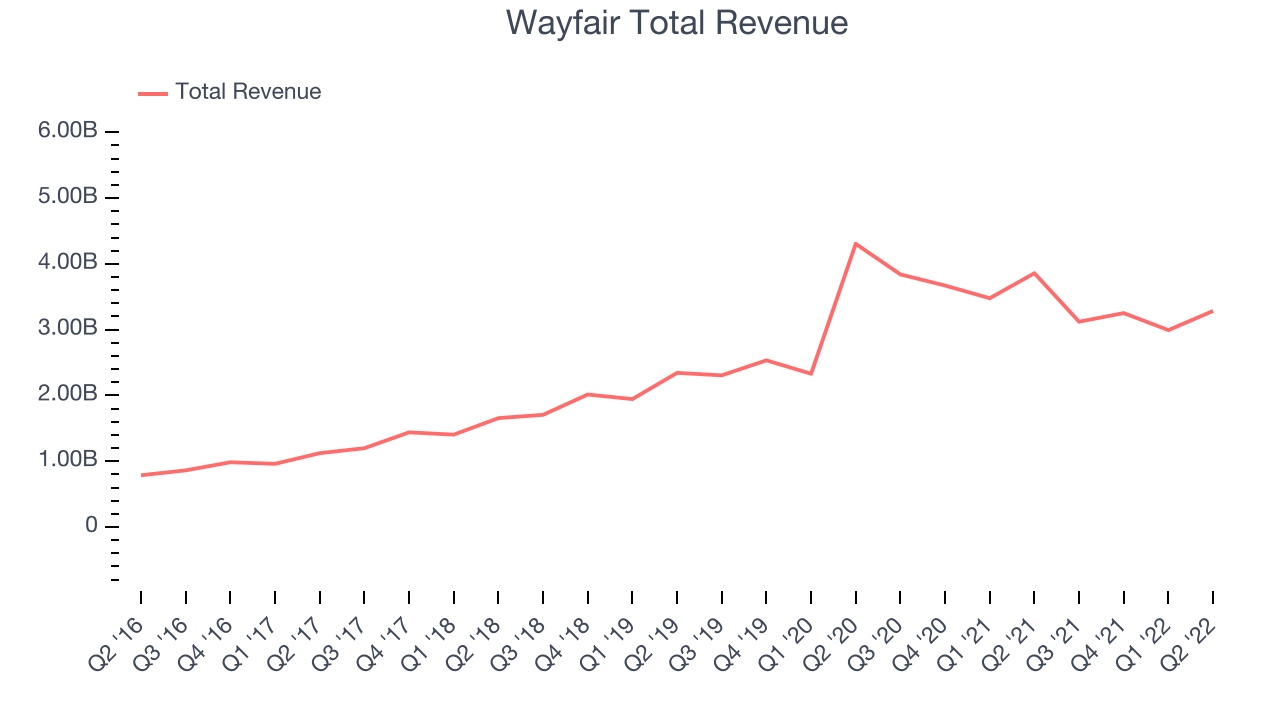

Online home goods retailer Wayfair (NYSE: W) reported Q2 FY2022 results that beat analyst expectations, with revenue down 14.8% year on year to $3.28 billion. Wayfair made a GAAP loss of $378 million, down on its profit of $130.4 million, in the same quarter last year.

Is now the time to buy Wayfair? Access our full analysis of the earnings results here, it's free.

Wayfair (W) Q2 FY2022 Highlights:

- Revenue: $3.28 billion vs analyst estimates of $3.18 billion (3.01% beat)

- EPS (non-GAAP): -$1.94 vs analyst estimates of -$1.88

- Free cash flow was negative $244 million, compared to negative free cash flow of $331 million in previous quarter

- Gross Margin (GAAP): 27.2%, down from 29.2% same quarter last year

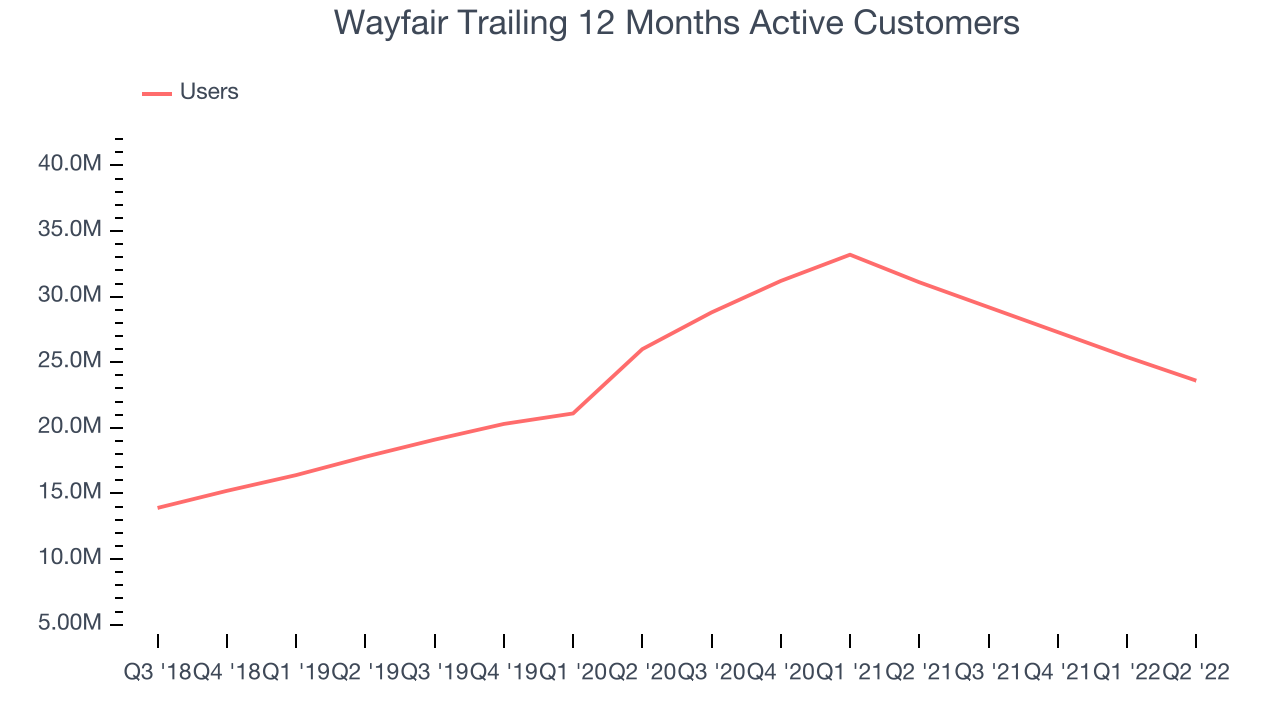

- Trailing 12 Months Active Customers: 23.6 million, down 7.5 million year on year

“During a difficult macroeconomic environment, we remain squarely focused on our customers and our suppliers, and on making sure Wayfair is their preferred platform for the Home. We are tightly controlling our many levers and steering Wayfair in a financially responsible manner through this period,” said Niraj Shah, CEO, co-founder and co-chairman, Wayfair.

Launched in 2002 by founder Niraj Shah, Wayfair (NYSE: W) is a leading online retailer for mass market home goods in the US, UK, Canada, and Germany.

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Sales Growth

Wayfair's revenue growth over the last three years has been strong, averaging 21.3% annually. The pandemic initially had a positive impact on Wayfair's revenue, but the growth has been pulled forward and subsequently normalized.

This quarter, Wayfair beat analyst estimates but reported a rather lacklustre 14.8% year on year revenue decline.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 4.03% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Usage Growth

As an online retailer, Wayfair generates revenue growth by growing both the number of buyers, and the average order size.

Over the last two years the number of Wayfair's active buyers, a key usage metric for the company, grew 15.3% annually to 23.6 million users. This is a solid growth for a consumer internet company.

Unfortunately, in Q2 the number of active buyers decreased by 7.5 million, a 24.1% drop year on year.

Key Takeaways from Wayfair's Q2 Results

Since it has still been burning cash over the last twelve months it is worth keeping an eye on Wayfair’s balance sheet, but we note that with a market capitalization of $6.78 billion and more than $1.73 billion in cash, the company has the capacity to continue to prioritise growth over profitability.

It was good to see Wayfair outperform Wall St’s revenue expectations this quarter. That feature of these results really stood out as a positive. On the other hand, there was a decline in number of users and the revenue has declined. Overall, this quarter's results could have been better. The company is flat on the results and currently trades at $64.09 per share.

Wayfair may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.