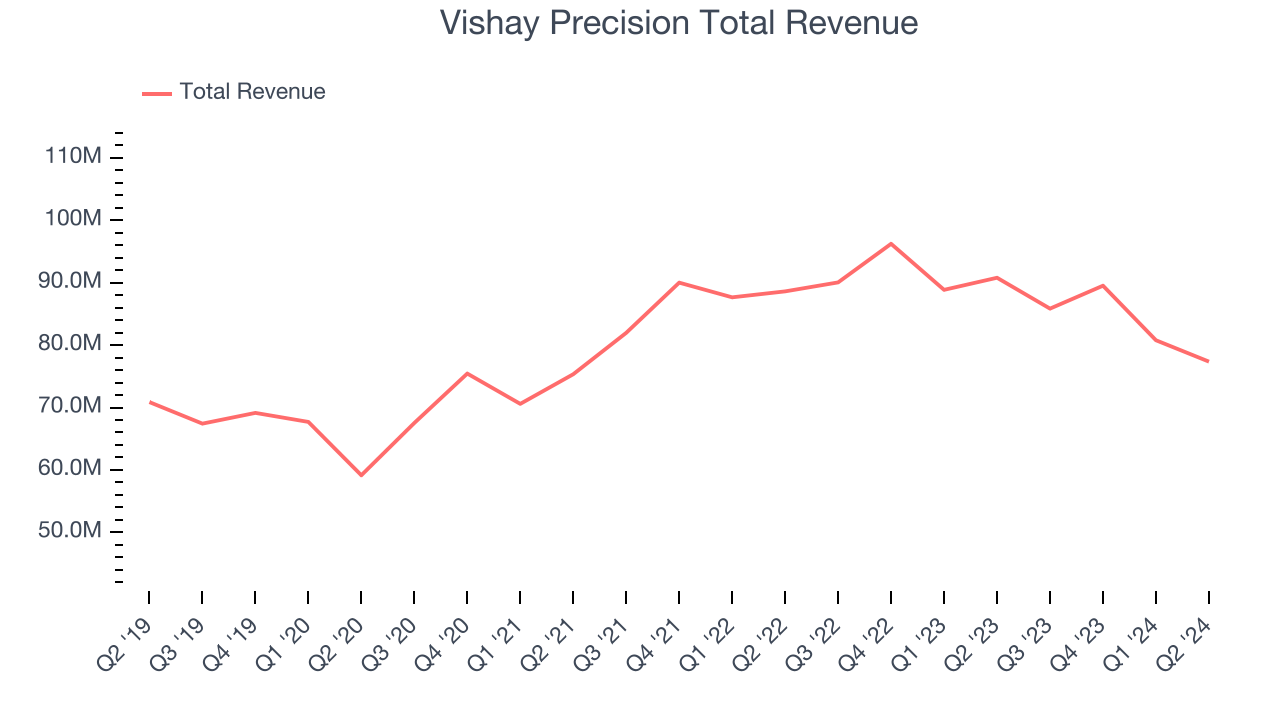

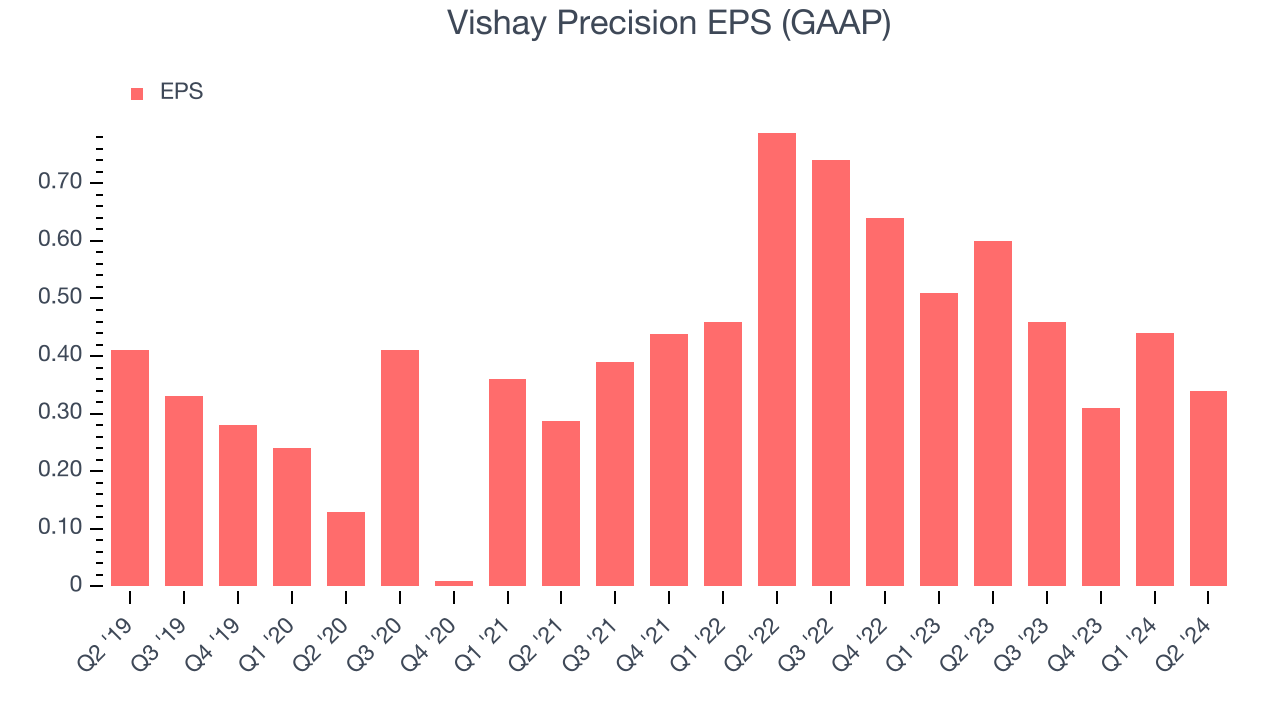

Precision measurement and sensing technologies provider Vishay Precision (NYSE:VPG) fell short of analysts' expectations in Q2 CY2024, with revenue down 14.8% year on year to $77.36 million. Next quarter's revenue guidance of $74 million also underwhelmed, coming in 6% below analysts' estimates. It made a GAAP profit of $0.34 per share, down from its profit of $0.60 per share in the same quarter last year.

Is now the time to buy Vishay Precision? Find out by accessing our full research report, it's free.

Vishay Precision (VPG) Q2 CY2024 Highlights:

- Revenue: $77.36 million vs analyst estimates of $79.62 million (2.8% miss)

- EPS: $0.34 vs analyst estimates of $0.32 (7.9% beat)

- Revenue Guidance for Q3 CY2024 is $74 million at the midpoint, below analyst estimates of $78.71 million

- Gross Margin (GAAP): 41.9%, down from 42.7% in the same quarter last year

- Adjusted EBITDA Margin: 13.2%, down from 16.4% in the same quarter last year

- Free Cash Flow of $4.86 million, up 26.8% from the previous quarter

- Market Capitalization: $419.6 million

Ziv Shoshani, Chief Executive Officer of VPG, commented, "Sales in the second quarter were 4.2% lower sequentially reflecting continued mixed trends across our markets. Our book-to-bill in the second quarter improved slightly to 0.95, reflecting orders of $73.5 million which declined slightly sequentially. Demand improved in some cyclical markets such as Steel and consumer, while orders were lower in portions of our Test & Measurement market, as well as in Avionics, Military & Space and our industrial markets, primarily due to project timing and continued cautious ordering by our distributor customers."

Emerging from Vishay Intertechnology in 2010, Vishay Precision (NYSE:VPG) operates as a global provider of precision measurement and sensing technologies.

Electronic Components

Like many equipment and component manufacturers, electronic components companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include data centers and telecommunications, which can benefit companies whose optical and transceiver offerings fit those markets. But like the broader industrials sector, these companies are also at the whim of economic cycles. Consumer spending, for example, can greatly impact these companies’ volumes.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Vishay Precision's sales grew at a weak 2% compounded annual growth rate over the last five years. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Vishay Precision's history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.1% annually. Vishay Precision isn't alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses seeing lower sales at this time.

This quarter, Vishay Precision missed Wall Street's estimates and reported a rather uninspiring 14.8% year-on-year revenue decline, generating $77.36 million of revenue. The company is guiding for a 13.8% year-on-year revenue decline next quarter to $74 million, a deceleration from the 4.7% year-on-year decrease it recorded in the same quarter last year. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

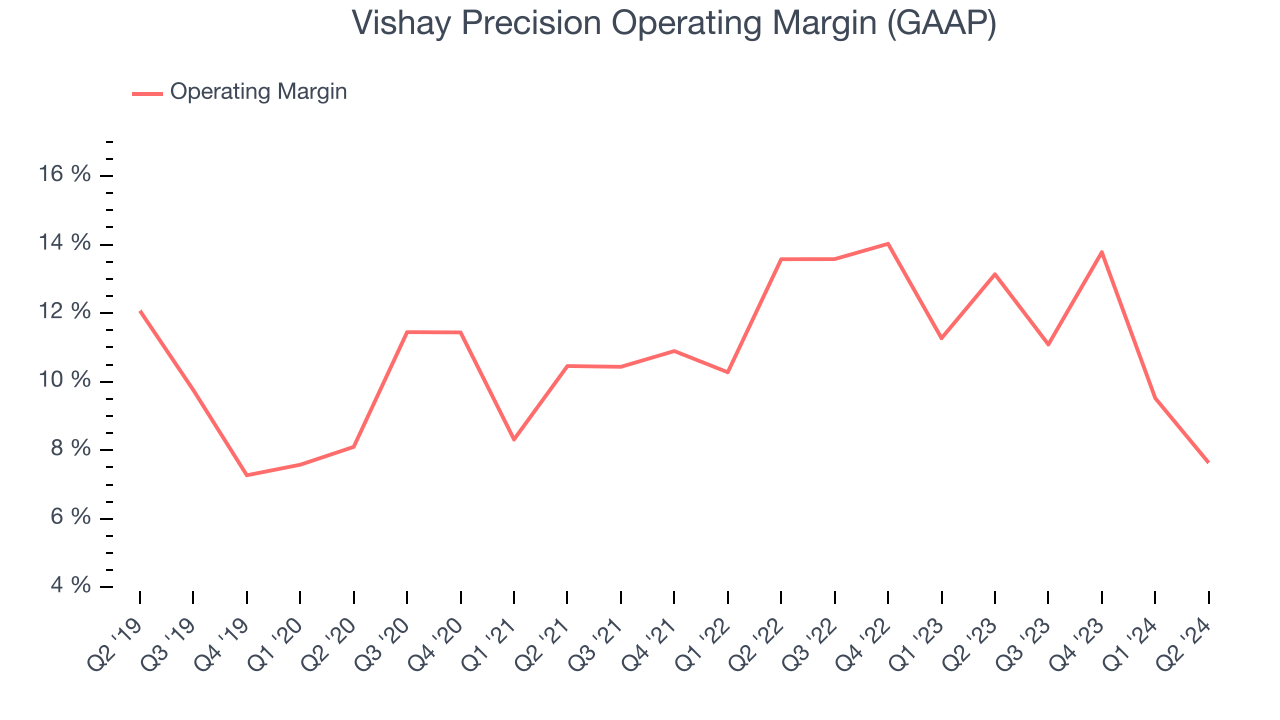

Vishay Precision has managed its expenses well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.9%. This result isn't surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Vishay Precision's annual operating margin rose by 2.5 percentage points over the last five years, showing its efficiency has improved.

This quarter, Vishay Precision generated an operating profit margin of 7.6%, down 5.5 percentage points year on year. Since Vishay Precision's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Sadly for Vishay Precision, its EPS declined by 3.1% annually over the last five years while its revenue grew by 2%. However, its operating margin actually expanded during this timeframe, telling us non-fundamental factors affected its ultimate earnings.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. For Vishay Precision, its two-year annual EPS declines of 13.6% show its recent history was to blame for its underperformance over the last five years. These results were bad no matter how you slice the data.

In Q2, Vishay Precision reported EPS at $0.34, down from $0.60 in the same quarter last year. Despite falling year on year, this print beat analysts' estimates by 7.9%. Over the next 12 months, Wall Street expects Vishay Precision to perform poorly. Analysts are projecting its EPS of $1.55 in the last year to shrink by 14.4% to $1.33.

Key Takeaways from Vishay Precision's Q2 Results

It was good to see Vishay Precision beat analysts' EPS expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its revenue fell short of Wall Street's estimates. Overall, this quarter could have been better. The stock remained flat at $31.42 immediately after reporting.

So should you invest in Vishay Precision right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.