Walmart (NYSE:WMT) Beats Q2 Sales Targets

Petr Huřťák /

August 17, 2023

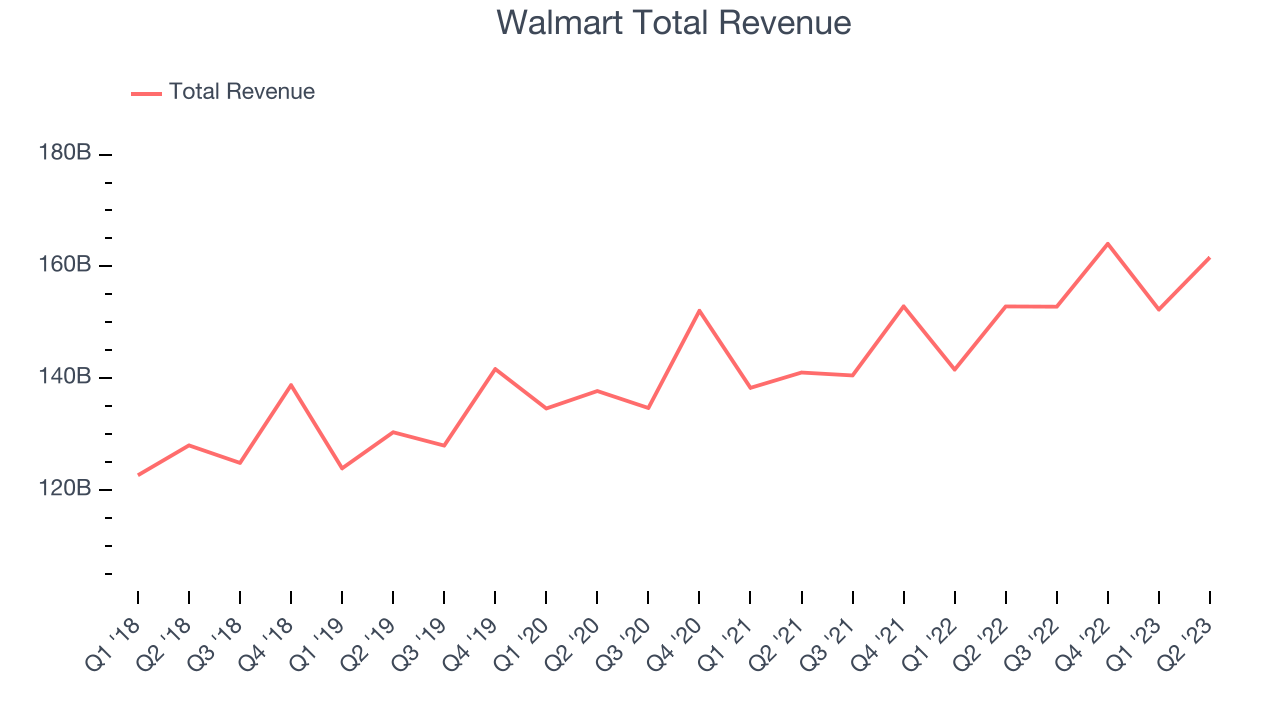

Retail behemoth Walmart (NYSE:WMT) reported results ahead of analysts' expectations in Q2 FY2024, with revenue up 5.74% year on year to $162 billion. Same-store sales and gross margin both exceeded expectations and along with the revenue beat, led to a 7.0% beat on adjusted EPS in the quarter. Guidance for next quarter and the full year were more mixed.

Is now the time to buy Walmart? Find out in our full research available to StockStory Edge members.

Walmart (WMT) Q2 FY2024 Highlights:

- Revenue: $162 billion vs analyst estimates of $159 billion (1.53% beat)

- EPS (non-GAAP): $1.84 vs analyst estimates of $1.72 (7.0% beat)

- EPS (non-GAAP) Guidance for Q3 2024 is $1.48 at the midpoint, below analyst estimates of $1.49

- Free Cash Flow of $8.78 billion, up from $9.05 billion in the same quarter last year

- Gross Margin (GAAP): 24.6%, up from 24.2% in the same quarter last year

- Same-Store Sales were up 6.4% year on year

"We had another strong quarter...Food is a strength, but we’re also encouraged by our results in general merchandise versus our expectations when we started the quarter. Our associates helped deliver increases in transaction counts and units sold, and profit is growing faster than sales. We’re in good shape with inventory, and we like our position for the back half of the year.” - Doug McMillon, President and CEO of Walmart

Known for its large-format Supercenters, Walmart (NYSE:WMT) is a retail pioneer that serves a budget-conscious consumer who is looking for a wide range of products under one roof.

Big-box retailers operate large stores that sell groceries and general merchandise at highly competitive prices. Because of their scale and resulting purchasing power, these big-box retailers–with annual sales in the tens to hundreds of billions of dollars–are able to get attractive volume discounts and sell at often the lowest prices. While e-commerce is a threat, these retailers have been able to weather the storm by either providing a unique in-store shopping experience or by reinvesting their hefty profits into omnichannel investments.

Sales Growth

Walmart is a behemoth in the consumer retail sector and benefits from economies of scale, an important advantage giving the business an edge in distribution and more negotiating power with suppliers.

As you can see below, the company's annualized revenue growth rate of 5.05% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre despite closing stores, implying that growth was driven by higher sales at existing, established stores.

This quarter, Walmart reported solid year-on-year revenue growth of 5.74% and its revenue of $162 billion outperformed analysts' estimates by 1.53%. Looking ahead, the analysts covering the company expect sales to grow 2.46% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

A retailer's store count often determines on how much revenue it can generate.

When a retailer like Walmart is shuttering stores, it usually means that brick-and-mortar demand is less than supply, and the company is responding by closing underperforming locations and possibly shifting sales online. As of the most recently reported quarter, Walmart operated 10,500 total retail locations, in line with its store count a year ago.

Taking a step back, the company has generally closed its stores over the last two years, averaging a 1.33% annual decline in its physical footprint. A smaller store base means that the company must rely on higher foot traffic and sales per customer at its remaining stores as well as e-commerce sales to fuel revenue growth.

Same-Store Sales

Walmart's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 6.93% year on year. Given its declining store count over the same period, this performance could stem from higher e-commerce sales or increased foot traffic at existing stores, which is sometimes a side effect of reducing the total number of stores. Nevertheless, Walmart is likely optimizing its operations for improved efficiency and profitability before expanding its physical footprint.

In the latest quarter, Walmart's same-store sales rose 6.4% year on year. This growth was in line with the 6.5% year-on-year increase it had posted 12 months ago.

Key Takeaways from Walmart's Q2 Results

With a market capitalization of $429 billion, a $13.9 billion cash balance, and positive free cash flow over the last 12 months, we're confident that Walmart has the resources needed to pursue a high-growth business strategy.

The quarter itself was quite solid, with same-store sales, total revenue, and adjusted EPS all coming in ahead of Wall Street analysts' expectations. Guidance was more mixed. The outlook for next quarter's revenue is roughly in line with expectations, although the outlook for adjusted EPS was slightly below. For the full year outlook, revenue was guided slightly below although adjusted EPS was guided above expectations. The stock is up 1.35% after reporting and currently trades at $161.41 per share.

So should you invest in Walmart right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.