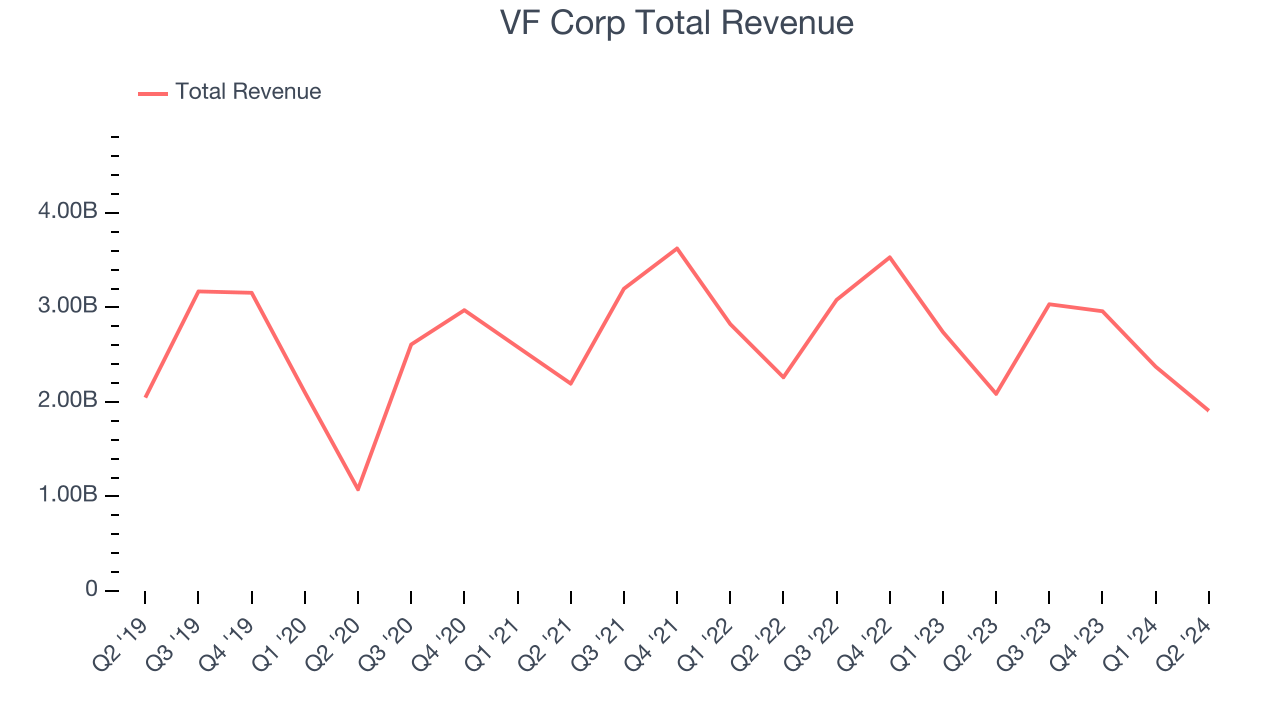

Lifestyle clothing conglomerate VF Corp (NYSE:VFC) reported Q2 CY2024 results exceeding Wall Street analysts' expectations, with revenue down 8.6% year on year to $1.91 billion. It made a non-GAAP loss of $0.33 per share, down from its loss of $0.15 per share in the same quarter last year.

Is now the time to buy VF Corp? Find out by accessing our full research report, it's free.

VF Corp (VFC) Q2 CY2024 Highlights:

- Revenue: $1.91 billion vs analyst estimates of $1.85 billion (3.3% beat)

- EPS (non-GAAP): -$0.33 vs analyst estimates of -$0.37

- Gross Margin (GAAP): 52%, down from 52.8% in the same quarter last year

- Adjusted EBITDA Margin: -9%, down from 2.8% in the same quarter last year

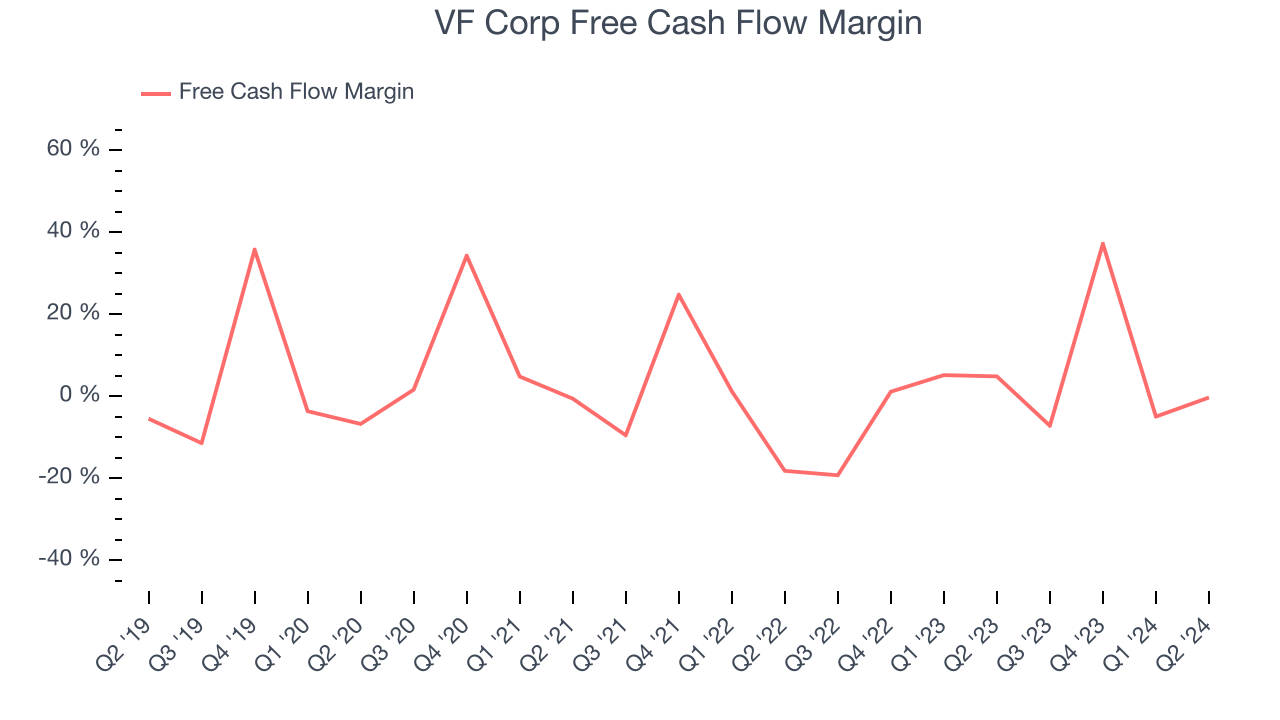

- Free Cash Flow was -$5.36 million compared to -$117.3 million in the previous quarter

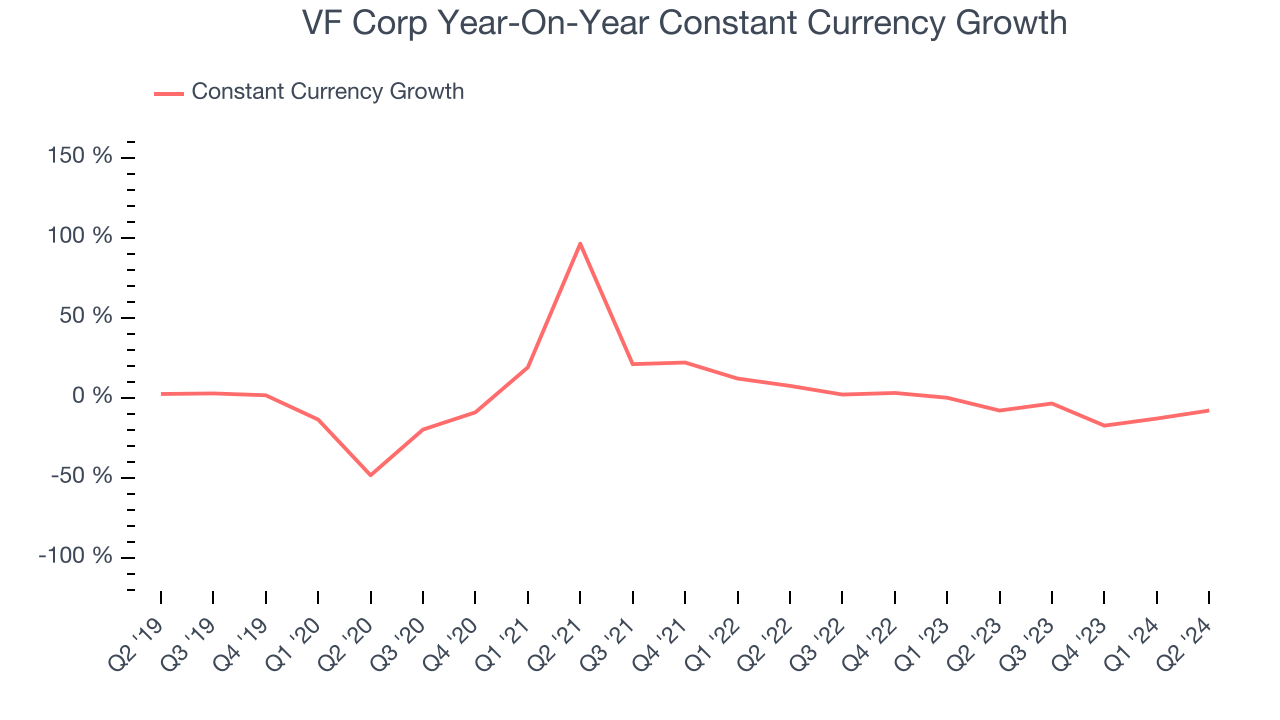

- Constant Currency Revenue fell 8% year on year, in line with the same quarter last year

- Market Capitalization: $6.25 billion

Owner of The North Face, Vans, and Supreme, VF Corp (NYSE:VFC) is a clothing conglomerate specializing in branded lifestyle apparel, footwear, and accessories.

Apparel, Accessories and Luxury Goods

Within apparel and accessories, not only do styles change more frequently today than decades past as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel, accessories, and luxury goods companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. VF Corp's demand was weak over the last five years as its sales were flat, a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. VF Corp's recent history shows its demand has stayed suppressed as its revenue has declined by 7.1% annually over the last two years.

We can dig further into the company's sales dynamics by analyzing its constant currency revenue, which exclude currency movements that are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.6% year-on-year declines. Because this number aligns with its normal revenue growth, we can see VF Corp's foreign exchange rates have been steady.

This quarter, VF Corp's revenue fell 8.6% year on year to $1.91 billion but beat Wall Street's estimates by 3.3%. Looking ahead, Wall Street expects revenue to decline 1.9% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

VF Corp has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.1%, lousy for a consumer discretionary business.

VF Corp broke even from a free cash flow perspective in Q2. The company's cash profitability regressed as it was 5.2 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren't a big deal because investment needs can be seasonal, but we'll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from VF Corp's Q2 Results

We were impressed by how significantly VF Corp blew past analysts' constant currency revenue expectations this quarter. We were also excited its revenue outperformed Wall Street's estimates. Overall, we think this was a strong quarter that should satisfy shareholders. The stock traded up 3.5% to $17 immediately following the results.

VF Corp may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.