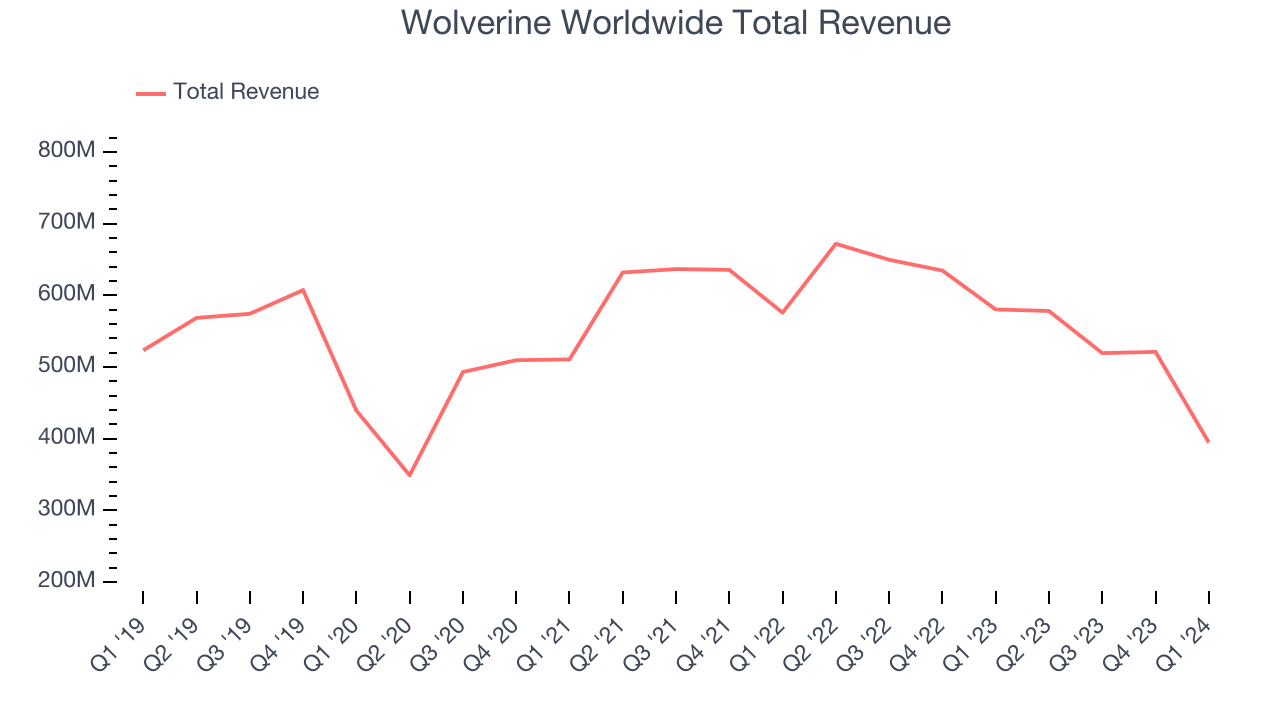

Footwear conglomerate Wolverine Worldwide (NYSE:WWW) reported Q1 CY2024 results exceeding Wall Street analysts' expectations, with revenue down 32% year on year to $394.9 million. On the other hand, the company's full-year revenue guidance of $1.71 billion at the midpoint came in slightly below analysts' estimates. It made a non-GAAP profit of $0.05 per share, down from its profit of $0.09 per share in the same quarter last year.

Wolverine Worldwide (WWW) Q1 CY2024 Highlights:

- Revenue: $394.9 million vs analyst estimates of $361.6 million (9.2% beat)

- EPS (non-GAAP): $0.05 vs analyst estimates of $0 ($0.05 beat)

- The company dropped its revenue guidance for the full year from $1.73 billion to $1.71 billion at the midpoint, a 1.2% decrease (but reiterated full year EPS (non-GAAP) guidance)

- Gross Margin (GAAP): 45.9%, up from 37.4% in the same quarter last year

- Free Cash Flow was -$42.3 million, down from $118.7 million in the previous quarter

- Market Capitalization: $912.6 million

Founded in 1883, Wolverine Worldwide (NYSE:WWW) is a global footwear company with a diverse portfolio of brands including Merrell, Hush Puppies, and Saucony.

Each brand in Wolverine Worldwide's lineup has its unique identity and market segment, ranging from outdoor and work footwear to fashion and casual wear. For example, Merrell is known for its high-performance outdoor footwear, appealing to adventure enthusiasts, while Hush Puppies offers relaxed, casual shoes that resonate with a lifestyle-oriented consumer base.

To improve its products, the company attempts to develop new materials and technologies to enhance comfort, durability, and performance. Some of Wolverine Worldwide's designs include Contour Welt and Durashocks, which are geared toward work footwear.

The company's global reach is supported by its extensive distribution network. Wolverine products are available in more than 200 countries and territories through a combination of wholesale, retail, e-commerce, and licensing channels. This ensures that Wolverine's brands are accessible to a vast consumer base worldwide.

Footwear

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Wolverine Worldwide's primary competitors include Nike (NYSE:NKE), Adidas (ETR:ADS), VF Corp (NYSE:VFC), who owns The North Face and Vans, Deckers Outdoor (NYSE:DECK), who owns UGG and Hoka, and Columbia Sportswear (NASDAQ:COLM).Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Wolverine Worldwide's revenue declined over the last five years, dropping 2% annually.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Wolverine Worldwide's recent history shows its demand has decreased even further as its revenue has shown annualized declines of 9.9% over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Wolverine Worldwide's recent history shows its demand has decreased even further as its revenue has shown annualized declines of 9.9% over the last two years.

This quarter, Wolverine Worldwide's revenue fell 32% year on year to $394.9 million but beat Wall Street's estimates by 9.2%. Looking ahead, Wall Street expects revenue to decline 12.5% over the next 12 months.

Operating Margin

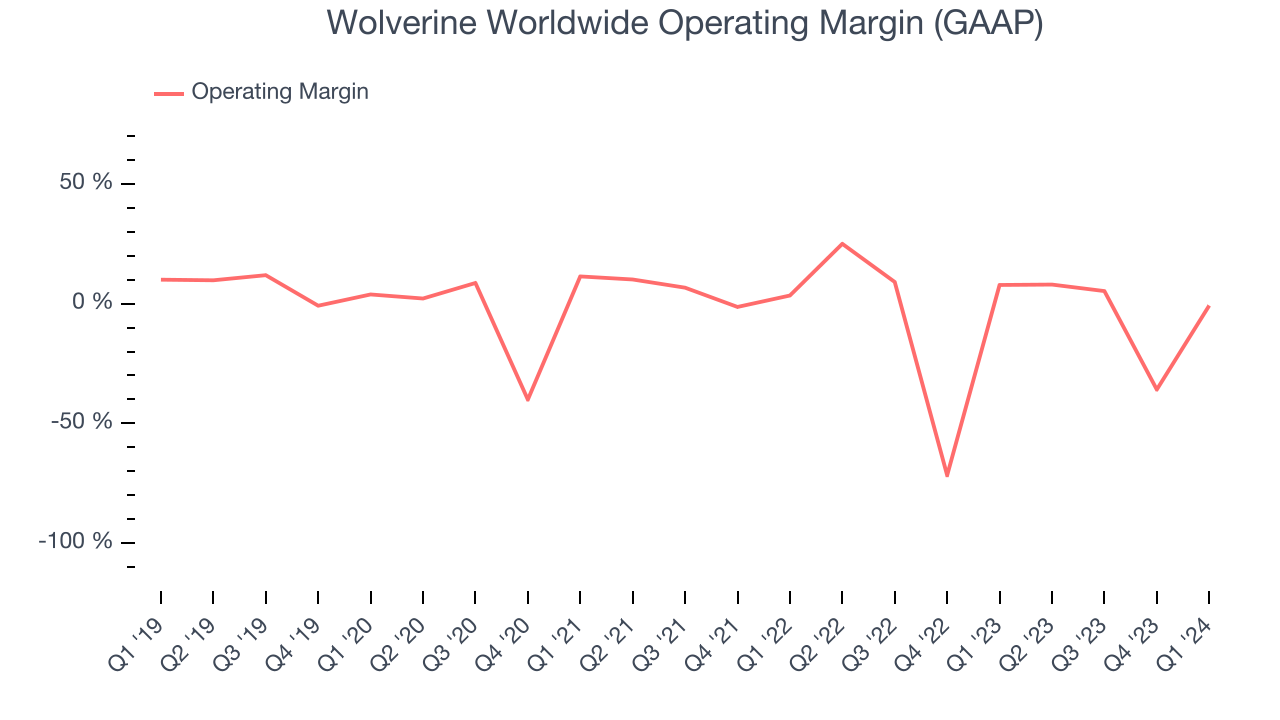

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Given the consumer discretionary industry's volatile demand characteristics, unprofitable companies should be scrutinized. Over the last two years, Wolverine Worldwide's high expenses have contributed to an average operating margin of negative 6.6%.

This quarter, Wolverine Worldwide generated an operating profit margin of negative 0.8%, down 8.6 percentage points year on year.

Over the next 12 months, Wall Street expects Wolverine Worldwide to become profitable. Analysts are expecting the company’s LTM operating margin of negative 5.8% to rise to positive 7.4%.EPS

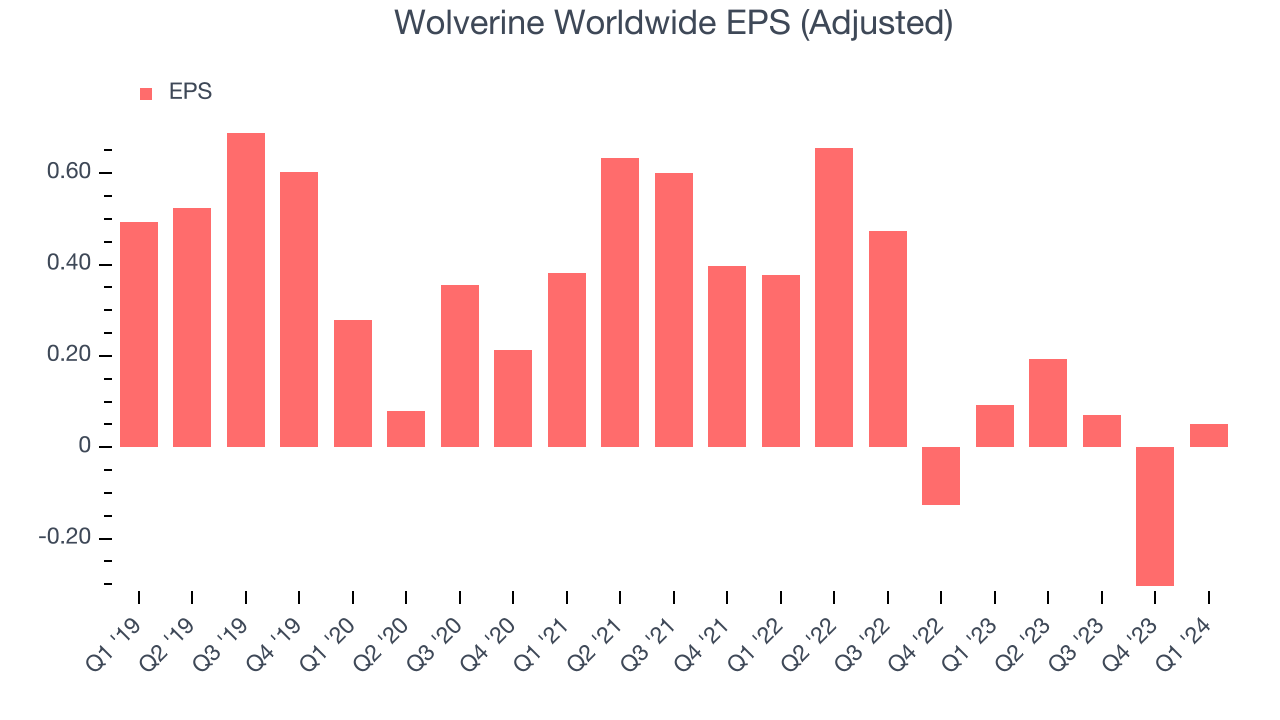

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, Wolverine Worldwide's EPS dropped 1,142%, translating into 65.5% annualized declines. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends or consumer preferences. Consumer discretionary companies are particularly exposed to this, leaving a low margin of safety around the company (making the stock susceptible to large downward swings).

In Q1, Wolverine Worldwide reported EPS at $0.05, down from $0.09 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. Over the next 12 months, Wall Street expects Wolverine Worldwide to grow its earnings. Analysts are projecting its LTM EPS of $0.01 to climb by 8,903% to $0.97.

Cash Is King

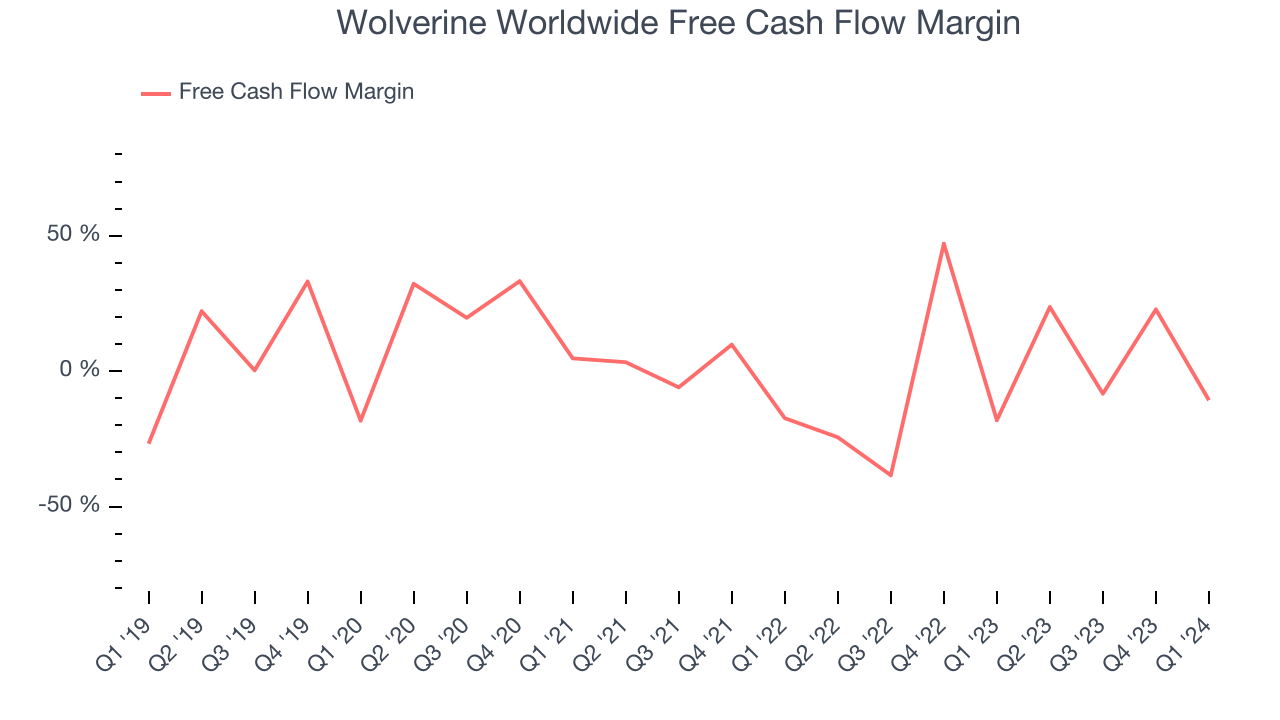

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, Wolverine Worldwide's demanding reinvestments to stay relevant with consumers have drained company resources. Its free cash flow margin has been among the worst in the consumer discretionary sector, averaging negative 1.1%.

Wolverine Worldwide burned through $42.3 million of cash in Q1, equivalent to a negative 10.7% margin, increasing its cash burn by 59.8% year on year.

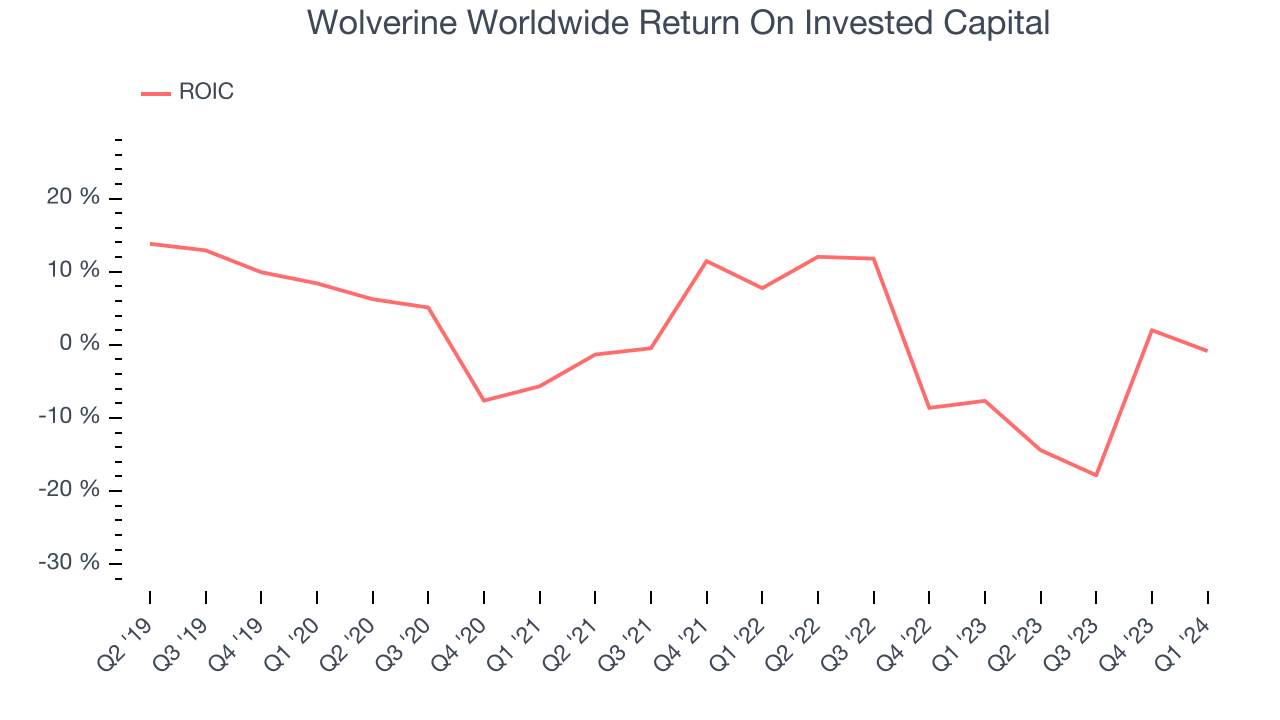

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Wolverine Worldwide's five-year average return on invested capital was 0.4%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Wolverine Worldwide's ROIC averaged 5.6 percentage point decreases over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Wolverine Worldwide's $1.02 billion of debt exceeds the $169.7 million of cash on its balance sheet. Furthermore, its 12x net-debt-to-EBITDA ratio (based on its EBITDA of $68.6 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Wolverine Worldwide could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Wolverine Worldwide can improve its balance sheet and remain cautious until it increases its profitability or reduces its debt.

Key Takeaways from Wolverine Worldwide's Q1 Results

We were impressed by how significantly Wolverine Worldwide blew past analysts' EPS expectations this quarter. We were also excited its revenue outperformed Wall Street's estimates. On the other hand, its operating margin missed and its full-year revenue guidance slightly fell short of Wall Street's estimates. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is flat after reporting and currently trades at $11.4 per share.

Is Now The Time?

Wolverine Worldwide may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Wolverine Worldwide, we'll be cheering from the sidelines. Its revenue has declined over the last five years, and analysts expect growth to deteriorate from here. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its declining EPS over the last five years makes it hard to trust. On top of that, its relatively low ROIC suggests it has historically struggled to find compelling business opportunities.

Wolverine Worldwide's price-to-earnings ratio based on the next 12 months is 11.8x. While there are some things to like about Wolverine Worldwide and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $10.57 per share right before these results (compared to the current share price of $11.40).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.