Outdoor lifestyle products brand (NYSE:YETI) fell short of analysts' expectations in Q4 FY2023, with revenue up 16% year on year to $519.8 million. It made a non-GAAP profit of $0.90 per share, improving from its profit of $0.78 per share in the same quarter last year.

YETI (YETI) Q4 FY2023 Highlights:

- Revenue: $519.8 million vs analyst estimates of $535.9 million (3% miss)

- EPS (non-GAAP): $0.90 vs analyst expectations of $0.96 (6.4% miss)

- Guidance for 2024 EPS (non-GAAP): $2.48 at the midpoint vs analyst expectations of $2.68 (7.6% miss)

- Free Cash Flow of $159.5 million, up 121% from the previous quarter

- Gross Margin (GAAP): 60.6%, up from 37.3% in the same quarter last year

- Market Capitalization: $4.19 billion

Founded by two brothers from Texas, YETI (NYSE:YETI) specializes in durable outdoor goods including coolers, drinkware, and gear tailored for adventure enthusiasts.

YETI was born out of frustration with the fragility of standard coolers that failed to meet the rigorous demands of outdoor activities. The founders, two avid outdoorsmen, established the company in 2006 to craft a cooler that could withstand harsh conditions and outlast the competition.

Today, the company’s products are engineered for durability and encompass coolers, drinkware, and related accessories.

YETI's products command premium prices, which are made possible by its customer base that is willing to pay more for quality and durability. The company's business model involves direct-to-consumer sales through its website and select retail partnerships. It also sponsors various sporting events to market itself to consumers.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Competitors in the outdoor and recreation goods industry include Vista Outdoor (NYSE:VSTO), Johnson Outdoors (NASDAQ:JOUT), and Clarus Corporation (NASDAQ:CLAR).Sales Growth

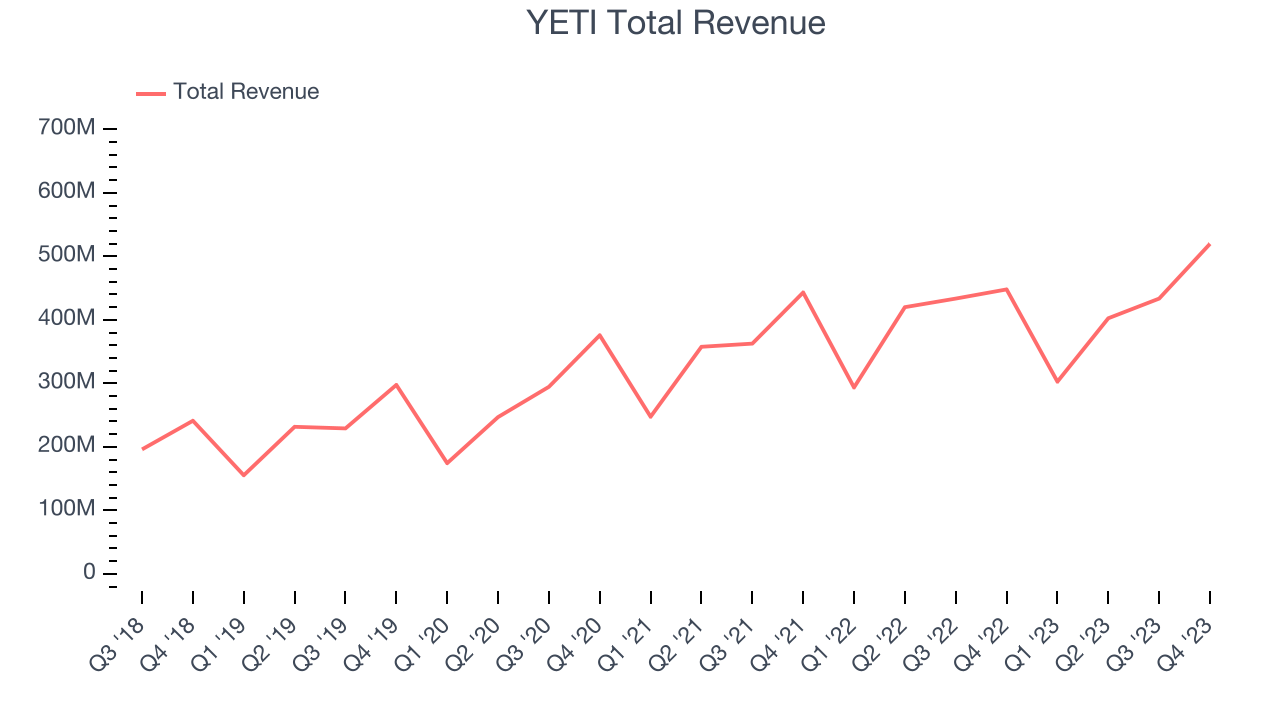

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. YETI's annualized revenue growth rate of 16.3% over the last five years was solid for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. YETI's recent history shows its momentum has slowed, as its annualized revenue growth of 8.4% over the last two years is below its five-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. YETI's recent history shows its momentum has slowed, as its annualized revenue growth of 8.4% over the last two years is below its five-year trend.

This quarter, YETI's revenue grew 16% year on year to $519.8 million, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 11.8% over the next 12 months, a deceleration from this quarter.

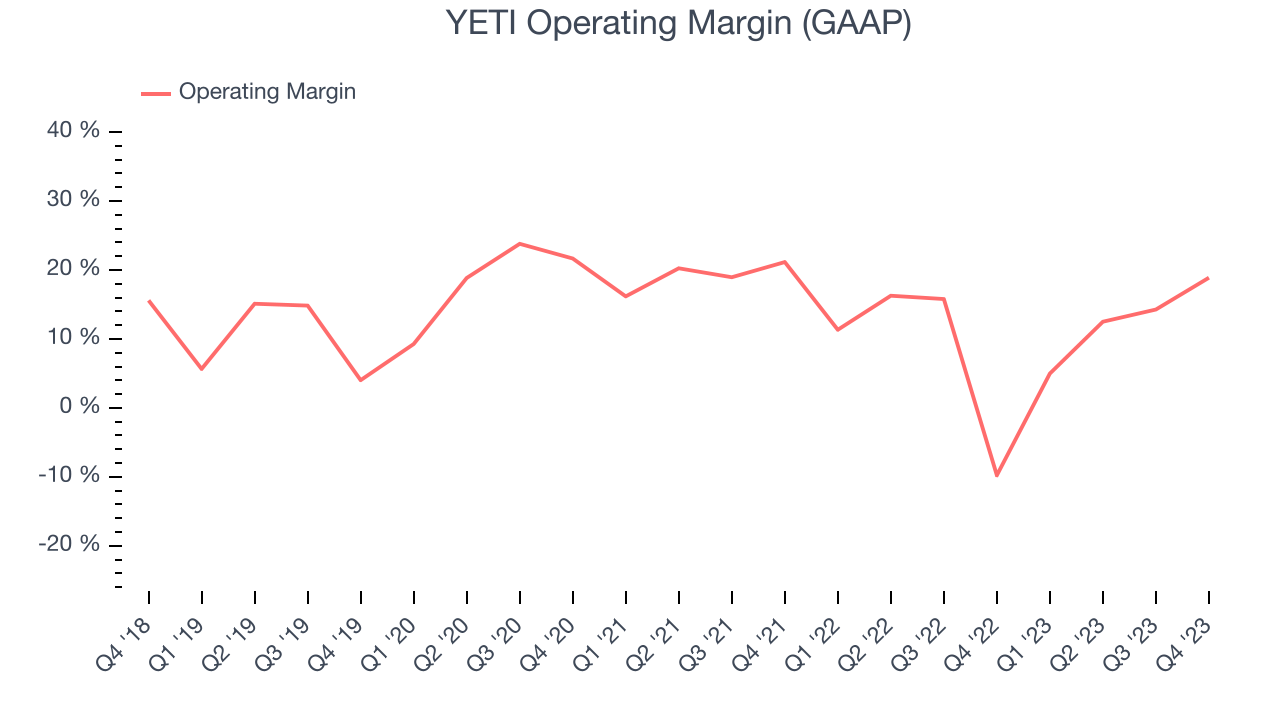

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

YETI has done a decent job managing its expenses over the last eight quarters. The company has produced an average operating margin of 10.8%, higher than the broader consumer discretionary sector.

In Q4, YETI generated an operating profit margin of 18.9%, up 28.6 percentage points year on year.

Over the next 12 months, Wall Street expects YETI to become more profitable. Analysts are expecting the company’s LTM operating margin of 13.6% to rise to 17.1%.EPS

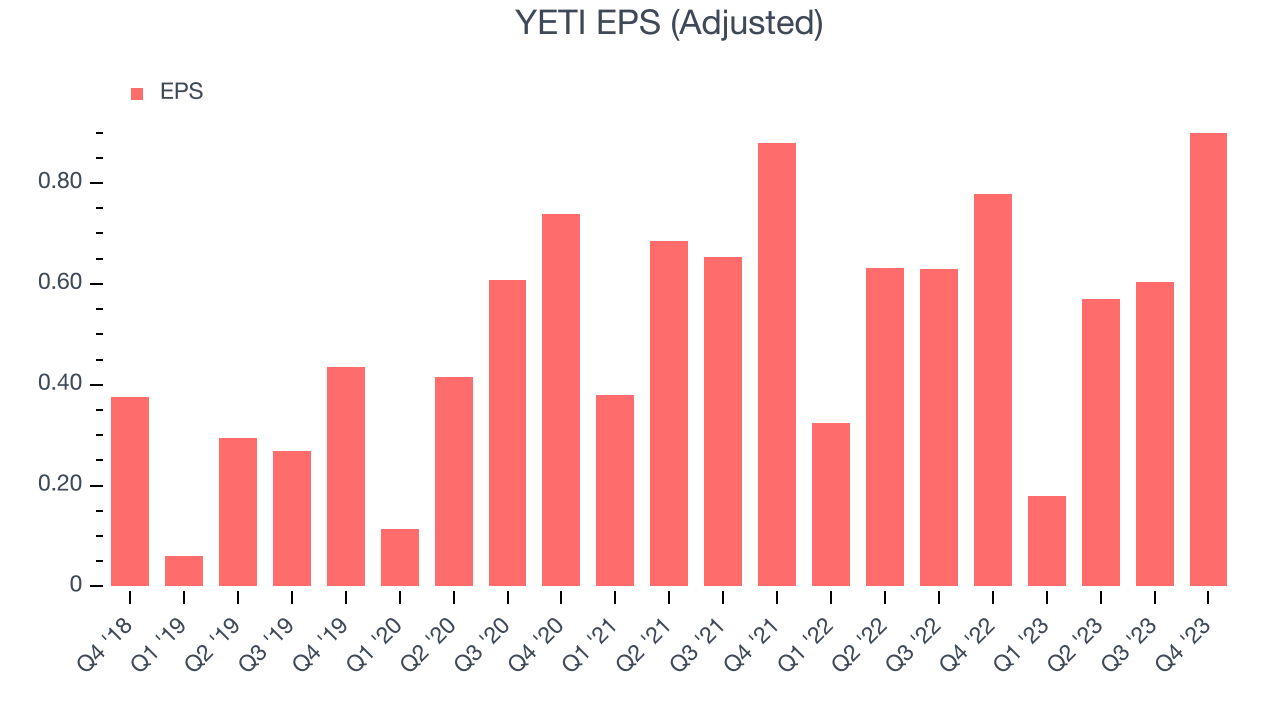

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, YETI's EPS grew 149%, translating into a remarkable 20% compounded annual growth rate. This performance is higher than its 16.3% annualized revenue growth over the same period. Let's dig into why.

YETI's operating margin has expanded 3.3 percentage points over the last five years, leading to higher profitability and earnings. Taxes and interest expenses can also affect EPS growth, but they don't tell us as much about a company's fundamentals.In Q4, YETI reported EPS at $0.90, up from $0.78 in the same quarter a year ago. This print unfortunately missed analysts' estimates, but we care more about long-term EPS growth rather than short-term movements. Over the next 12 months, Wall Street expects YETI to grow its earnings. Analysts are projecting its LTM EPS of $2.25 to climb by 19.4% to $2.69.

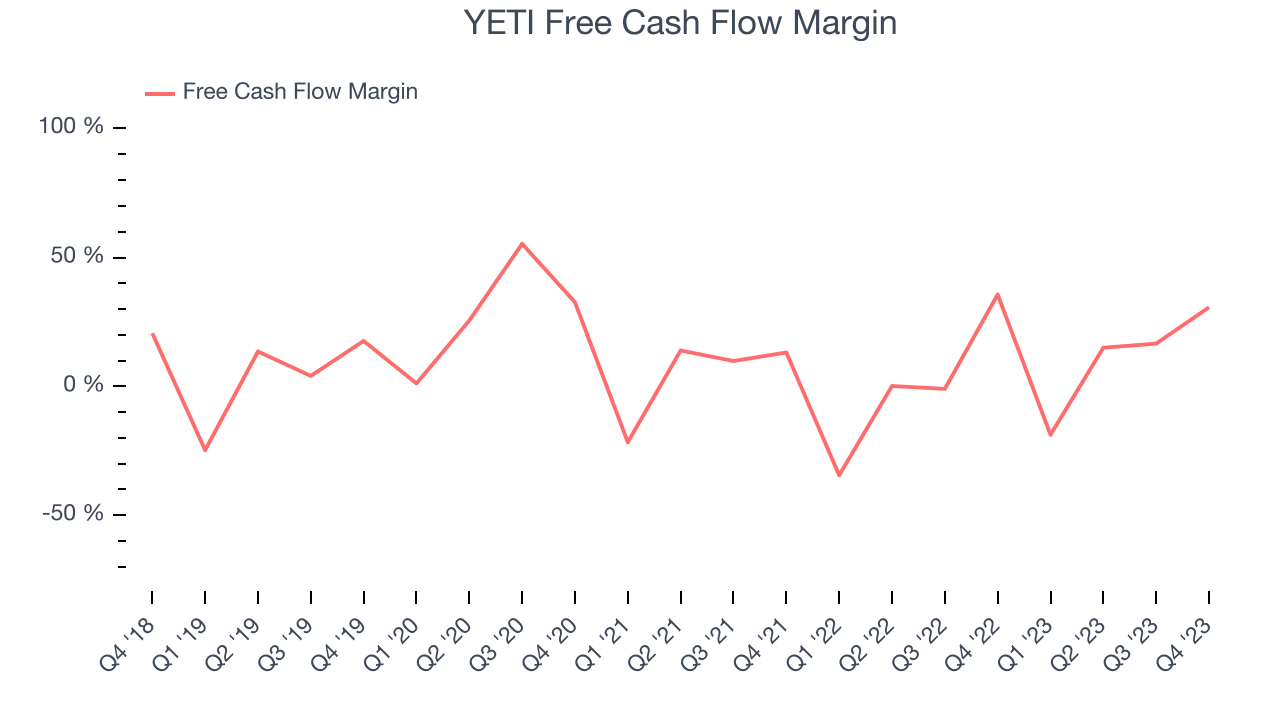

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, YETI has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 8.9%, subpar for a consumer discretionary business.

YETI's free cash flow came in at $159.5 million in Q4, equivalent to a 30.7% margin and in line with the same quarter last year. Over the next year, analysts predict YETI's cash profitability will fall. Their consensus estimates imply its LTM free cash flow margin of 14.2% will decrease to 10%.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

YETI's five-year average ROIC was 67.9%, placing it among the best consumer discretionary companies. Just as you’d like your investment dollars to generate returns, YETI's invested capital has produced excellent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, YETI's ROIC over the last two years averaged a 7.5 percentage point decrease each year. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Key Takeaways from YETI's Q4 Results

We struggled to find many strong positives in these results. Its full-year EPS forecast missed and its revenue fell short of Wall Street's estimates by a meaningful amount. In the quarter, revenue and EPS also fell short. Management said that "results were below our guidance, primarily as a result of more cautious and inconsistent spending on high-priced ticket items in our Coolers & Equipment category." Overall, this was a poor quarter for YETI. The company is down 12.9% on the results and currently trades at $42 per share.

Is Now The Time?

YETI may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We have other favorites, but we understand the arguments that YETI isn't a bad business. First off, its revenue growth has been good over the last five years. And while its falling ROIC shows its profitable business opportunities are shrinking, its EPS growth over the last five years has significantly beat its peer group average.

YETI's price-to-earnings ratio based on the next 12 months is 17.9x. There are things to like about YETI and there's no doubt it's a bit of a market darling, at least for some investors. But it seems there's a lot of optimism already priced in and we wonder if there are better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $47.81 per share right before these results (compared to the current share price of $42).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.