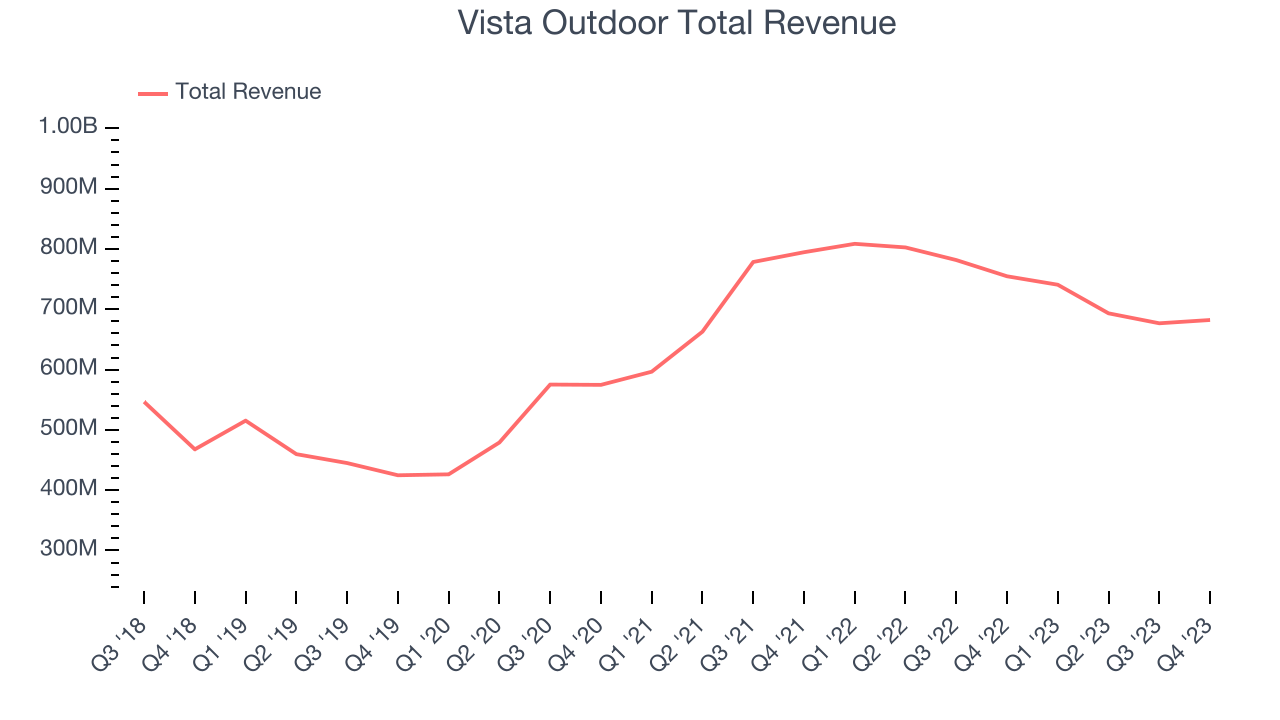

Outdoor sports and recreation products corporation (NYSE:VSTO) missed analysts' expectations in Q3 FY2024, with revenue down 9.6% year on year to $682.3 million. On the other hand, the company's outlook for the full year was close to analysts' estimates with revenue guided to $2.78 billion at the midpoint. It made a GAAP loss of $2.55 per share, down from its profit of $1.13 per share in the same quarter last year.

Is now the time to buy Vista Outdoor? Find out by accessing our full research report, it's free.

Vista Outdoor (VSTO) Q3 FY2024 Highlights:

- Market Capitalization: $1.64 billion

- Revenue: $682.3 million vs analyst estimates of $688.3 million (0.9% miss)

- EPS: -$2.55 vs analyst estimates of $0.82 (-$3.37 miss)

- The company reconfirmed its revenue guidance for the full year of $2.78 billion at the midpoint

- Free Cash Flow of $126.7 million, up from $28.03 million in the previous quarter

- Gross Margin (GAAP): 29.7%, down from 32.1% in the same quarter last year

“Over the last few months, Revelyst’s culture of innovation drove exciting new product introductions at the brand level, secured incremental revenue opportunities for the segment and led to the successful launch of our Revelyst Lyst, which brought products directly to consumers at the enterprise level,” said Eric Nyman, CEO of Revelyst and co-CEO of Vista Outdoor.

Emerging from a 2015 spin-off, Vista Outdoor (NYSE:VSTO) specializes in the production and sale of outdoor gear and shooting sports equipment.

Leisure Facilities and Products

Consumers have lots of choices when it comes to how they spend their free time and extra money, so the companies offering leisure products and experiences must highlight their value proposition. Fitness companies may be riding the wellness trend, for example, while those selling recreational vehicles or toys may have to lean into innovation to stand out. Either way, all leisure companies must compete against the 800-pound gorilla of social media and streaming entertainment, which offer instant gratification and have been taking share of consumers’ free time for over a decade.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Vista Outdoor's annualized revenue growth rate of 6% over the last 5 years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Vista Outdoor's recent history shines a dimmer light on the company, as its revenue was flat over the last 2 years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Vista Outdoor's recent history shines a dimmer light on the company, as its revenue was flat over the last 2 years.

This quarter, Vista Outdoor missed Wall Street's estimates and reported a rather uninspiring 9.6% year-on-year revenue decline, generating $682.3 million of revenue. Looking ahead, Wall Street expects sales to grow 1.7% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

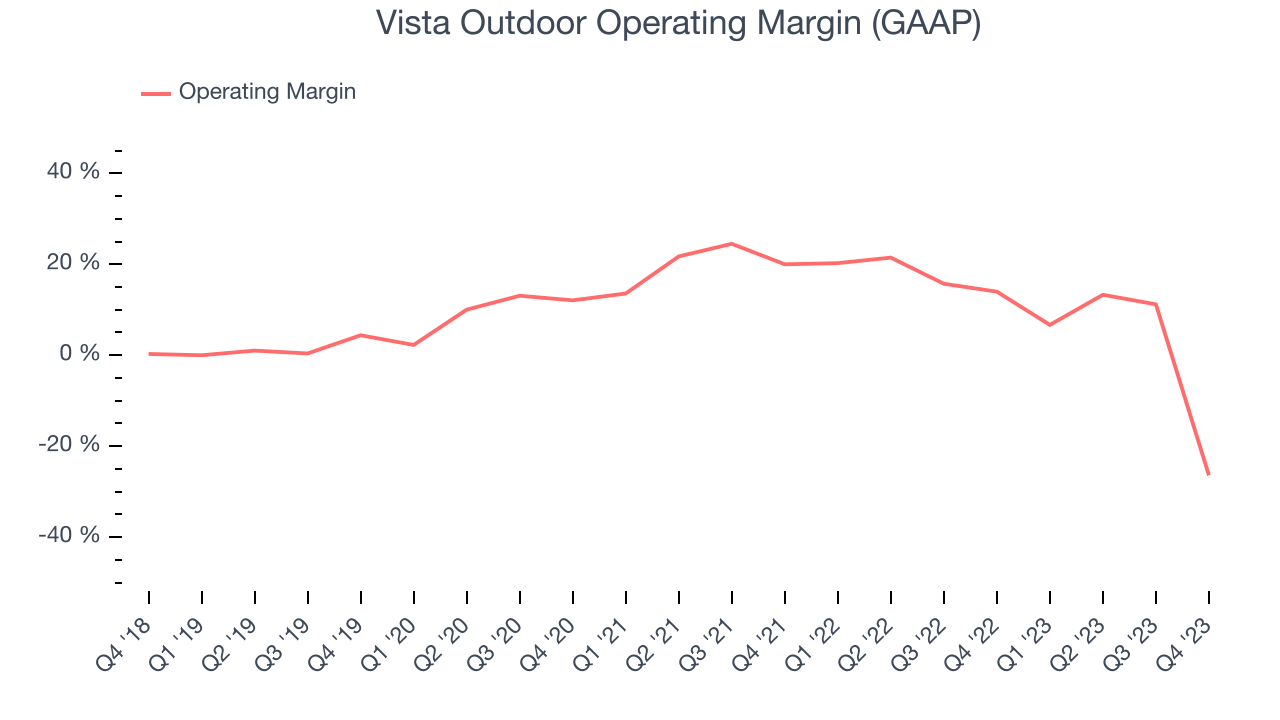

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Vista Outdoor was profitable over the last two years but held back by its large expense base. It's demonstrated mediocre profitability for a consumer discretionary business, producing an average operating margin of 9.5%.

This quarter, Vista Outdoor generated an operating profit margin of negative 26.4%, down 40.4 percentage points year on year. This reduction indicates the company was less efficient with its expenses over the last year, spending more money in areas like corporate overhead and advertising.

Over the next 12 months, Wall Street expects Vista Outdoor to shrink its losses but remain unprofitable. Analysts are expecting the company’s operating margin to rise by 12.2 percentage points to negative 14.2%.Key Takeaways from Vista Outdoor's Q3 Results

It was encouraging to see Vista Outdoor provide full-year revenue guidance that slightly topped analysts' expectations, but that's where the good news ends. Its revenue missed estimates, driven by lower sales volumes across nearly all categories. In response, the company lowered its prices and increased discounting to combat the term consumer pressures. Furthermore, its operating margin flipped from positive to negative while its adjusted EPS, EBITDA, and free cash flow missed Wall Street's projections.

On the bright side, the planned $1.9 billion sale of its sporting products segment (renamed to The Kinetic Group) is going as planned. On the Revelyst side (its outdoor products segment), the company expects to start generating revenue growth next quarter.

Overall, this was a mediocre quarter for Vista Outdoor. The stock is flat after reporting and currently trades at $28.12 per share.

Vista Outdoor may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.