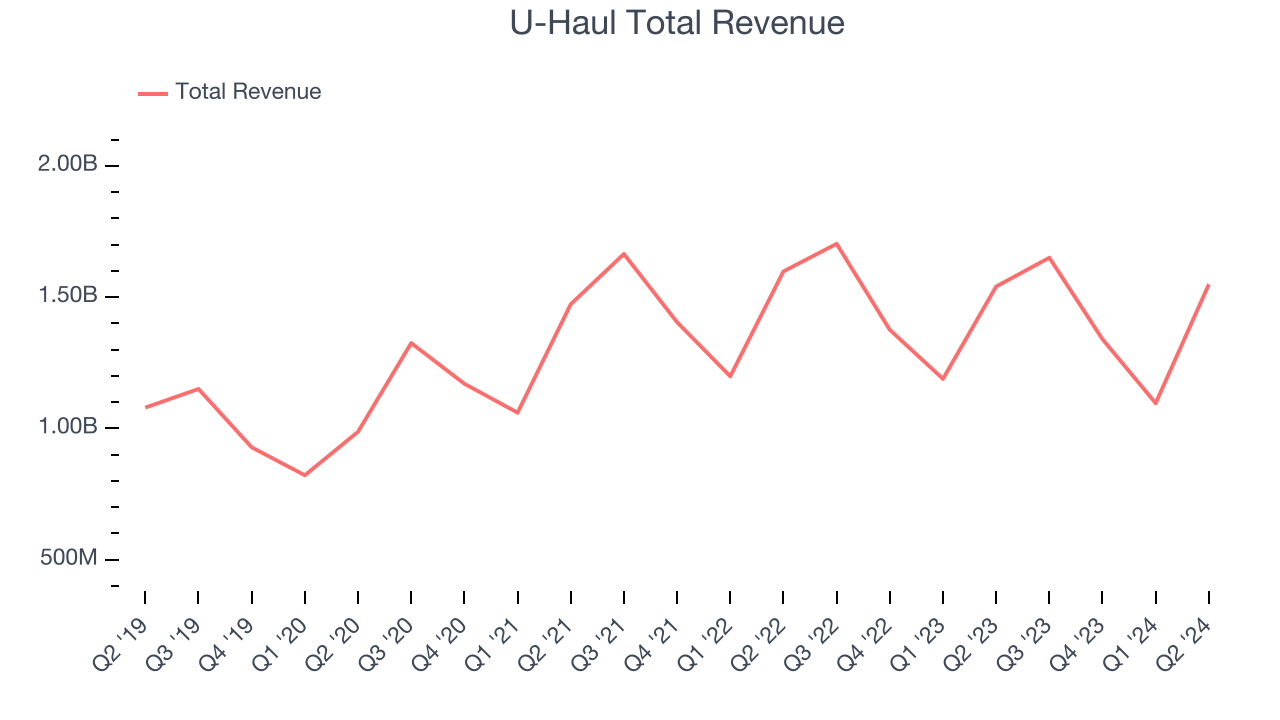

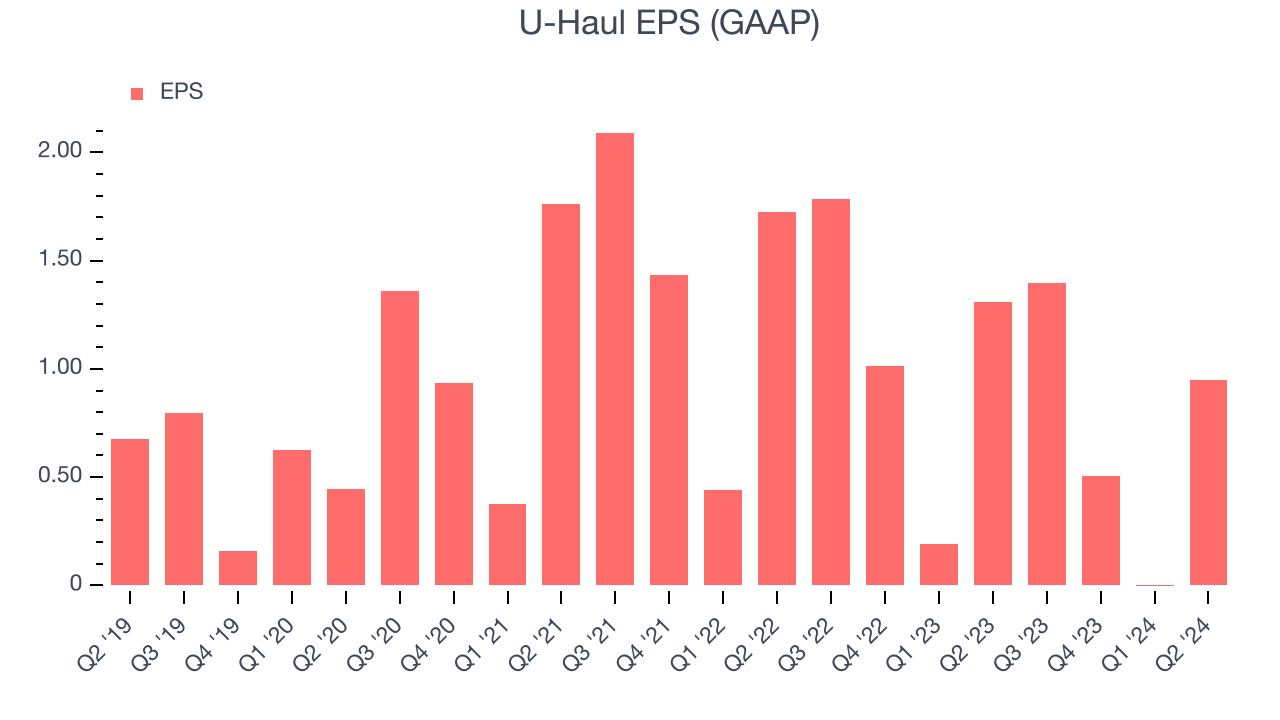

Moving and storage solutions provider U-Haul (NYSE:UHAL) reported results in line with analysts' expectations in Q2 CY2024, with revenue flat year on year at $1.55 billion. It made a GAAP profit of $0.95 per share, down from its profit of $1.31 per share in the same quarter last year.

Is now the time to buy U-Haul? Find out by accessing our full research report, it's free.

U-Haul (UHAL) Q2 CY2024 Highlights:

- Revenue: $1.55 billion vs analyst estimates of $1.54 billion (small beat)

- EPS: $0.95 vs analyst expectations of $1.20 (20.8% miss)

- Market Capitalization: $12.06 billion

Founded by a husband and wife, U-Haul (NYSE:UHAL) offers truck and trailer rentals and self storage units.

Ground Transportation

The growth of e-commerce and global trade continues to drive demand for shipping services, especially last-mile delivery, presenting opportunities for ground transportation companies. The industry continues to invest in data, analytics, and autonomous fleets to optimize efficiency and find the most cost-effective routes. Despite the essential services this industry provides, ground transportation companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Over the last five years, U-Haul grew its sales at a decent 7.9% compounded annual growth rate. This shows it was successful in expanding, a useful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. U-Haul's recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2% over the last two years.

This quarter, U-Haul's $1.55 billion of revenue was flat year on year and in line with Wall Street's estimates. We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

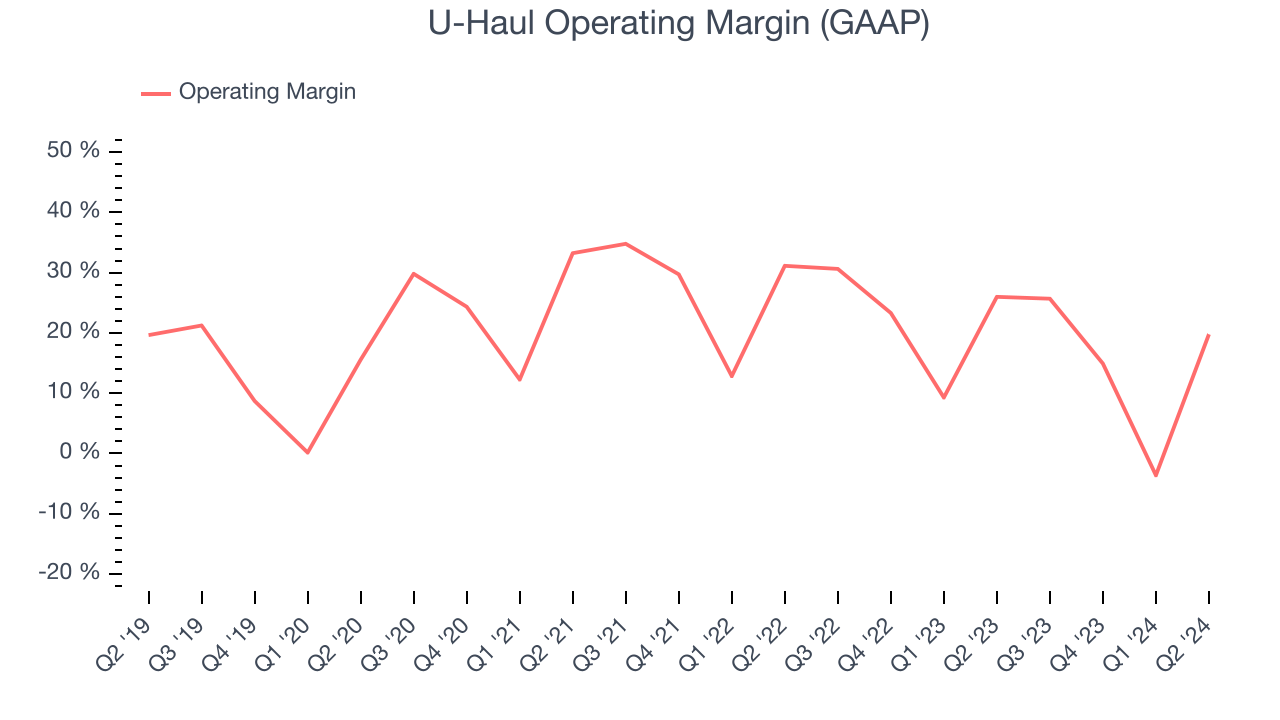

Operating Margin

U-Haul has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 21.6%. This result isn't surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, U-Haul's annual operating margin rose by 3.5 percentage points over the last five years, showing its efficiency has improved.

This quarter, U-Haul generated an operating profit margin of 19.8%, down 6.2 percentage points year on year. Conversely, the company's gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like sales, marketing, R&D, and administrative overhead.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

U-Haul's EPS grew at an unimpressive 6.1% compounded annual growth rate over the last five years, lower than its 7.9% annualized revenue growth. However, its operating margin actually expanded during this timeframe, telling us non-fundamental factors affected its ultimate earnings.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. U-Haul's two-year annual EPS declines of 29.3% were bad and lower than its two-year revenue performance.

In Q2, U-Haul reported EPS at $0.95, down from $1.31 in the same quarter last year. This print missed analysts' estimates. We also like to analyze expected EPS growth based on Wall Street analysts' consensus projections, but there is insufficient data.

Key Takeaways from U-Haul's Q2 Results

EPS missed by a fairly large amount. The stock traded down 5% to $60.11 immediately after reporting.

U-Haul may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.