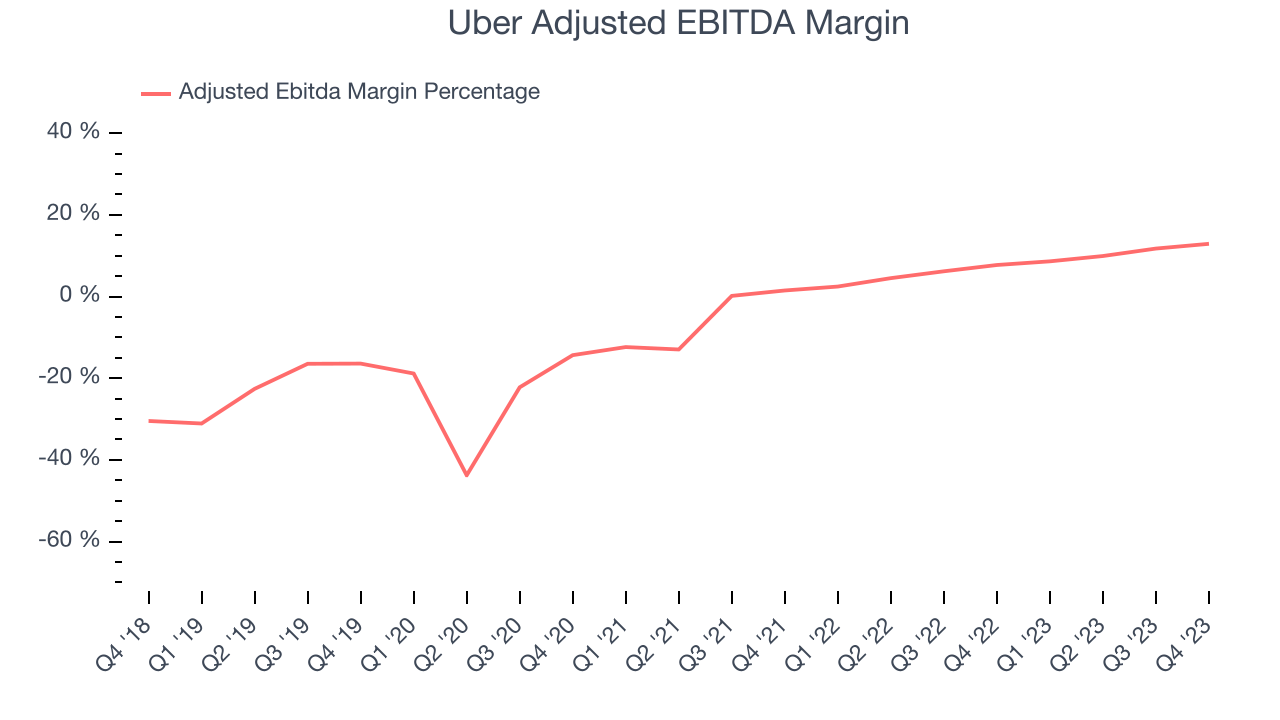

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

This quarter, Uber's EBITDA came in at $1.28 billion, resulting in a 12.9% margin. The company has also shown above-average profitability for a consumer internet business over the last four quarters, with average EBITDA margins of 10.8%.

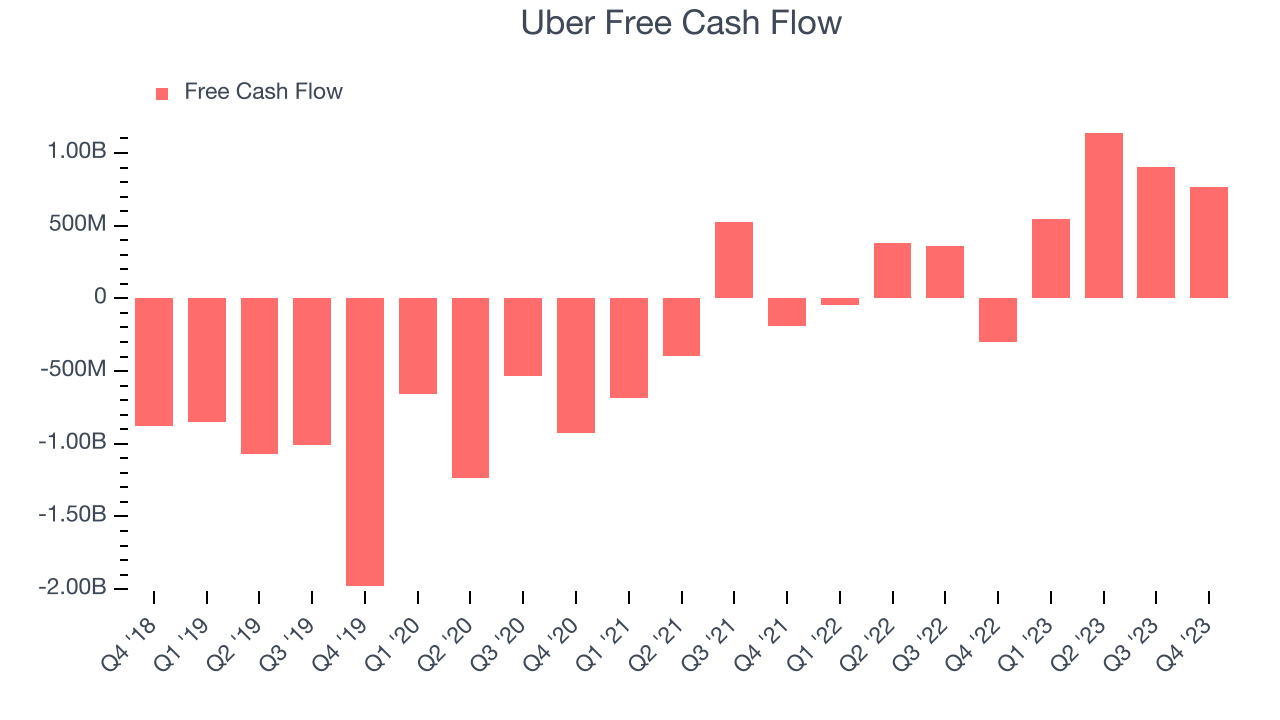

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Uber's free cash flow came in at $768 million in Q4, turning positive year on year.

Uber has generated $3.36 billion in free cash flow over the last 12 months, a solid 9% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from Uber's Q4 Results

It was great to see Uber's strong user growth this quarter. We were also happy its revenue, EBITDA, and EPS outperformed Wall Street's estimates. This was driven by not only user growth but also better-than-expected gross bookings in both its mobility ($19.3 billion vs estimates of $19.1 billion) and delivery ($17.0 billion vs estimates of $16.7 billion) segments. 2023 was a milestone year for the company as it finally turned a profit and powered nearly 26 million daily trips. Looking ahead, Uber's gross bookings and EBITDA guidance also beat analysts' forecasts. Zooming out, we think this was a decent quarter, showing that the company is staying on track. The stock is up 1.2% after reporting and currently trades at $71.3 per share.

Is Now The Time?

When considering an investment in Uber, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Uber is a good business. Its revenue growth has been exceptional over the last three years. And while its gross margins make it extremely difficult to reach positive operating profits compared to other consumer internet businesses, the good news is its top-tier ARPU growth shows the increasing value of its platform to its users. On top of that, its user acquisition is efficient.

At the moment Uber trades at 24.9x next 12 months EV-to-EBITDA. There's definitely a lot of things to like about Uber and looking at the consumer internet landscape right now, it seems that the company trades at a pretty interesting price point.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.