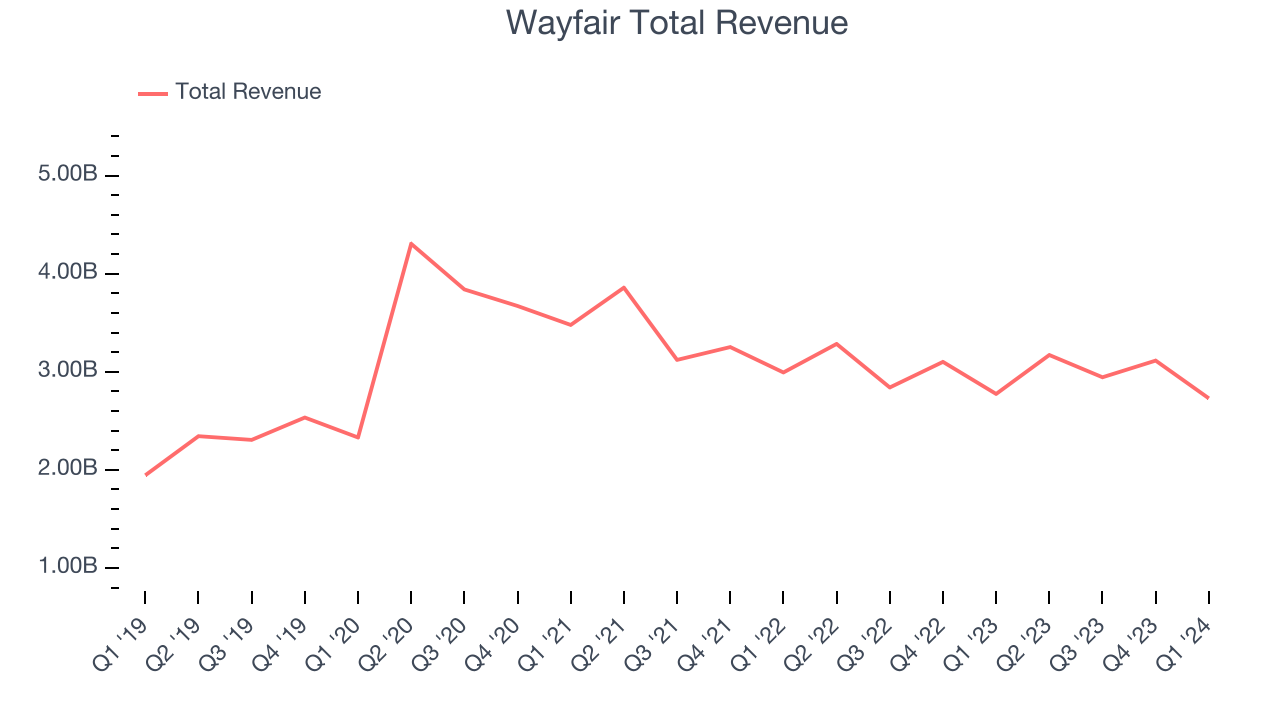

Online home goods retailer Wayfair (NYSE: W) announced better-than-expected results in Q1 CY2024, with revenue down 1.6% year on year to $2.73 billion. It made a non-GAAP loss of $0.32 per share, improving from its loss of $1.13 per share in the same quarter last year.

Is now the time to buy Wayfair? Find out by accessing our full research report, it's free.

Wayfair (W) Q1 CY2024 Highlights:

- Revenue: $2.73 billion vs analyst estimates of $2.64 billion (3.5% beat)

- Adjusted EBITDA: $75 million vs. analyst estimates of $71.8 million (4.4% beat)

- EPS (non-GAAP): -$0.32 vs analyst estimates of -$0.40

- Guidance is usually on the earnings call, and this can move the stock further

- Gross Margin (GAAP): 30%, up from 29.6% in the same quarter last year

- Free Cash Flow was -$193 million, down from $62 million in the previous quarter

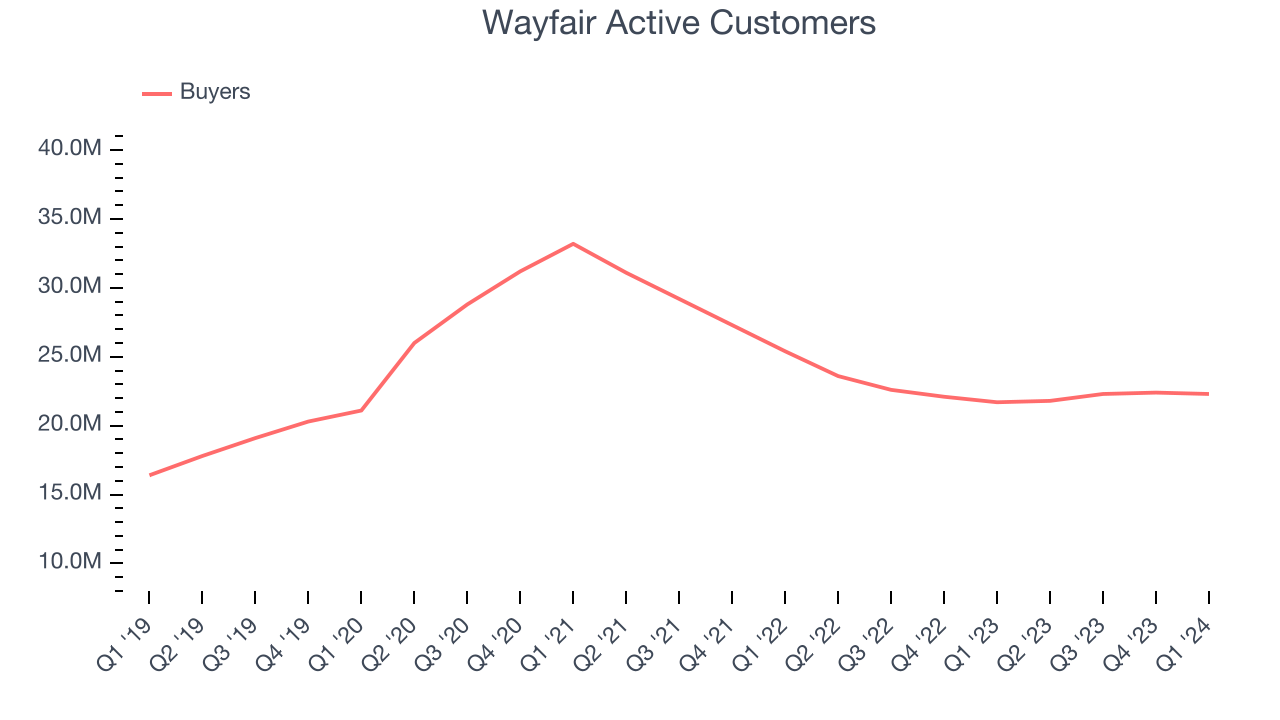

- Active Customers: 22.3 million, up 600,000 year on year

- Market Capitalization: $6.09 billion

"The first quarter ended on an upswing," said Niraj Shah, CEO, co-founder and co-chairman, Wayfair.

Launched in 2002 by founder Niraj Shah, Wayfair (NYSE: W) is a leading online retailer for mass market home goods in the US, UK, Canada, and Germany.

Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Sales Growth

Wayfair's revenue has been declining over the last three years, dropping on average by 7.6% annually. This quarter, Wayfair beat analysts' estimates but reported a year on year revenue decline of 1.6%.

Ahead of the earnings results, analysts were projecting sales to grow 1.3% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Usage Growth

As an online retailer, Wayfair generates revenue growth by expanding its number of buyers and the average order size in dollars.

Wayfair has been struggling to grow its active buyers, a key performance metric for the company. Over the last two years, its buyers have declined 10.6% annually to 22.3 million. This is one of the lowest rates of growth in the consumer internet sector.

Luckily, Wayfair added 600,000 active buyers in Q1, leading to 2.8% year-on-year growth.

Key Takeaways from Wayfair's Q1 Results

It was great to see Wayfair beat analysts' revenue and adjusted EBITDA expectations this quarter. On the other hand, its revenue growth slowed. Guidance is typically given on the earnings call, and this can move the stock further. Overall, this was a solid quarter for Wayfair. The stock is up 8.9% after reporting and currently trades at $55 per share.

So should you invest in Wayfair right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.