Quarterly earnings results are a good time to check in on a company’s progress, especially compared to other peers in the same sector. Today we are looking at Veeva Systems (NYSE:VEEV), and the best and worst performers in the vertical software group.

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, there are industries that have very specific needs. Whether it is life-sciences, education or banking, the demand for so called vertical software, addressing industry specific workflows, is growing, fueled by the pressures on improving productivity and quality of offerings.

The 11 vertical software stocks we track reported a weaker Q3; on average, revenues were in line with analyst consensus estimates, while on average next quarter revenue guidance was 2.32% under consensus. Tech stocks have been hit the hardest as investors start to value profits over growth, but vertical software stocks held their ground better than others, with the share prices up 1% since the previous earnings results, on average.

Veeva Systems (NYSE:VEEV)

Built on top of Salesforce as one of the first vertical-focused cloud platforms, Veeva (NYSE:VEEV) provides data and customer relationship management (CRM) software for organizations in the life sciences industry.

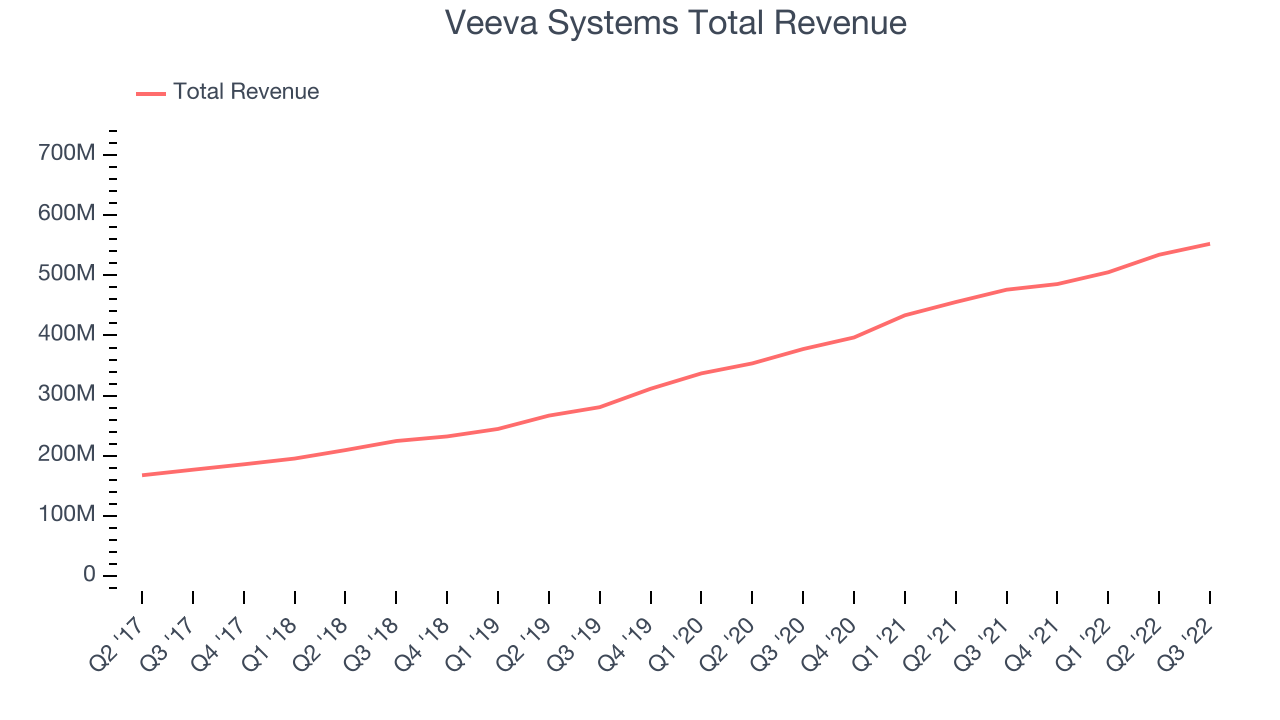

Veeva Systems reported revenues of $552.3 million, up 16% year on year, beating analyst expectations by 1.15%. It was a weaker quarter for the company, with revenue guidance for the next quarter and the full year missing analysts' expectations.

"Consistent execution and strong innovation have us tracking a year ahead of our 2025 targets and set up for significant growth toward 2030 and beyond," said CEO Peter Gassner.

The stock is down 17.9% since the results and currently trades at $157.20.

Read our full report on Veeva Systems here, it's free.

Best Q3: Toast (NYSE:TOST)

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE:TOST) provides integrated point of sale (POS) hardware, software, and payments solutions for restaurants.

Toast reported revenues of $752 million, up 54.6% year on year, beating analyst expectations by 4.31%. It was a very strong quarter for the company, with a significant improvement in gross margin and exceptional revenue growth.

Toast delivered the fastest revenue growth among its peers. The stock is down 10.3% since the results and currently trades at $17.95.

Is now the time to buy Toast? Access our full analysis of the earnings results here, it's free.

Weakest Q3: Upstart (NASDAQ:UPST)

Founded by the former head of Google's enterprise business Dave Girouard, Upstart (NASDAQ:UPST) is an AI-powered lending platform that helps banks better evaluate the risk of lending money to a person and provide loans to more customers.

Upstart reported revenues of $157.2 million, down 31.2% year on year, missing analyst expectations by 7.2%. It was a weak quarter for the company, with declining revenue and underwhelming guidance for the next quarter.

Upstart had the weakest performance against analyst estimates in the group. The stock is down 29.4% since the results and currently trades at $13.45.

Read our full analysis of Upstart's results here.

nCino (NASDAQ:NCNO)

Founded in 2011 in North Carolina, nCino (NASDAQ:NCNO) makes cloud-based operating systems for banks and provides that software as a service.

nCino reported revenues of $105.2 million, up 50.3% year on year, beating analyst expectations by 1.78%. It was a mixed quarter for the company, with exceptional revenue growth but underwhelming revenue guidance for the next quarter.

The stock is up 1.61% since the results and currently trades at $26.50.

Read our full, actionable report on nCino here, it's free.

2U (NASDAQ:TWOU)

Originally named 2tor after the founder's dog Tor, 2U (NASDAQ:TWOU) provides software for universities and colleges to deliver online degree programs and courses.

2U reported revenues of $232.2 million, flat year on year, in line with analyst expectations. It was a weak quarter for the company, with a decline in gross margin.

The stock is up 17.3% since the results and currently trades at $7.49.

Read our full, actionable report on 2U here, it's free.

The author has no position in any of the stocks mentioned