Intimatewear and beauty retailer Victoria’s Secret (NYSE:VSCO) reported results in line with analysts' expectations in Q3 FY2023, with revenue down 4% year on year to $1.27 billion. It made a GAAP loss of $0.92 per share, down from its profit of $0.29 per share in the same quarter last year.

Is now the time to buy Victoria's Secret? Find out by accessing our full research report, it's free.

Victoria's Secret (VSCO) Q3 FY2023 Highlights:

- Revenue: $1.27 billion vs analyst estimates of $1.27 billion (small miss)

- EPS(non-GAAP): -$0.86 vs analyst expectations of -$0.78 ($0.06 miss)

- EPS (non-GAAP) Guidance for Q4 2023 is $2.40 at the midpoint, below analyst estimates of $2.44

- Gross Margin (GAAP): 33.8%, down from 34.7% in the same quarter last year

- Same-Store Sales were down 7% year on year (beat vs. expectations of down 8.5% year on year)

- Store Locations: 1,360 at quarter end, increasing by 9 over the last 12 months

Chief Executive Officer Martin Waters commented on the third quarter, “We delivered third quarter results within our guidance range, and we are encouraged by the improving sales trend as we transition into the all-important holiday season. Our sales trend in North America continued to improve as planned each month throughout the third quarter with October being our strongest month. Our teams have been resiliently focused on what is within our control and working tirelessly on multiple growth initiatives designed to create momentum. We are delivering key initiatives such as our new multi-tender loyalty program, new customer experience enhancements in our digital business, product improvements and launches to enhance the Victoria’s Secret brand and accelerate our beauty business, a reimagined merchandise strategy for our PINK brand, and the return of our iconic fashion show with the Victoria’s Secret World Tour ’23.”

Spun off from L Brands in 2020, Victoria’s Secret (NYSE:VSCO) is an intimate clothing and beauty retailer that sells its own brands of lingerie, undergarments, and personal fragrances.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

Victoria's Secret is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company's annualized revenue growth rate of 7.4% over the last three years was decent despite closing stores.

This quarter, Victoria's Secret reported a rather uninspiring 4% year-on-year revenue decline, missing Wall Street's expectations. Looking ahead, analysts expect sales to grow 1.7% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

The number of stores a retailer operates is a major determinant of how much it can sell, and its growth is a critical driver of how quickly company-level sales can grow.

When a retailer like Victoria's Secret keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. As of the most recently reported quarter, Victoria's Secret operated 1,360 total retail locations, in line with its store count a year ago.

Taking a step back, the company has kept its physical footprint more or less flat over the last two years while other consumer retail businesses have opted for growth. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

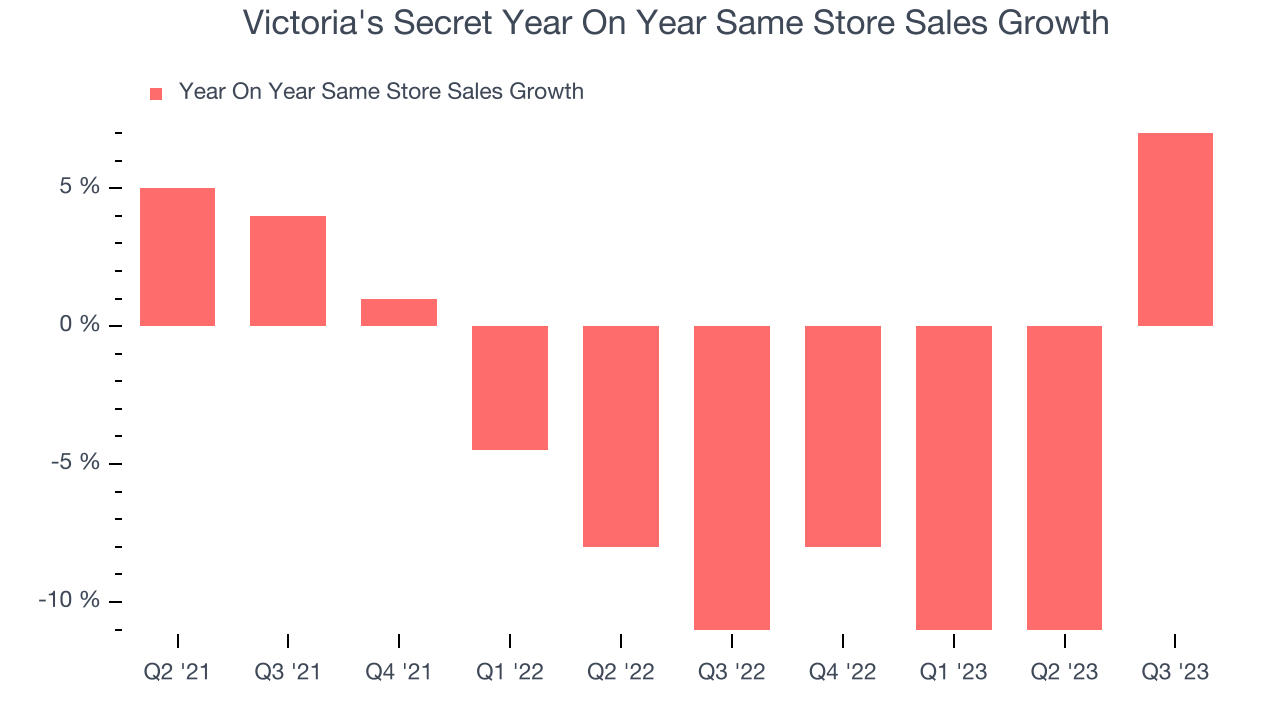

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Victoria's Secret's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 7.4% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Victoria's Secret's same-store sales fell 7% year on year. This decrease was a further deceleration from the 11% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Victoria's Secret's Q3 Results

While the same-store sales beat was a major positive, revenue and EPS missed. Guidance for next quarter and the full year were both below expectations. Overall, this was a mixed but generally negative quarter for Victoria's Secret. The stock is flat after reporting and currently trades at $23.67 per share.

Victoria's Secret may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.